The main entrance of the headquarters of the central bank of Serbia. Serbia was one of several emerging European economies to deploy asset purchases during the pandemic. (photo: BalkansCat by Getty Images)

How Emerging European Economies Found a New Monetary Policy Tool

September 29, 2021

The purchase of government bonds by emerging market central banks may be reminiscent for some of the days of monetary financing of the government, which was often followed by rising inflation and currency depreciations. However, the successful actions by several central banks in emerging Europe to buy government bonds during the COVID-19 pandemic countered this history.

Related Links

Amid the financial market turmoil at the start of the pandemic, central banks in Croatia, Hungary, Poland, Romania, Serbia, and Turkey rolled out asset purchase programs (APPs), buying up local currency bonds issued by governments but also by the private sector in the case of Hungary. New IMF research suggests that asset purchases in emerging Europe contributed to the relief of financial market dysfunction, without signs of destabilizing effects. With this goal achieved and to support the transmission of higher policy rates to the longer end of the yield curve, central banks in emerging Europe should taper or end asset purchase programs once monetary policies are tightened.

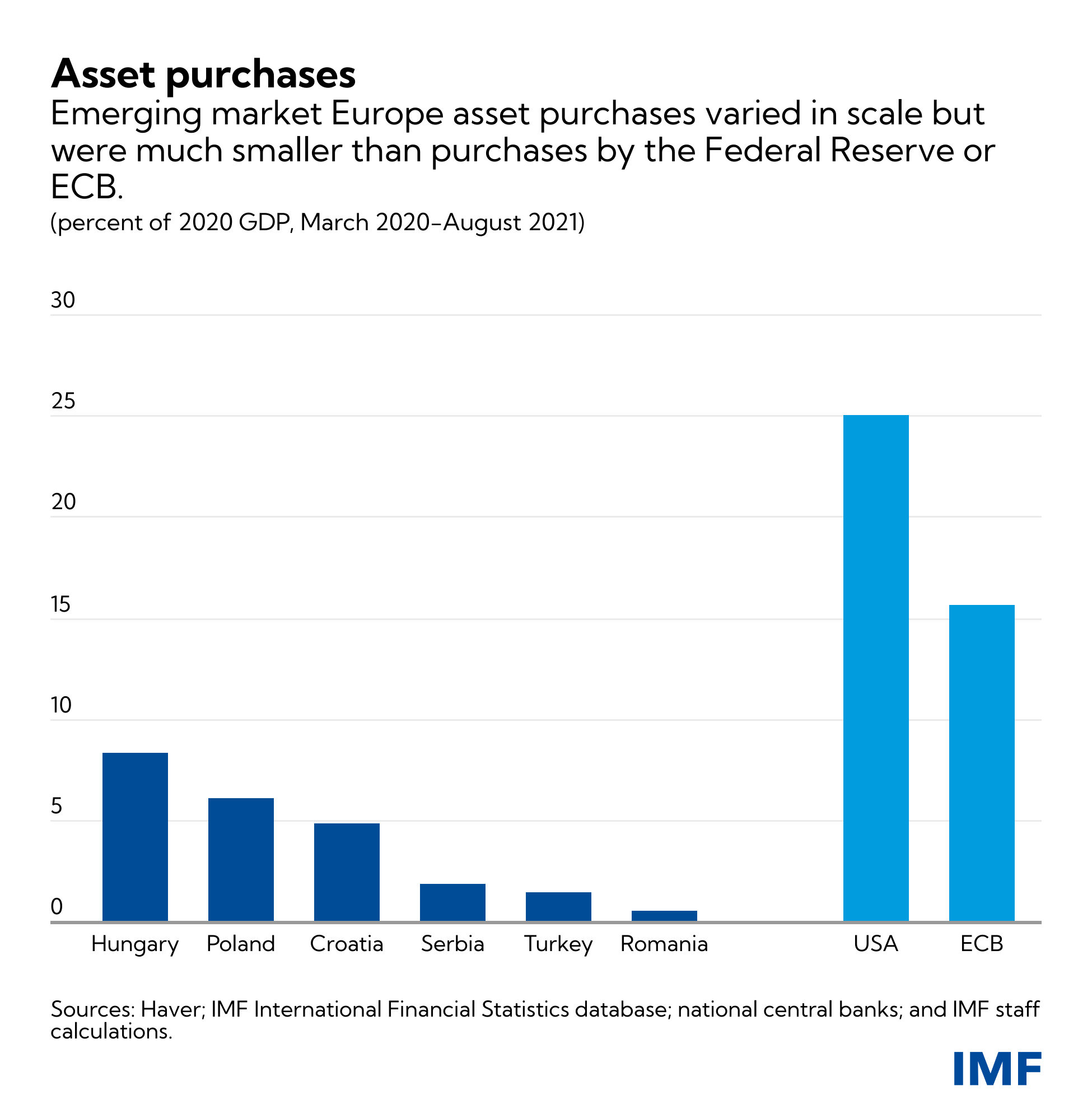

Asset purchase programs in emerging Europe are distinct

Compared to APPs employed by advanced economy central banks during the pandemic, most APPs in emerging Europe were smaller in scale, though with significant differentiation within the region. They were also generally limited to the immediate period following the onset of the pandemic, except in Hungary and Poland, where asset purchases continue.

The limited scale and duration of these APPs is consistent with their goals, which was to mitigate financial market dysfunction, provide liquidity, and repair monetary policy transmission mechanisms. This sets these APPs apart from the quantitative easing employed by advanced economy central banks, which aimed to provide additional stimulus in the context of policy interest rates at or near the effective lower bound. Indeed, APPs in emerging Europe were mostly implemented alongside or even preceded conventional monetary policy easing. For example, Romania’s asset purchase program essentially concluded during the summer of 2020, but the policy interest rate only reached its low of 1.25 percent in January 2021.

