Three Days at Camp David: How a Secret Meeting in 1971 Transformed the Global Economy

Jeffrey E. Garten

Three Days at Camp David:

How a Secret Meeting in 1971 Transformed the

Global Economy

HarperCollins, New York, NY, 2021,

448 pp., $23.99

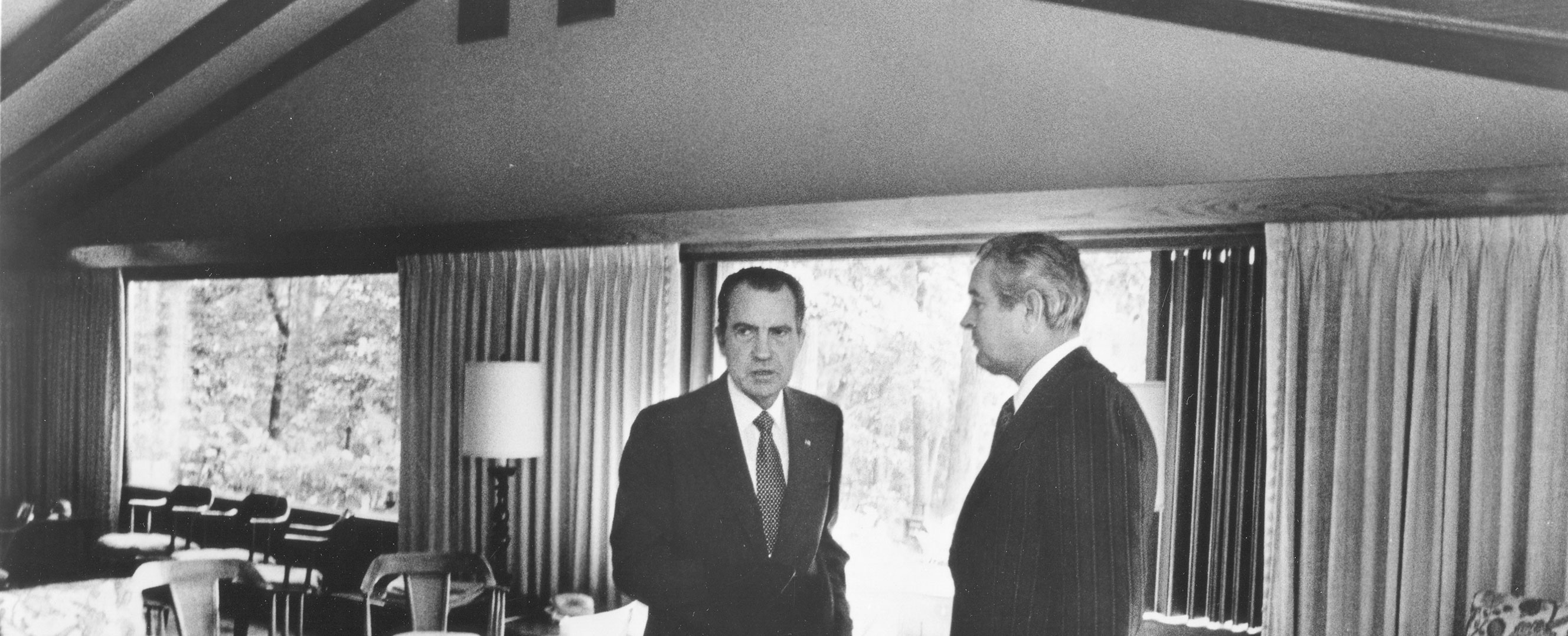

History is a confluence of underlying forces and specific triggering events. Think of the start of World War I: economic, imperial, and nationalistic tensions that had simmered for years exploded into open conflict when Archduke Franz Ferdinand’s motorcade took a wrong turn, putting him in the path of an assassin’s bullet. Less dramatic—but for international economists and officials at the time, no less momentous—was the collapse of the Bretton Woods system of fixed exchange rates in the early 1970s. While much has been written about the flaws of that system and the forces that made its demise inevitable, far less is known about the event that triggered that demise—President Richard Nixon’s decision to close the “gold window” on August 15, 1971. Jeffrey E. Garten’s superb account in Three Days at Camp David fills this gap.

When Bretton Woods was established, the United States promised to provide gold, on demand, in exchange for dollars accruing in foreign central banks. As the country ran balance of payments deficits during the 1960s, however, it began to deplete its gold stock. With US monetary gold falling to $10 billion (against $40 billion in liabilities), the situation became dire—prompting Nixon to summon his leading financial officials to a meeting at Camp David, the presidential retreat, over the weekend of August 13–15, 1971.

We meet key players—Nixon, Arthur Burns, John Connolly, Paul Volcker, George Shultz, and others—whose backgrounds, personalities, and preoccupations greatly influenced the outcomes at Camp David. Burns and Volcker worried about how foreign officials would react to closing the gold window. Connolly argued that doing so would help bludgeon the surplus countries into revaluing their currencies. Shultz, a student of Milton Friedman, favored floating exchange rates, which would make the whole issue moot, while Nixon cared less about foreign central bankers and worried only about the reaction of the American public.

Garten gives a detailed account of the discussions, chronicling how politician Nixon transformed the dominant narrative about shuttering the gold window: from a mea culpa that acknowledged the United States’ lax policies and abrogation of its international responsibilities, to one that proclaimed a triumphant fresh start for its place in the world, which went down well with his domestic audience.

Garten describes the aftermath, the short-lived Smithsonian Agreement, and relays an anecdote illustrating how sensitive officials were to any change in parities. When Connolly pressed the Japanese finance minister to revalue the yen by 17 percent, he refused, on the grounds that a 17 percent revaluation during the interwar period had resulted in the then–finance minister’s assassination. Connolly, who was in the car during President John F. Kennedy’s assassination (and had himself been shot), accepted a 16.9 percent revaluation. (In fact, the Japanese prime minister had pre-authorized up to a 20 percent revaluation.)

It would be trite to say that Garten’s book belongs on every international economist’s bookshelf. It doesn’t. It belongs on their bedside tables as light, but thoroughly enjoyable, reading and a useful reminder that, whatever economic forces might be at play, it is people, personalities, and politics that make history.

ATISH REX GHOSH, IMF historian

Opinions expressed in articles and other materials are those of the authors; they do not necessarily represent the views of the IMF and its Executive Board, or IMF policy.