Value chains transform manufacturing—and distort the globalization debate

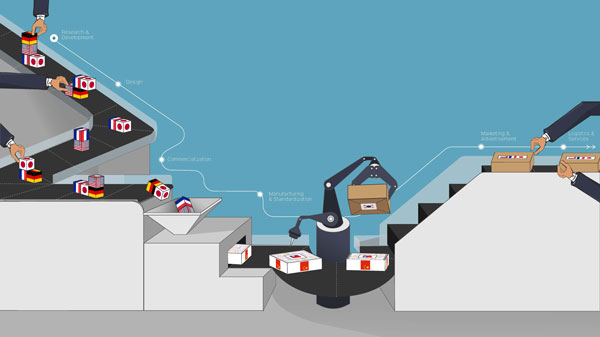

Walk into a Toyota dealership in New York or Munich, and you might think you are looking at cars made in Japan. You would be mistaken. In fact, the 15,000 components that make up a modern car are often produced by different firms in different locations. There are three main hubs for auto production—North America, Europe, and east Asia. Research and development and design mostly take place in Germany, Japan, and the United States, with China starting to play a significant role as well, given the 5 million STEM (science, technology, engineering, and mathematics) graduates it trains each year. Each of these hubs combines production in high-wage economies with parts and components from lower-wage, emerging market economies. Parts and components crisscross multiple borders during the production process.

From smartphones and autos to TVs and computers, more than two-thirds of international trade now takes place within such global value chains. That’s up from 60 percent in 2001. The rise of value chains has reshaped the world economy, fueling dramatic advances in living standards in emerging-market economies like China and Vietnam, where labor costs are relatively low, while widening income inequality in advanced economies, including the United States. Yet decades-old methods of gathering trade data, developed in the pre-value-chain world, fail to reflect this transformation, giving rise to a skewed picture of the movement of goods and services around the world. The result: acrimonious debates over job losses blamed on trade are rooted in inadequate data, amplifying misguided calls for protectionism.

Take the case of a smartphone exported by China. When it is shipped to the United States, official trade statistics record its full value as an import from China. But research on value chains, such as the Global Value Chain Development Reports, published by the World Trade Organization and the World Bank, shows that it would be more accurate to say the United States imports different types of value added from different partners, including labor- intensive assembly from China and more sophisticated manufacturing inputs from South Korea. That is because official trade statistics measure the gross value of trade, not the value added at each link in the chain. What is more, official statistics don’t capture the growing importance of services, such as computer coding, logistics, and marketing, that are contained in the value of manufactured goods. Much of the value added in a nominally Chinese-made smartphone, such as computer coding and marketing, originates in the United States and other advanced economies. Viewed from this value-added perspective, bilateral trade imbalances look quite different. The contentious US trade deficit with China, for example, is roughly cut in half when the analysis shifts from gross value to value added because China tends to be at the end of many value chains.

Growth driver

Global value chains have been a boon to developing economies because they

make it easier for them to diversify away from commodities toward

higher-value-added manufactured goods and services. How? By breaking up the

production process so that different steps can be carried out in different

countries. In the past, a country had to master the production of a whole

manufactured product to export it, which rarely happened. With value

chains, a country can specialize in one or several activities in which it

has a comparative advantage. The phenomenon has enabled China to export

nominally high-tech products even though its role has been largely that of

assembler. The unbundling of production started within advanced economies

in response to competition and declining logistics costs and then went

global as big developing economies opened up.

The global value chain for China’s 2009 exports of electrical and optical equipment—a category that includes smartphones, tablets, and cameras—illustrates the country’s role . The vertical axis shows worker compensation per hour, a measure of value added. The horizontal axis maps the steps in the production process, starting with high-value design and financial inputs from advanced economies. Then come sophisticated parts such as computer chips from Japan, the United States, South Korea, and Taiwan Province of China. China adds value toward the end of the chain with production of some simple parts and assembly. China also has many so-called backward linkages to domestic sectors such as metal and plastic manufacturing, which contribute to the production process prior to assembly. Finally, at the end of the chain come high-value inputs consisting mostly of services such as marketing as products are sold in the United States, Europe, and Japan. In the case of exports of these products to the United States, China contributes almost half the value added. The country’s considerable share of value added has provided jobs for large numbers of low-skilled workers, helping drive economic growth and reducing poverty. So breaking up the production process enabled many labor-intensive activities to settle in China, enhancing the country’s ability to exploit its comparative advantage.

Vietnam is another emerging market economy deeply involved in global value chains. Following its market-oriented reforms and opening to global trade starting in the late 1980s, Vietnam attracted major investments by foreign firms, such as Korea’s Samsung, seeking a low-cost locale for labor-intensive assembly. Policymakers in Vietnam worry that they will be stuck with only low-end assembly, but analysis of the production chain shows that there are extensive backward linkages; that is, many firms sell to exporters but are not exporters themselves. In 2012, about 5 million Vietnamese worked for firms that manufactured for export; the number working in firms that sold to exporters was much higher at 7 million . These linkages have important implications for policy. Although developing economies maintain higher barriers to imports than advanced economies, they recognize that their exporters need access to the best imported inputs if they are to be competitive globally. Many solve that problem by creating special economic zones where exporters have duty-free access to imported parts. Shenzhen, China, is a classic example. However, it would be much better to liberalize the entire economy so that indirect exporters and producers of goods sold domestically also have access to the best inputs.

