The long reach of life experience affects real-world economic outcomes, for policymakers and consumers alike

On October 29, 1929, the roaring twenties came to a sudden close in the United States. In an event known as “Black Tuesday,” the US stock market collapsed, and it would not match its 1929 peak for a long time, until the 1950s.

The subsequent impacts of the Great Depression were not felt just in the stock market. They were felt in people’s stomachs as they lined up at soup kitchens or slept in shantytowns. Those who grew up during the Great Depression, the “Depression babies,” were a generation that was extraordinarily frugal and averse to risks, especially those of the stock market. The trauma people experienced altered a whole generation, their beliefs and outlook on the world and their economic choices—in financial markets, in labor markets, and in many other aspects of their lives.

In economic science, Depression babies have come to represent a new wave of behavioral economics research. It is broadening the field to draw knowledge and methods from adjacent social and natural sciences, in addition to its origins as psychology and economics. Many of the new topics and methods regarding trauma, stress, addiction, mental health, and child development are inherently focused on policy. They link directly to work on what Anne Case and Angus Deaton termed “deaths of despair” in the 21st century and to the persistence of gender roles and racial discrimination.

Behavioral beginnings

But let’s step back for a brief origin story. More than 50 years ago, in the late 1960s, the field of economics was comfortable with mathematical rigor and models, and the most prominent economists of the era, such as Paul Samuelson and Milton Friedman, felt they were more like physicists than psychologists. Yet, at about the same time, two Israeli psychologists, Daniel Kahneman and Amos Tversky, met at Hebrew University in Jerusalem and started a collaboration that would eventually change the status quo in economics. Their most famous work, introducing prospect theory in 1979, combined a few principles to describe how people make decisions when facing risk—principles that seemed very plausible and that were also inconsistent with traditional economics. One principle is that people overweight minuscule probabilities and underweight likely events. (Have you ever felt disturbed by the tiny probability of a plane crash? That’s what they mean.) Another key insight was that people care about changes in relative wealth and wholeheartedly despise losses. (You may find yourself frustrated if you lose $20, even if this barely affects your total wealth.) Prospect theory alone was deemed worthy of a Nobel Prize in economics, but Kahneman and Tversky contributed many more psychological insights about “heuristics and biases” to economic thought.

Once the flame of behavioral economics was lit, the torch was passed to researchers in economics and finance to continue this work. Richard Thaler, who won the Nobel Prize in economics in 2017, collaborated with Kahneman and Tversky and later would go on to publish a special series of articles titled Anomalies on phenomena that psychology-free economics could not explain, such as why stock prices tend to rise in January.

Behavioral economics at this time focused on identifying anomalies and offering psychological solutions to explain them. Once theoretical models were in place, a second wave of behavioral economics in the 2000s started focusing on documenting behavioral biases empirically—often large, real-world impacts—and incorporating them into other areas of economic research. For example, a key puzzle in development economics is why profitable investment opportunities, such as applying fertilizer, can have low take-up. The insight that people care a lot about changes in their relative wealth and hate losses (for example, if the fertilizer does not improve their crop yield) can help explain this puzzle.

In fact, behavioral economics became so well integrated into almost all fields of economics—finance, labor, public, development, macro—during this second wave of behavioral research that some might reasonably have thought, “We are done.” We have infused psychological realism into the classical Homo economicus, the economic person who always chooses optimally and looks more like a computer than a human.

Mind and body

But here is the problem: if we think of Homo economicus as a computer, then behavioral economics introduced the idea that this computer may have flawed software and may occasionally short-circuit. Yet, even with these flaws, the behavioral agent remained a computer, albeit one that malfunctioned somewhat. However the programming is set up—with a dose of overoptimism, recency bias, or sunk-cost fallacy—dictates how the behavioral agent proceeds forever.

And that’s decidedly not what happened with Depression babies. Their experience altered them profoundly. In fact, don’t the members of every generation have shared experiences that alter them? That’s why we have names for them, such as “baby boomers” for those born into the postwar boom.

This is what the most recent wave of behavioral economics aims to bring to the field. Humans are much more than computers, even computers with flawed software. They are living, breathing organisms affected by their unique life paths. Many economic researchers—in health economics and neuroeconomics, for example—have long argued that we cannot ignore the biological mechanisms that govern our bodies and rewire our brains. We are now in a position to see more systematically the missing pieces: humans have a mind and a body, and an economic science that describes human behavior needs to account for both.

