Economic analysis can shine a revealing light on the causes and consequences of social unrest

The past decade was marked by a series of high-profile social protests—the Arab Spring, Black Lives Matter, the Gilets Jaunes, and Occupy Wall Street, to name just a few. Yet while there has been a lot of soul-searching about their causes and consequences, and even though many commentators have pointed their fingers at economic forces, the economics profession has been relatively slow to respond. Indeed, rigorous quantitative economic analysis of social unrest is scant, with evidence limited to isolated cases until recently. However, a new body of IMF staff research is filling this gap by analyzing the risks and economic costs of social unrest.

Measuring unrest

A key challenge when researching social unrest—defined as protests, riots, and other forms of civil disorder and conflict—is identifying when such events have occurred. Although sources of information are available, many are sporadic or are inconsistent in their coverage.

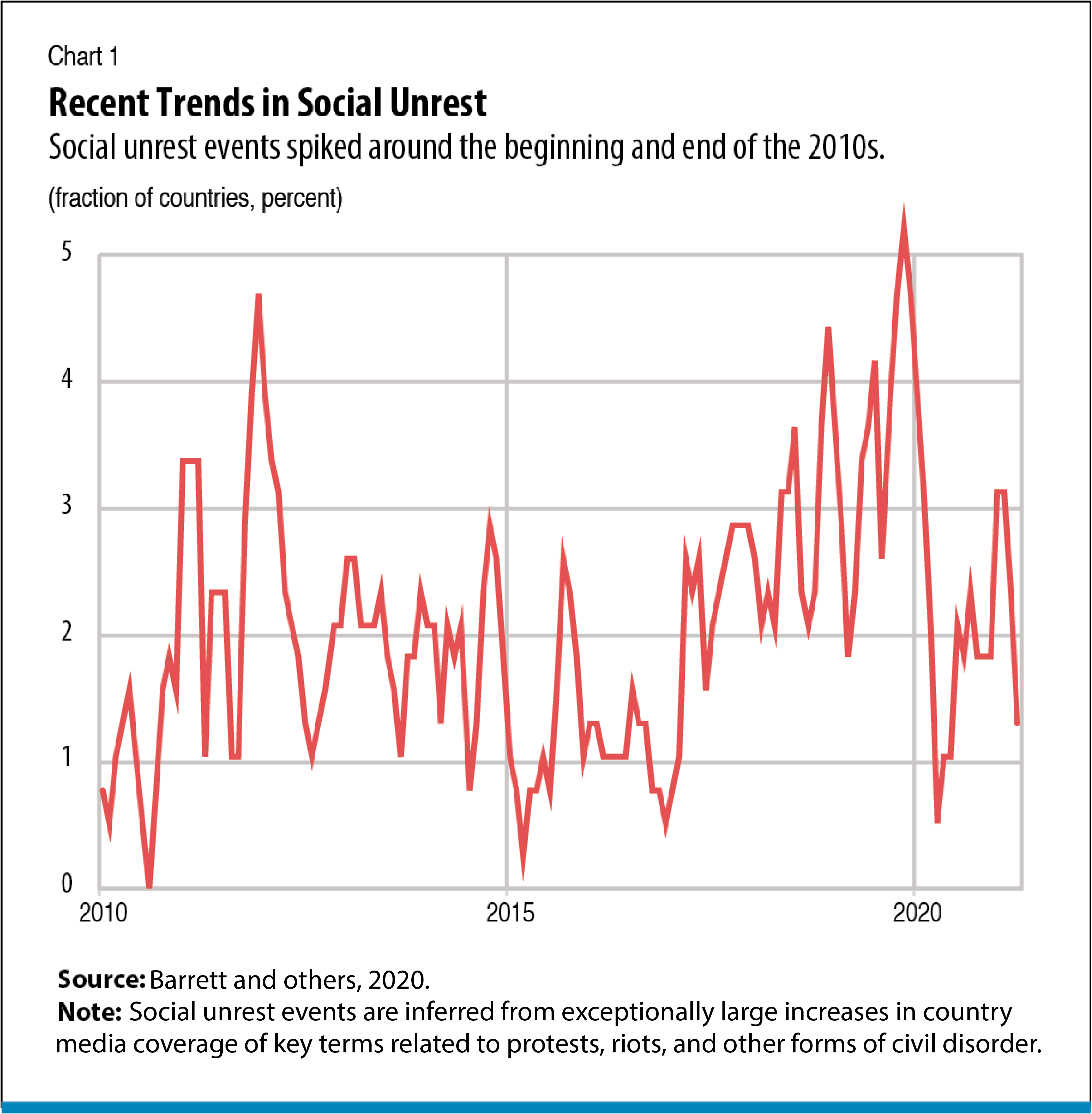

To address these shortcomings, we constructed the Reported Social Unrest Index, based on press coverage of social unrest (Barrett and others 2020). This provides a consistent, monthly measure of social unrest for 130 countries from 1985 to the present. Spikes in the index line up very closely with narrative descriptions of disorder in a variety of case studies, suggesting that the index captures real events rather than shifts in media sentiment or attention. Several pieces of IMF research, discussed further in this article, have since used this measure to analyze the causes and consequences of unrest.

This measure shows that major social unrest events are rare. The probability that a country will experience such an event in a given month is only 1 percent, on average. But this risk quadruples if a country has experienced a social unrest event within the previous six months and doubles if a neighboring country has.

More recently—at least prior to COVID-19—the frequency of social unrest events has increased. In late 2019, contemporaneous unrest in both South America and the Middle East drove the number of such events to its highest level in three decades. And although a combination of restrictions on activity and voluntary abstention from mass gatherings meant that unrest ceased almost entirely during the first wave of the pandemic, it remains to be seen whether it will reemerge as restrictions ease (see chart 1).