Advanced economy impact

The growth of global value chains also benefits advanced economies, which tend to concentrate on high-value-added activities such as advanced technology, financial services, sophisticated manufacturing components, and marketing and servicing. Still, there are winners and losers. Studies have found that the United States has lost middle-skill manufacturing jobs because of trade with China and economies contributing to its value chains, while gaining jobs in high-skill manufacturing and in services, leaving total employment largely unchanged. College-educated American workers have seen their salaries rise, while those without a college education have seen wages decline.

The impact wasn’t limited to the United States. Between 1995 and 2015, when emerging market and developing economies were opening to the expansion of trade and value chains, advanced economies saw increases in high- and low-skill jobs and declines in middle-skill employment . This was not all the result of trade; many studies emphasize the dominant role of technological change. Middle-skill jobs involving routine, repetitive tasks have been the easiest either to automate or move to lower-wage countries, allowing employers to cut costs. The activities remaining in advanced economies have been more technology-and skill-intensive. In addition, many low-skill jobs in construction, health care, and hospitality have been difficult to automate or outsource.

The perceived distributional consequences of expanding trade and value chains are driving the backlash against globalization and prompting calls for trade barriers in rich countries. But protectionism was a bad strategy before the rise of global value chains, and it is a worse strategy now. Take, for example, the tariffs the United States imposed on China in 2018—25 percent on $50 billion in imports and 10 percent on $200 billion in additional imports. Parts and components comprise 37 percent of US imports from China, and the list of products taxed seems to have been even more heavily weighted toward these items, which US firms use to be more competitive. The cost of the tariffs was passed on to US firms, which lost sales as a result. That was the case even before Chinese retaliation imposed additional losses on US exporters. In a world of complex value chains, it is hard to predict the precise impact of import tariffs, but it is safe to say that some firms and workers in the protectionist country will be hurt, and the net effect will be negative.

Rather than trying to hold back progress, public policies should seek to ease the adjustment for displaced workers. Distinguishing between job losses resulting from trade and technology does not make sense when designing safety nets to help workers and communities affected by change. Some advanced economies have adjusted better to the forces of globalization than others. In Germany, for example, because of progressive taxation and a strong safety net, there has been little change in inequality as measured by its Gini coefficient calculated after taxes and transfers. In the United States, on the other hand, there has been a significant increase in inequality because public policy has exacerbated the market trend toward job and wage polarization through regressive tax cuts.

Shifting perspective

Official statistics tell us that about 80 percent of world trade consists of manufactured goods and primary products such as food, oil, and minerals, with the remaining 20 percent consisting of services such as tourism, overseas college education, and international finance. This ratio has changed little in 40 years. The picture looks very different when the analysis shifts to value added in trade. The share of services in trade, measured in value-added terms, rose by more than a third from 1980 to 2009—from 31 percent to 43 percent. This means that the services content in merchandise was increasing. Some of the increase reflects the growing use of software. Moreover, managing global supply chains involves relying more on services such as transportation, finance, and insurance. A final factor is that prices of services have risen, while manufacturing prices have declined because of the sector’s more rapid productivity growth.

In every major economy, the share of services in trade is larger in value-added terms than in gross value terms. Among the 34 economies in the Organisation for Economic Co-operation and Development, services account for about half of value added in exports. For emerging market economies that are well integrated into global value chains, such as Mexico, China, Vietnam, and Thailand, the proportion is about 40 percent. In addition, advanced economies use a lot of imported services in their production chains. This is less true for developing and emerging market economies because they tend to have greater restrictions on imports of services and on foreign direct investment in service industries. Recent research has shown that using imported services enhances manufactured exports of emerging market economies, because access to the best inputs in the world improves productivity.

Developing economy lessons

The rise of global value chains does not fundamentally change trade theory, but it does provide a more complex picture. Breaking up the production process offers new opportunities for integration of rich and poor economies, with potential benefits for each—but with homework as well. I have mentioned some of the emerging market economies that are deeply involved, but large parts of the developing world are left out. Globalization is like a fast train, and you need a platform to get it to stop at your location. Building the platform requires all the basic elements markets depend on: rule of law, infrastructure, education, and health care. Developing and emerging market economies that have succeeded even moderately well have seen impressive economic growth and poverty reduction.

For rich countries there is an analogous challenge: integration and innovation spur change in employment and wages, creating winners and losers. It is tempting to use protection to try to slow or reverse these changes. But total isolation will cut you off from the dynamic global economy, and partial protection will benefit some firms at the expense of other firms, while also hurting consumers. With the complexity of modern value chains, it is impossible to fine-tune trade policy to help a geographic region or group of workers. It is better to concentrate on easing the adjustment as production and jobs naturally evolve.

For rich and poor countries alike, free trade is the best policy. The world has achieved reasonably free trade in manufactures, at least until the recent bouts of protectionism. But there are greater restrictions on trade and investment in services, especially in the developing world. Given their growing role in production and value chains, services are a logical next focus of liberalization.

DAVID DOLLAR is a senior fellow in the John L. Thornton China Center at the Brookings Institution.

Opinions expressed in articles and other materials are those of the authors; they do not necessarily reflect IMF policy.