How can this insight help us do economics better? Let’s return to the Depression babies and how economic research has conceptualized what happened to their generation. Neuroscience and neuropsychiatry research tell us that our past personal experiences alter how we are wired. Decades of research on neuroplasticity document how the human brain continually reorganizes pathways based on new experiences. As our brain uses certain pathways more, these pathways become stronger. In contrast, pathways that are used less get pruned. Thus, in addition to the effects of hunger and stress, the Great Depression also persistently affected people’s brains. The experience exposed the real-life danger of financial markets and how they could jeopardize people’s ability to put food on the table. As a result, teens and young adults during the Great Depression of the 1930s were much less likely to participate in the stock market later in life. Only 13 percent invested in the stock market at all, less than half the rate of any later generation.

Experience effects

The concept of experience effects formalizes how personal lifetime experiences influence people’s beliefs and decisions in a lasting way. It challenges traditional economic thinking that people use all available information to form beliefs. One approach is to model human thinking and decision-making under risk as putting more weight on outcomes that people, personally, have seen in the past. If they have witnessed a colossal stock market crash, they will assume it can happen again and, moreover, believe that the risk is high. In fact, decades of data on US stock market investment confirm this: Investors who have experienced lower stock market returns during the preceding years of their lives are less likely to invest in the stock market. Individuals with good experiences are more likely to invest.

But experience effects are not only about what happened in the recent past. An important insight is that different generations are shaped differently and, as a result, might even respond differently to the same recent event. A 60-year-old will react very differently to a financial crisis and stock market crash than a 30-year-old, simply because the 60-year-old has seen so much more in her life and is intuitively taking the average over all those experiences. The 30-year-old has seen much less. Therefore, a recent crisis spans a larger proportion of his life and will receive greater weight in his thinking and decision-making. This is not to say that Kahneman and Tversky were wrong about simple recency bias. Quite the contrary! Individuals exhibit clear recency bias, weighting recent information more than very old information. But it is only personal lifetime experiences that count, and it is against a lifetime of past experiences that new experiences are weighted.

Stock market data reveal other interesting facets of human decision-making. One is the “domain specificity” of experience effects: experiences matter only for decisions in the same domain. For example, stock market experience does not seem to affect bond market investment. Research also reveals that domain-specific experiences can extend beyond just stock or bond returns. Related research on the stock market investment of East and West Germans shows that those who lived under communism are much less likely to trust the stock market and invest in stocks, even years and decades after German reunification. Years of exposure to emotional propaganda about the stock market as the pinnacle of capitalism, which serves only a few, seem to have left their mark.

Emotions, which affect our perceptions, also play another role. East Germans who had a fairly good life under communism—even according to nonfinancial measures, such as living in one of the celebrated communist showcase cities—are the most adamant about the harms of the stock market and capitalism. However, those who suffered under the communist regime—say from the severe air pollution in East Germany or religious oppression—were much more likely to embrace the post-communism market economy.

These concepts of experience effects appear to apply to almost any realm of life. Unemployment experiences leave scars and make consumers cautious even many years later when they have stable and high-paying jobs. Banks with failing capital ratios respond with higher capitalization than others. Lived experiences of returns in the bond market affect investment in bonds. Individuals with higher socioeconomic status tend to have a more optimistic economic outlook.

Inflation is another macroeconomic variable policymakers frequently examine. And, you guessed it, inflation experiences appear to meaningfully shape people’s beliefs and decisions regarding inflation. Research using more than 50 years of survey data on inflation expectations has documented that the average inflation people have observed during their lifetimes strongly predicts their actual inflation expectations. And those experience-based expectations affect important real-world outcomes—for example, the choice to buy a house. It turns out that inflation protection is a key motivation for choosing to purchase a home (rather than rent). As a result, people who have experienced higher inflation are more likely to choose homeownership over renting and a fixed-rate mortgage over one with an adjustable rate, again to protect against rising inflation (and interest) rates.

The reach of experience effects is even longer: One inflation puzzle observed by the Federal Reserve in the United States, and noted in many other countries, is that women consistently had higher inflation expectations than men. Experience effects solved this puzzle by documenting a critical difference in experience between men and women: grocery shopping. Only in households where the woman was the primary grocery shopper did women have higher inflation expectations than their male partners. Since food prices have faced higher inflation (or at least higher volatility—and we know from previous research that consumers latch on to upswings), people who shop for food have higher inflation expectations. As long as gender roles keep more women than men doing grocery shopping, their lived experiences will continue to differ—and so will their corresponding beliefs.

