Ghana: IMF Program Helps Restore Luster to a Rising Star in Africa

May 2019

Ghana has been hailed as one of sub-Saharan Africa’s success stories. It was the first to free itself from colonial rule, in 1957. It built a stable democracy in the 1990s, overcoming decades of political upheaval. A thriving economy fueled by exports of cocoa, gold, and—more recently—oil helped cut the poverty rate from 53 percent in 1991 to 21 percent in 2012.

But by 2015, Ghana’s economy was in trouble, hobbled by widening current account and budget deficits, rampant inflation, and a depreciating currency. Credit dried up as interest rates rose and banks’ bad loans piled up. At the root of Ghana’s woes was out-of-control government spending, largely to pay salaries of an overgrown civil service.

The program

In early 2015, Ghana turned to the IMF for a $918 million loan to help stabilize the economy. IMF advisors, working with the Ghanaian government, developed a three-part program:

- Restore debt sustainability. The government limited hiring and wage increases and eliminated subsidies for utilities and petroleum products. To raise revenue, it cracked down on tax evasion and rationalized exemptions. New revenue sources included a tax on luxury cars and increased taxes on high earners. To put Ghana’s finances on a sounder footing, the new Public Financial Management Act called for improved accounting standards, procedures, and technology.

- Strengthen monetary policy. The authorities agreed to gradually end central bank financing of the budget deficit—a major source of inflation—and to fortify the inflation-targeting regime.

- Clean up the banking system. An asset quality review revealed significant under-capitalization. Some banks were recapitalized, and the Bank of Ghana used its newly enhanced authority to wind down insolvent lenders. The central bank developed regulations to ensure that banks meet sound underwriting and credit evaluation standards. It also paid back insolvent microfinance institutions’ depositors.

The outcome

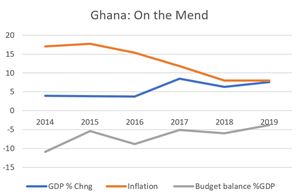

Ghana’s economy is on the mend. The trade and budget deficits are narrowing. The pace of economic growth is poised to rise to 8.8 percent in 2019 from 2.2 percent in 2015. The inflation rate is projected to fall to 8 percent from almost 19 percent. Cuts to wasteful spending made room for much needed social services, such as free secondary education. For Ghana’s 28 million people, it all adds up to higher incomes, better job opportunities, and more purchasing power. Still, Ghana remains largely reliant on foreign financing, exposing it to swings in investor sentiment. Maintaining fiscal discipline will also be a challenge.