The risks to global growth are broadly balanced and a soft landing is a possibility

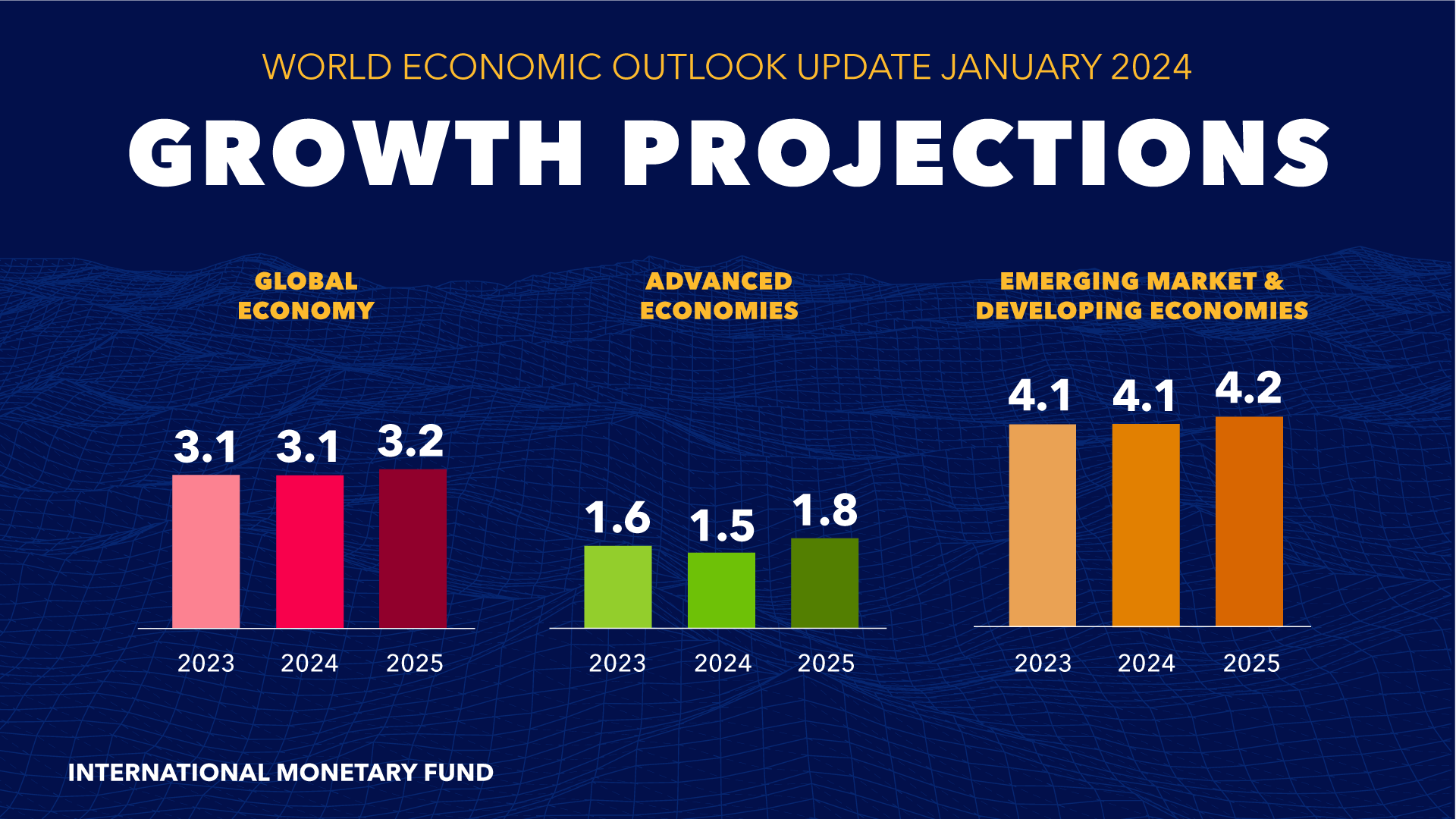

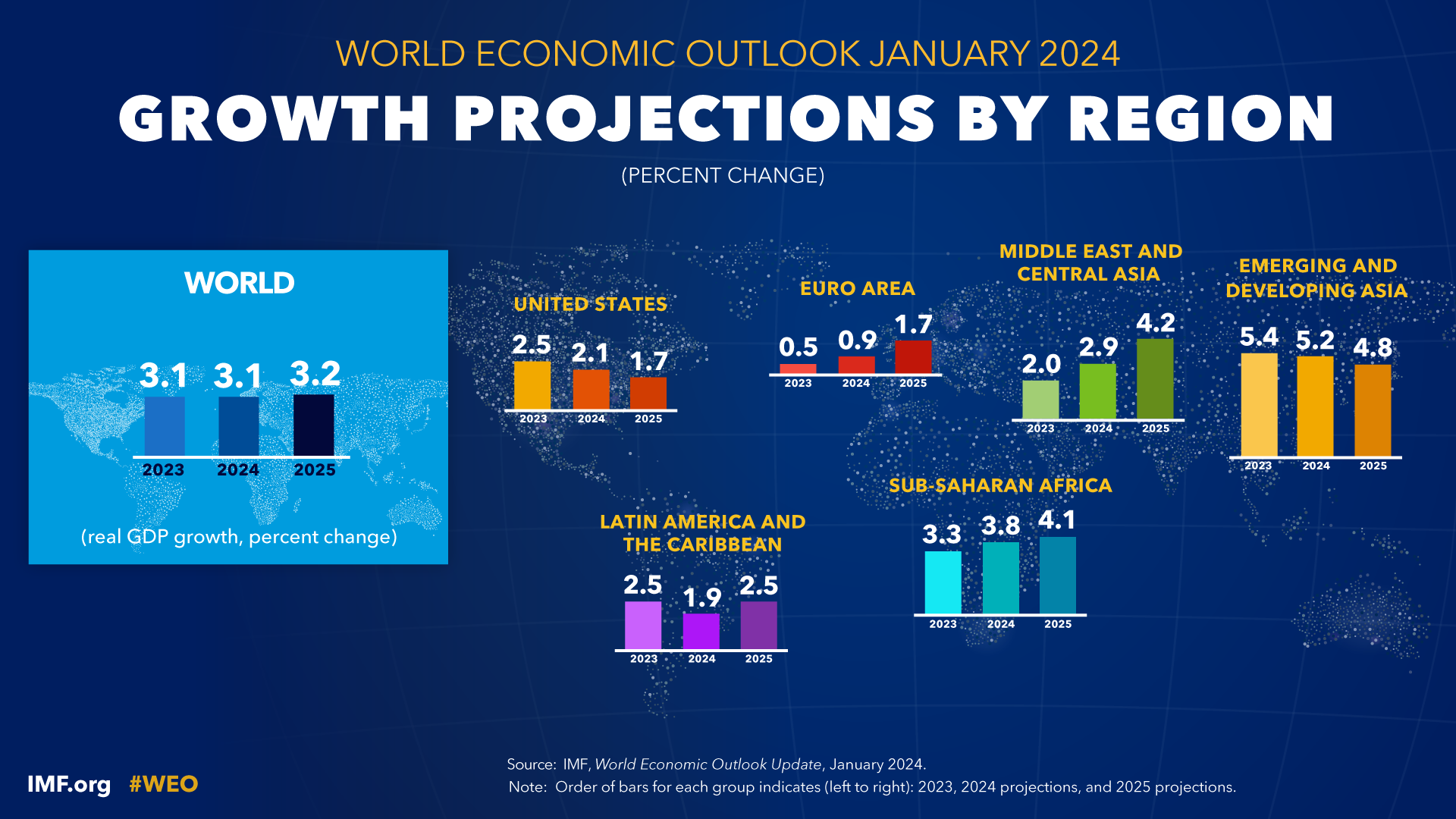

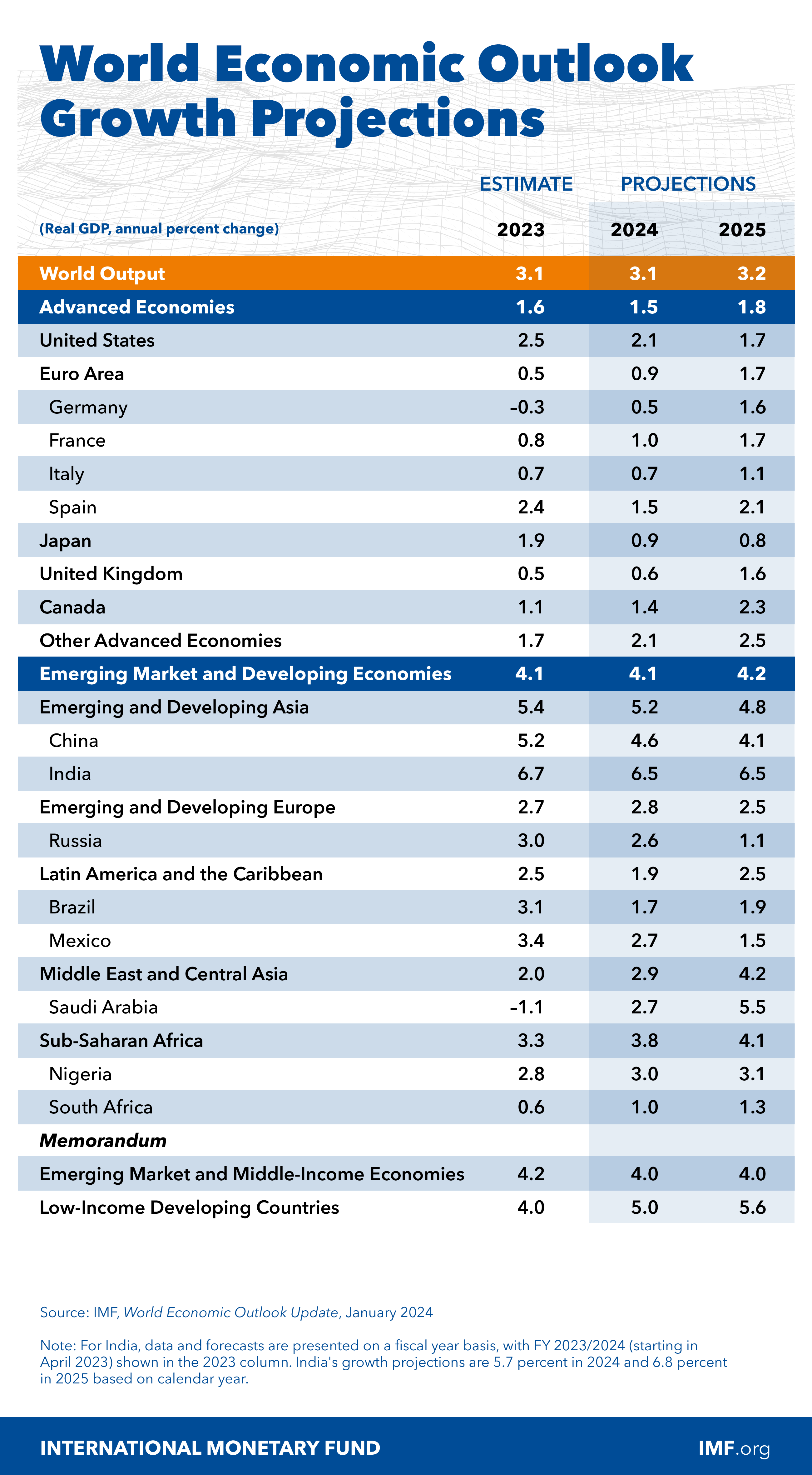

Global growth is projected at 3.1 percent in 2024 and 3.2 percent in 2025, with the 2024 forecast 0.2 percentage point higher than that in the October 2023 World Economic Outlook (WEO) on account of greater-than-expected resilience in the United States and several large emerging market and developing economies, as well as fiscal support in China. The forecast for 2024–25 is, however, below the historical (2000–19) average of 3.8 percent, with elevated central bank policy rates to fight inflation, a withdrawal of fiscal support amid high debt weighing on economic activity, and low underlying productivity growth. Inflation is falling faster than expected in most regions, in the midst of unwinding supply-side issues and restrictive monetary policy. Global headline inflation is expected to fall to 5.8 percent in 2024 and to 4.4 percent in 2025, with the 2025 forecast revised down.