Economic causes

While we now have a solid picture of when social unrest occurs, identifying the underlying drivers is a more complex task. Economic factors such as inequality are often blamed, but they are likely just part of the reason. One case in point is that although inequality has crept up slowly in recent decades, it has not significantly worsened over the past decade in a way that would explain the recent surge of discontent.

To drill down on the causes, IMF economists Sandile Hlatshwayo and Chris Redl used machine learning techniques to assess the ability of more than 340 economic and social indicators to predict unrest (Hlatshwayo and Redl, forthcoming). A central finding is that past turmoil—both domestically and in neighboring countries—is by far the most important variable for predicting future strife. It is about 10 times as informative as the most revealing economic or social factors.

Although at first pass this might seem a little surprising, it is consistent with theoretical models of protests, which view coordination as a central driver of unrest. The intuition is that mass protests are more likely to have an impact than smaller ones. The resulting dynamics are thus highly unpredictable, with protests often growing when people think others will join in. This idea has much in common with a bank run, when people rush to withdraw deposits because they see others in line. As a result, factors signaling that others are more willing to protest—such as past protests or protest in culturally similar neighboring countries—can act as coordinating signals.

This is not to say that socioeconomic factors are irrelevant. Prices, particularly of food and fuel, seem to be particularly important. Other factors identified as predictive of unrest are digital access and social media penetration, suggesting that the ability to communicate and coordinate on a large scale might be essential to protest activity. Moreover, a history of domestic and neighboring unrest may not just be coordinating signals, but might also reflect long-standing and unresolved issues, such as a legacy of institutional racism.

Economic and financial consequences

Economic factors play a much more prominent role when it comes to the consequences of unrest.

