Global recovery is steady but slow and differs by region

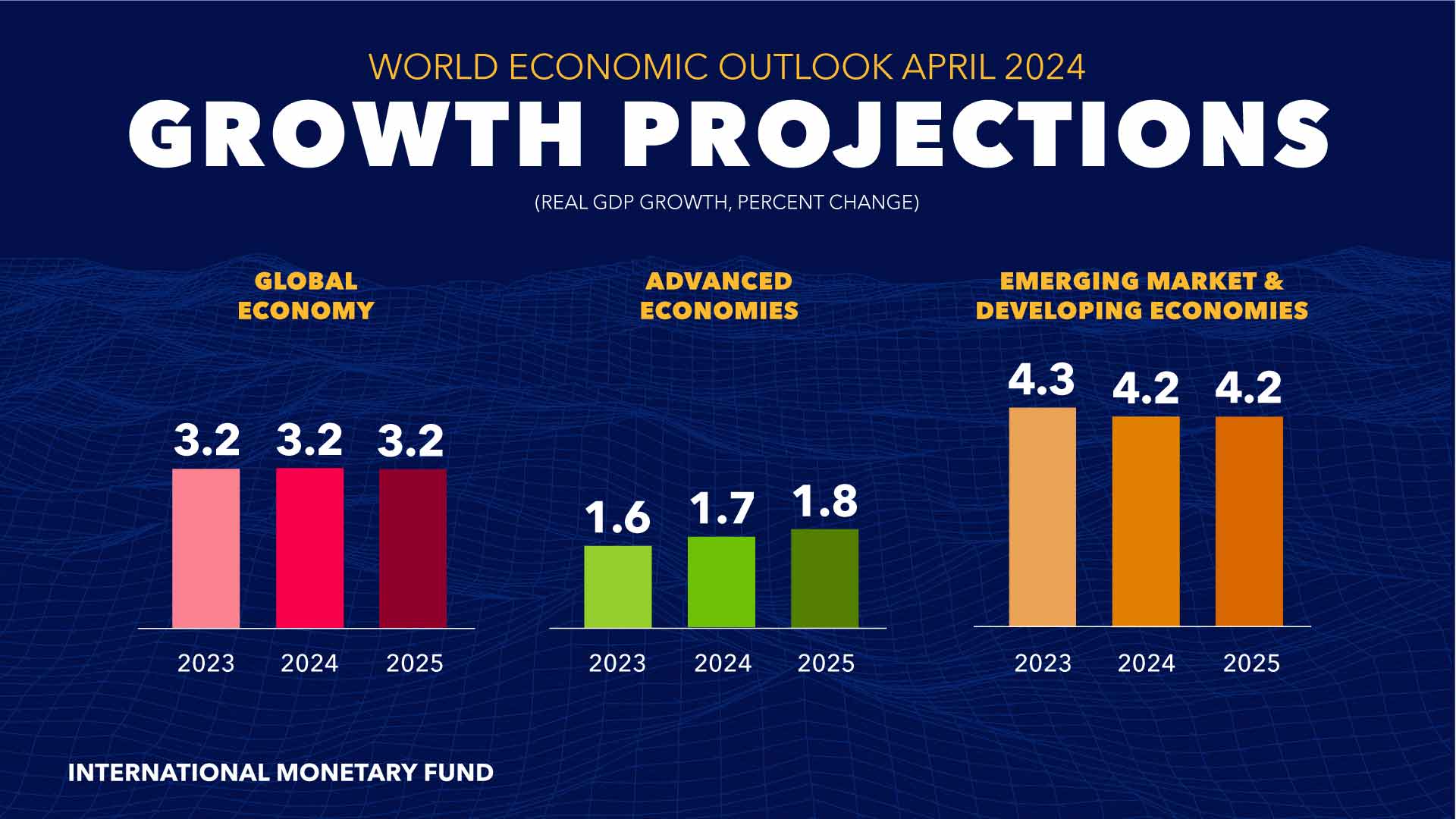

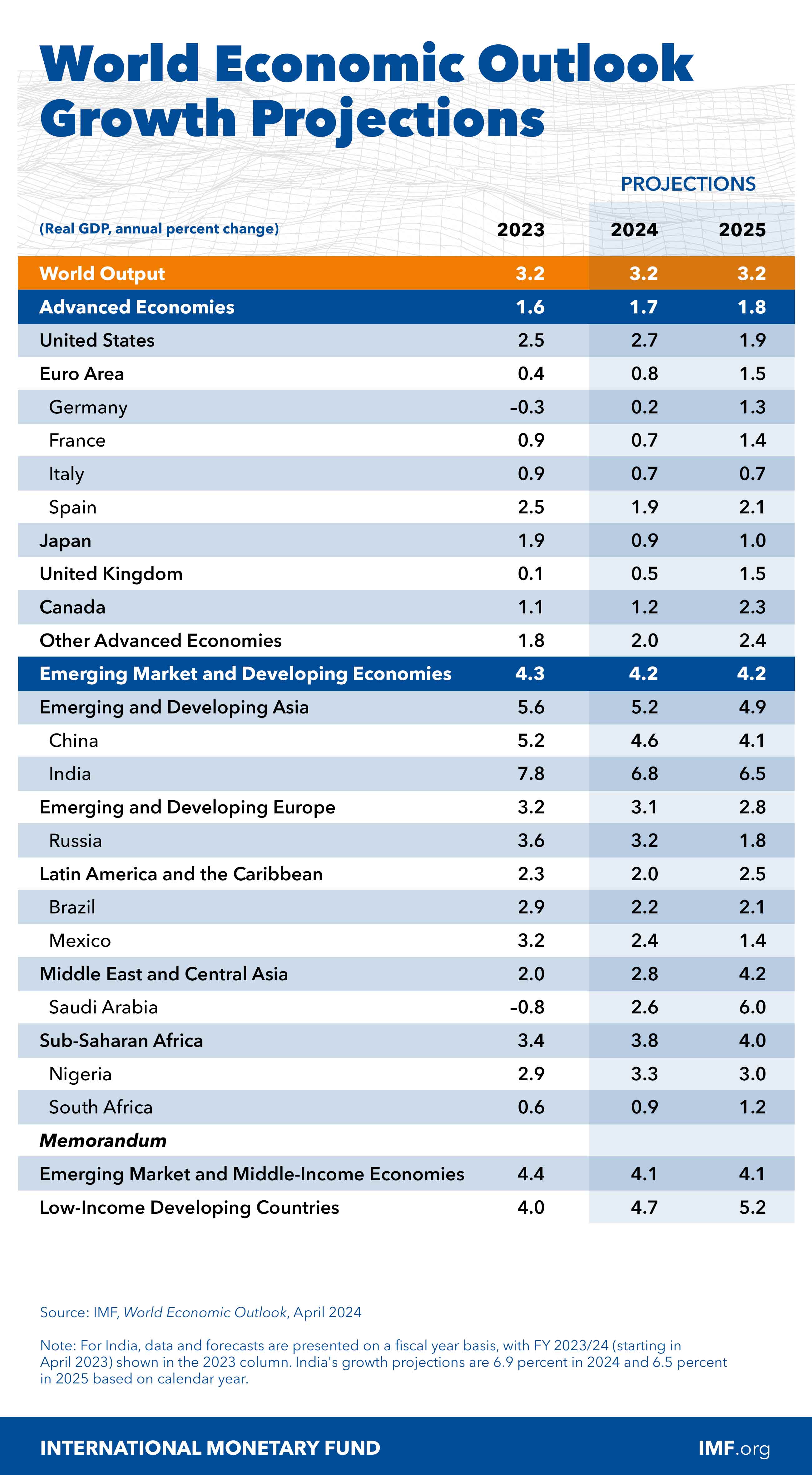

The baseline forecast is for the world economy to continue growing at 3.2 percent during 2024 and 2025, at the same pace as in 2023. A slight acceleration for advanced economies—where growth is expected to rise from 1.6 percent in 2023 to 1.7 percent in 2024 and 1.8 percent in 2025—will be offset by a modest slowdown in emerging market and developing economies from 4.3 percent in 2023 to 4.2 percent in both 2024 and 2025. The forecast for global growth five years from now—at 3.1 percent—is at its lowest in decades. Global inflation is forecast to decline steadily, from 6.8 percent in 2023 to 5.9 percent in 2024 and 4.5 percent in 2025, with advanced economies returning to their inflation targets sooner than emerging market and developing economies. Core inflation is generally projected to decline more gradually.