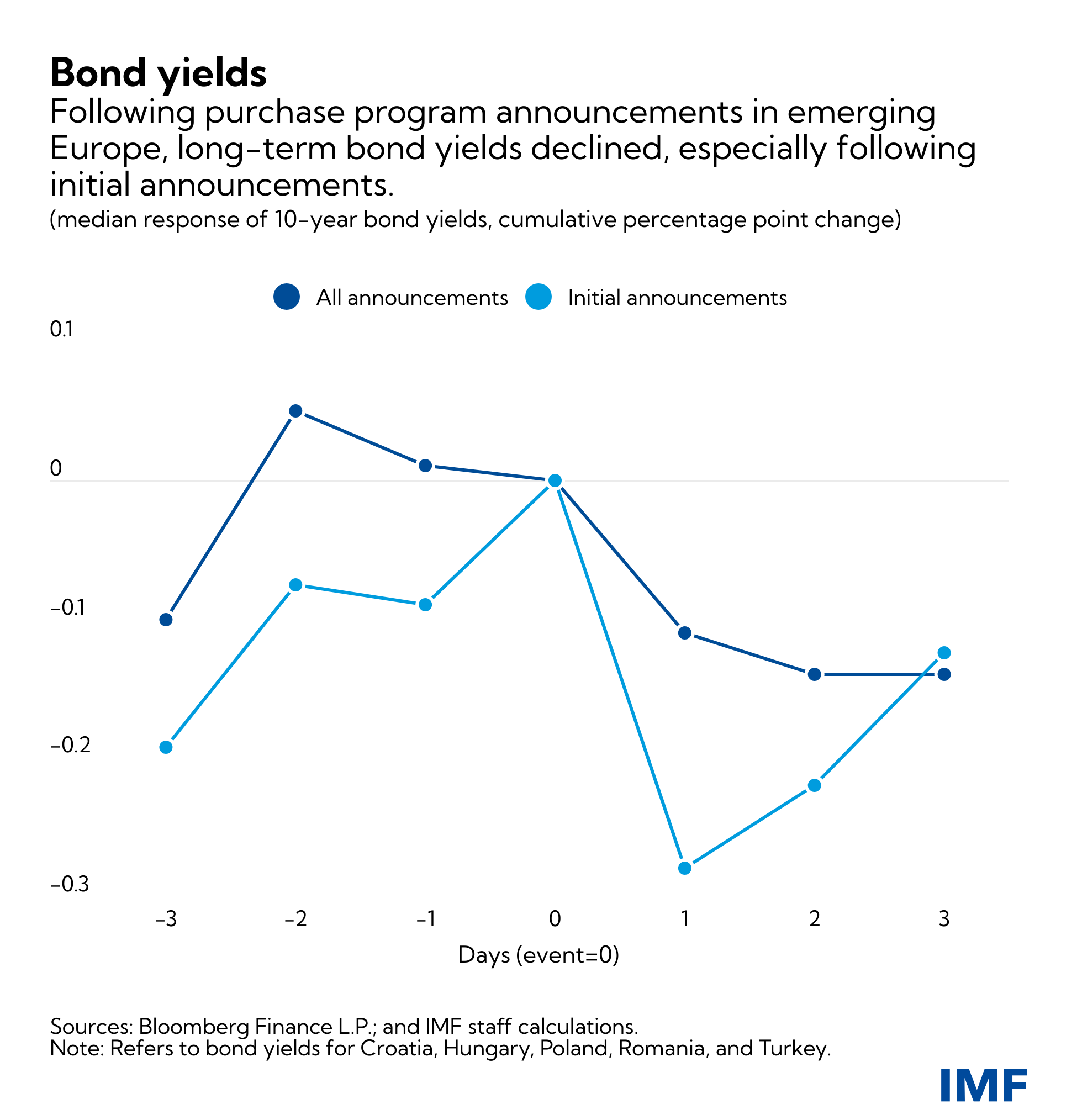

Asset purchase programs reduced bond market pressures

IMF research suggests that APPs in emerging Europe were successful in alleviating market dysfunction in the immediate aftermath of the pandemic shock. Using an event study approach, we find evidence that APP announcements led to an easing of bond market liquidity pressures and a reversal in the surge in term spreads.

Importantly, we found no evidence that these APPs led to currency pressures. This may reflect their mostly limited duration and scope. In countries where APPs were more extensive or prolonged, the actions by central banks to absorb the added liquidity created by these purchases may have also played a role in minimizing the impact on exchange rates. For example, the central bank of Poland issued its own securities, while the central bank of Hungary used a deposit facility to drain liquidity created by purchases.

Tapering or discontinuing remaining asset purchase programs

After successfully alleviating initial market dysfunction, most APPs in the region have already concluded. For ongoing APPs in Hungary and Poland, central banks should consider the goals and their role in monetary policy tightening, which has already begun in Hungary. Increases in policy rates should be accompanied by a tapering or discontinuation of APPs, which would support the transmission of higher policy rates to the longer end of the yield curve.

In August, the National Bank of Hungary announced that it would begin to gradually reduce its purchases of government bonds. While the National Bank of Poland has not yet raised interest rates, the pace of purchases has slowed significantly from the spring months.

The future role of asset purchase programs

While APPs in emerging Europe were successful during the pandemic and now appear to be part of the toolkit, less clear are the conditions in which to use them in the future. In part, their use may depend on global circumstances. It is important to recognize that the nearly universal easing of monetary policies during the pandemic created more conducive conditions for EMs to employ such tools. It remains to be seen whether APPs could be employed by EMs in response to idiosyncratic shocks without triggering reactions such as currency depreciation.

Country fundamentals also matter. One concern about APPs in EMs is that they could abet fiscal dominance if they help support deficits that cannot be financed by conventional means. A strong track record of macroeconomic stability and credible economic institutions are likely to mitigate concerns about fiscal dominance. To this end, the structure and discipline provided by EU membership make these risks less acute, potentially enhancing future scope for APPs in these countries.