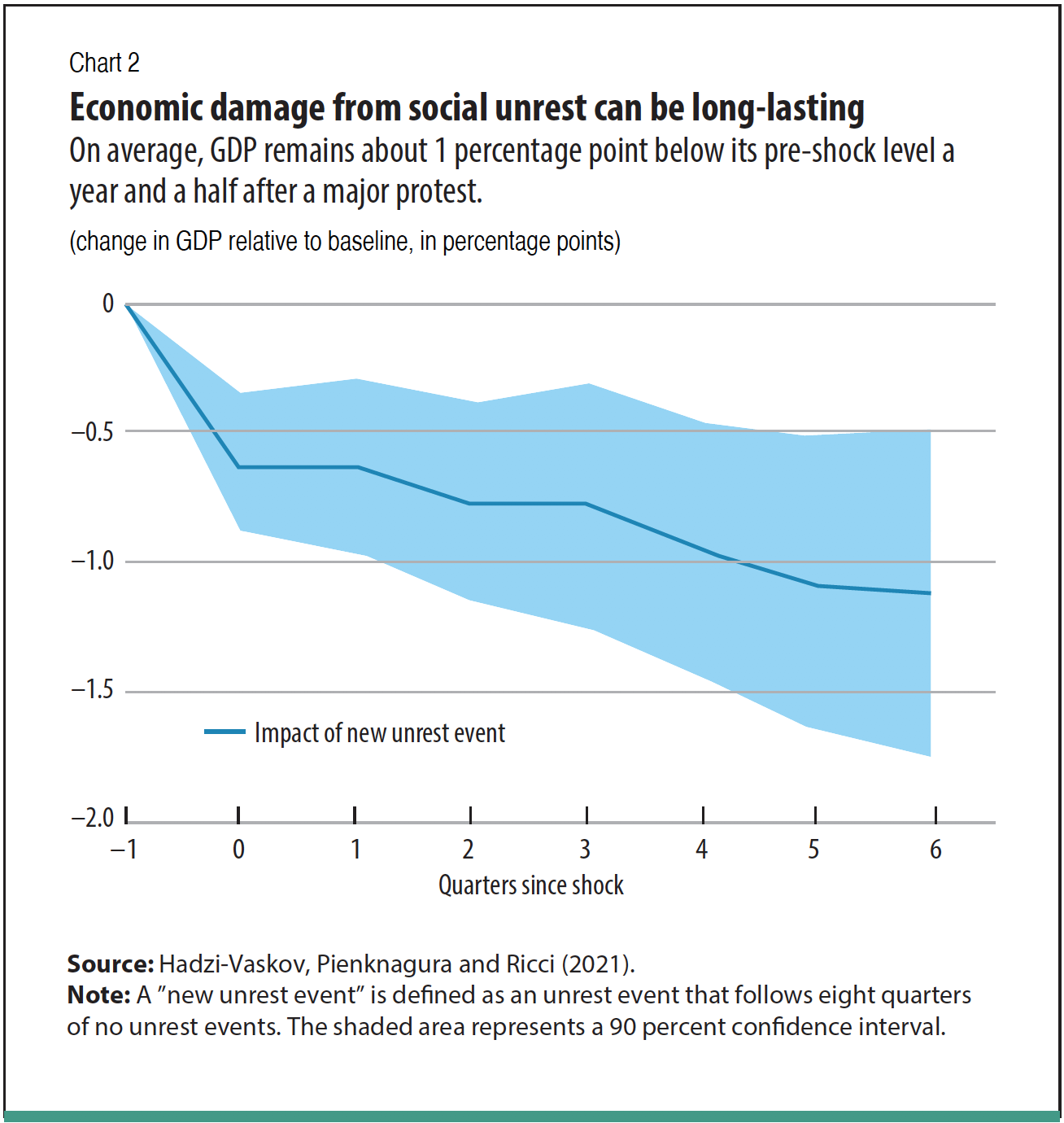

First and foremost, IMF economist Metodij Hadzi-Vaskov and colleagues find a tight link between unrest and subsequent economic performance (Hadzi-Vaskov, Pienknagura, and Ricci 2021). On average, major unrest events are followed by a 1 percentage point reduction in GDP six quarters after the event (see chart 2). Unrest motivated by socioeconomic factors is associated with sharper GDP contractions than unrest associated with political motives. Yet events triggered by a combination of both factors correspond to the sharpest GDP contractions.

Taken at face value, these results could mean one of three things: unrest impedes growth; unrest is caused by low growth; or unrest and low growth are both caused by something else, such as fiscal austerity. The first explanation is likely the most plausible because the link between unrest and growth holds regardless of whether the country was experiencing low growth or fiscal austerity prior to unrest.

The economic costs of unrest can also be measured by stock market valuations. Relative to macroeconomic indicators such as GDP, this measure can address concerns about the direction of causality, simply because the high frequency of stock market data leaves less time for other, slower-moving, factors to have an impact.