The global economy has been surprisingly resilient, despite significant central bank interest rate hikes to restore price stability. Chapter 2 explains that changes in mortgage and housing markets over the prepandemic decade of low interest rates moderated the near-term impact of policy rate hikes. Chapter 3 focuses on medium-term prospects and shows that the lower predicted growth in output per person stems, notably, from persistent structural frictions preventing capital and labor from moving to productive firms. Chapter 4 further indicates how dimmer prospects for growth in China and other large emerging market economies will weigh on trading partners.

Chapter 1: Global Prospects and Policies

Economic activity was surprisingly resilient through the global disinflation of 2022–23. As global inflation descended from its mid-2022 peak, economic activity grew steadily, defying warnings of stagflation and global recession. However, the pace of expansion is expected to be low by historical standards and the speed of convergence toward higher living-standards for middle- and lower-income countries has slowed, implying persistent global disparities. With inflationary pressures abating more swiftly than expected in many countries, risks to the global outlook are now broadly balanced compared with last year. Monetary policy should ensure that inflation touches down smoothly. A renewed focus on fiscal consolidation is needed to rebuild room for budgetary maneuver and priority investments, and to ensure debt sustainability. Intensifying supply-enhancing reforms are crucial to increase growth towards the higher prepandemic era average and accelerate income convergence. Multilateral cooperation is needed to limit the costs and risks of geoeconomic fragmentation and climate change, speed the transition to green energy, and facilitate debt restructuring.

Chapter 2: Feeling the Pinch? Tracing the Effects of Monetary Policy through Housing Markets

Why are some feeling the pinch from higher rates and not others? Chapter 2 investigates the effects of monetary policy across countries and over time through the lens of mortgage and housing markets. Monetary policy has greater effects where (1) fixed-rate mortgages are not common, (2) home buyers are more leveraged, (3) household debt is high, (4) housing supply is restricted, and (5) house prices are overvalued. These characteristics vary significantly across countries, and thus the effects of monetary policy are strong in some and weak in others. Moreover, recent shifts in mortgage and housing markets may have limited the drag of higher policy rates up to now in several countries. The risk that households may still feel the pinch should be taken seriously where fixed-rate mortgages have short fixation periods, especially if households are heavily indebted.

Chapter 3: Slowdown in Global Medium-Term Growth: What Will It Take to Turn the Tide?

The world economy's growth engine is losing steam, prompting questions about its medium-term prospects. Chapter 3 delves into the drivers behind the growth decline and identifies a significant and widespread slowdown in total factor productivity as a key factor, partly driven by increased misallocation of capital and labor between firms within sectors. Demographic pressures and a slowdown in private capital formation further precipitated the growth slowdown. Absent policy action or technological advances, medium-term growth is projected to fall well below prepandemic levels. To bolster growth, urgent reforms are necessary to improve resource allocation to productive firms, boost labor force participation, and leverage artificial intelligence for productivity gains. Addressing these issues is critical, given the additional constraints high public debt and geoeconomic fragmentation may impose on future growth.

Chapter 4: Trading Places: Real Spillovers from G20 Emerging Markets

As G20 emerging markets account for almost one-third of world GDP and about one-quarter of global trade, spillovers from shocks originating in these economies can have important ramifications for global activity. Chapter 4 documents that, since 2000, spillovers from shocks in G20 emerging markets—particularly China—have increased and are now comparable in size to those from shocks in advanced economies. Trade, notably through global value chains, is a key propagation channel. Spillovers generate a reallocation of economic activity across firms and sectors in other countries. Looking ahead, a plausible growth acceleration in G20 emerging markets, even excluding China, could support global growth over the medium term and spill over to other countries. Policymakers in recipient economies should maintain sufficient buffers and strengthen policy frameworks to manage the possibility of larger shocks from G20 emerging markets.

Publications

-

September 2024

Finance & Development

- PRODUCTIVITY

-

September 2024

Annual Report

- Resilience in the Face of Change

-

Regional Economic Outlooks

- Latest Issues