Policymaker biases

Even expert policymakers act as predicted by experience effects. (Policymakers have human brains, after all.) The inflation forecasts of the Federal Reserve Board of Governors tend to be biased toward their lifetime experienced inflation and away from expert analysts’ forecasts. And this bias makes the Federal Reserve governors' forecasts less accurate.

An extreme case is exemplified by Henry Wallich, who was raised during the hyperinflation in 1920s Germany and became a Federal Reserve governor in 1974. During his tenure, he dissented a record-breaking 27 times because he believed the Federal Reserve should be more concerned with inflation.

The four key features of experience effects that influence policymakers and laypeople are exactly the same:

- The long-lasting effects of experience

- Greater weight on more recent events

- Domain-specific experience effects

- The negligible effect of learned knowledge vis-à-vis experience-based beliefs, however distorted

Experience effects thus inform interventions and programs addressing crises in several important dimensions. First, policymakers typically face a trade-off between resolving crises quickly and the cost of doing so. The long-lasting ramifications of experience effects highlight the benefits of swiftly resolving a crisis. For example, the impact of the recent inflationary period on beliefs could affect how people respond to price swings for a long time. The shorter and milder the period, the weaker the long-term scarring. Conversely, the more traumatic the experience during crises, the longer they will haunt people—even years later—as we saw with the Great Depression.

Second, the evidence on experience effects implies that policymakers ought to account for the different experiences of their different target populations. The same intervention might yield vastly different responses depending on how past events have shaped people’s behavior and outlook. Ideally, any policy would be fine-tuned for each country-age-gender cohort or at least consider their different lifetime exposures.

Last, experience-based learning shapes policy support, offering a robust alternative to purely informational approaches. Direct engagement, such as through a pilot intervention, can affect preferences substantially more than theoretical explanations. The Affordable Care Act (ACA) in the United States provides an example. Individuals on government health insurance who had direct, immediate benefits were more likely to support the ACA. Initially skeptical Republicans were especially likely to become supporters, which highlights how experience can overcome partisanship. Pilot programs give policymakers a path to test new policies and gauge how public sentiment is affected. Positive personal experiences among pilot participants can foster and ensure enduring public support.

Podcast

Economists build models based on basic assumptions of human behavior. But people are complicated, right? Ulrike Malmendier is a behavioral economist whose innovative research has shown that experiential learning rewires the brain to make decisions based on past experiences. Malmendier and Journalist Rhoda Metcalfe discuss how behavioral economics is helping to build better economic models.

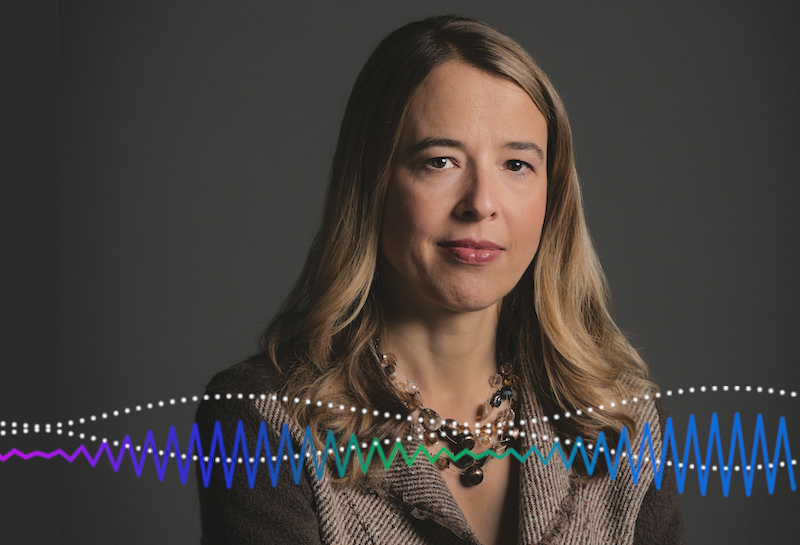

ULRIKE MALMENDIER is a professor of economics and finance at the University of California, Berkeley.

CLINT HAMILTON is a PhD student in finance at the Haas School of Business at the University of California, Berkeley.

Opinions expressed in articles and other materials are those of the authors; they do not necessarily reflect IMF policy.