Because stock market valuations capture investors’ expectations about the future return of stocks, they also provide valuable insight into the future economic outlook. We examine 156 unrest events in 72 countries and find that stock market returns drop 1.4 percentage points on average after major unrest events (Barrett and others 2021b).

There is a further subtle point in this finding: in countries with more open and democratic institutions, unrest events have a negligible impact on stock market returns. But in countries with more authoritarian regimes, the effect is large and negative: on average, stock market returns fall 2 percent within three days and about 4 percent in the following month. This finding on the role of institutions is echoed in the research on growth mentioned earlier, which finds that stronger rule of law dampens the adverse effect of unrest on GDP.

Stock market data offer further clues about how unrest affects the economic outlook because the volume of shares traded increases sharply following unrest events. Because more trades occur when investors disagree on the value of an asset, higher trading volume typically reflects more uncertainty over the outlook. The evidence thus points to an indirect information channel rather than direct disruption to economic activity. In other words, in countries with high standards of governance, social unrest does not lead to more disagreement and uncertainty about the economic outlook in countries with open institutions, which perhaps reflects the ability to reconcile divergent opinions and find compromises. This flexibility may be missing in more authoritarian systems.

Unrest and pandemics

It is also timely to note that history is replete with examples of epidemics subverting social order and ultimately causing social unrest—the Plague of Justinian, the Black Death, and the 1830s cholera pandemic, to name just a few. One possible reason is that an epidemic can reveal or aggravate preexisting fault lines in society, such as inadequate social safety nets or a perception of government incompetence. It can also lead to a widening divide among different ethnic or religious groups or economic classes. Consistent with this notion of the social scarring effect of epidemics, we find that countries with more frequent and severe epidemics also experienced more unrest on average (Barrett and Chen 2021a).

On the other hand, social scarring in the form of unrest may not show up quickly. During and in the immediate aftermath of an epidemic, mitigating factors may prevail. For example, the disease outbreak may impede the transportation needed to organize major protests and dissuade crowds from gathering. Moreover, public opinion might favor cohesion and solidarity in times of duress. In some cases, incumbent regimes may also take advantage of an emergency to consolidate power and suppress dissent.

The COVID-19 experience is consistent with this historical pattern. The number of major unrest events worldwide has fallen to its lowest level in almost five years. Statistical analyses confirm a negative relationship between unrest and COVID-19–related lockdown across countries. When a country is in lockdown, the likelihood of major unrest is significantly lower.

There is no denying that COVID-19 has exposed or exacerbated many preexisting problems in our society. If history is a predictor, societal fault lines may sow the seeds of instability, and unrest may emerge after the pandemic fades. One thing is certain: economics can play an essential role in improving our understanding of social unrest—when it occurs, why, and its wider consequences.

PHILIP BARRETT is an economist in the IMF’s Research Department.

SOPHIA CHEN is an economist in the IMF’s Research Department.

References:

Barrett, Philip, Maximiliano Appendino, Kate Nguyen, and Jorge de Leon Miranda. 2020. “Measuring Social Unrest Using Media Reports.” IMF Working Paper 20/129, International Monetary Fund, Washington, DC.

Barrett, Philip, and Sophia Chen. 2021a. “Social Repercussions of Pandemics.” IMF Working Paper 21/021, International Monetary Fund, Washington, DC.

Barrett, Philip, Mariia Bondar, Sophia Chen, Mali Chivakul, and Deniz Igan. 2021b. “Pricing Protest: The Response of Financial Markets to Social Unrest.” IMF Working Paper 21/079, International Monetary Fund, Washington, DC.

Hadzi-Vaskov, Metodij, Samuel Pienknagura, and Luca Ricci. 2021. “The Macroeconomic Impact of Social Unrest.” IMF Working Paper 21/135, International Monetary Fund, Washington, DC.

Hlatshwayo, Sandile, and Chris Redl. Forthcoming. “Forecasting Social Unrest.” IMF Working Paper, International Monetary Fund, Washington, DC.

Opinions expressed in articles and other materials are those of the authors; they do not necessarily represent the views of the IMF and its Executive Board, or IMF policy.