With disinflation and steady growth, the likelihood of a hard landing has receded, and risks to global growth are broadly balanced. On the upside, faster disinflation could lead to further easing of financial conditions. Looser fiscal policy than necessary and than assumed in the projections could imply temporarily higher growth, but at the risk of a more costly adjustment later on. Stronger structural reform momentum could bolster productivity with positive cross-border spillovers. On the downside, new commodity price spikes from geopolitical shocks––including continued attacks in the Red Sea––and supply disruptions or more persistent underlying inflation could prolong tight monetary conditions. Deepening property sector woes in China or, elsewhere, a disruptive turn to tax hikes and spending cuts could also cause growth disappointments.

Policymakers’ near-term challenge is to successfully manage the final descent of inflation to target, calibrating monetary policy in response to underlying inflation dynamics and—where wage and price pressures are clearly dissipating—adjusting to a less restrictive stance. At the same time, in many cases, with inflation declining and economies better able to absorb effects of fiscal tightening, a renewed focus on fiscal consolidation to rebuild budgetary capacity to deal with future shocks, raise revenue for new spending priorities, and curb the rise of public debt is needed. Targeted and carefully sequenced structural reforms would reinforce productivity growth and debt sustainability and accelerate convergence toward higher income levels. More efficient multilateral coordination is needed for, among other things, debt resolution, to avoid debt distress and create space for necessary investments, as well as to mitigate the effects of climate change.

Publications

-

March 2024

Finance & Development

-

ECONOMICS

How should it change?

-

September 2023

Annual Report

- COMMITTED TO COLLABORATION

-

Regional Economic Outlooks

- Latest Issues