It’s fitting that G20 finance ministers and central bank governors will meet this week at Sao Paulo’s Biennale Pavilion, designed by famed architect Oscar Niemeyer. With its flowing lines and striking façade, it is a monument to the boldness of modern Brazil.

I hope the G20 takes inspiration from this landmark to act boldly, too. With recent improvement to the global-near term outlook, G20 policymakers have an opportunity to rebuild policy momentum, setting their sights on a more equitable, prosperous, sustainable, and cooperative future.

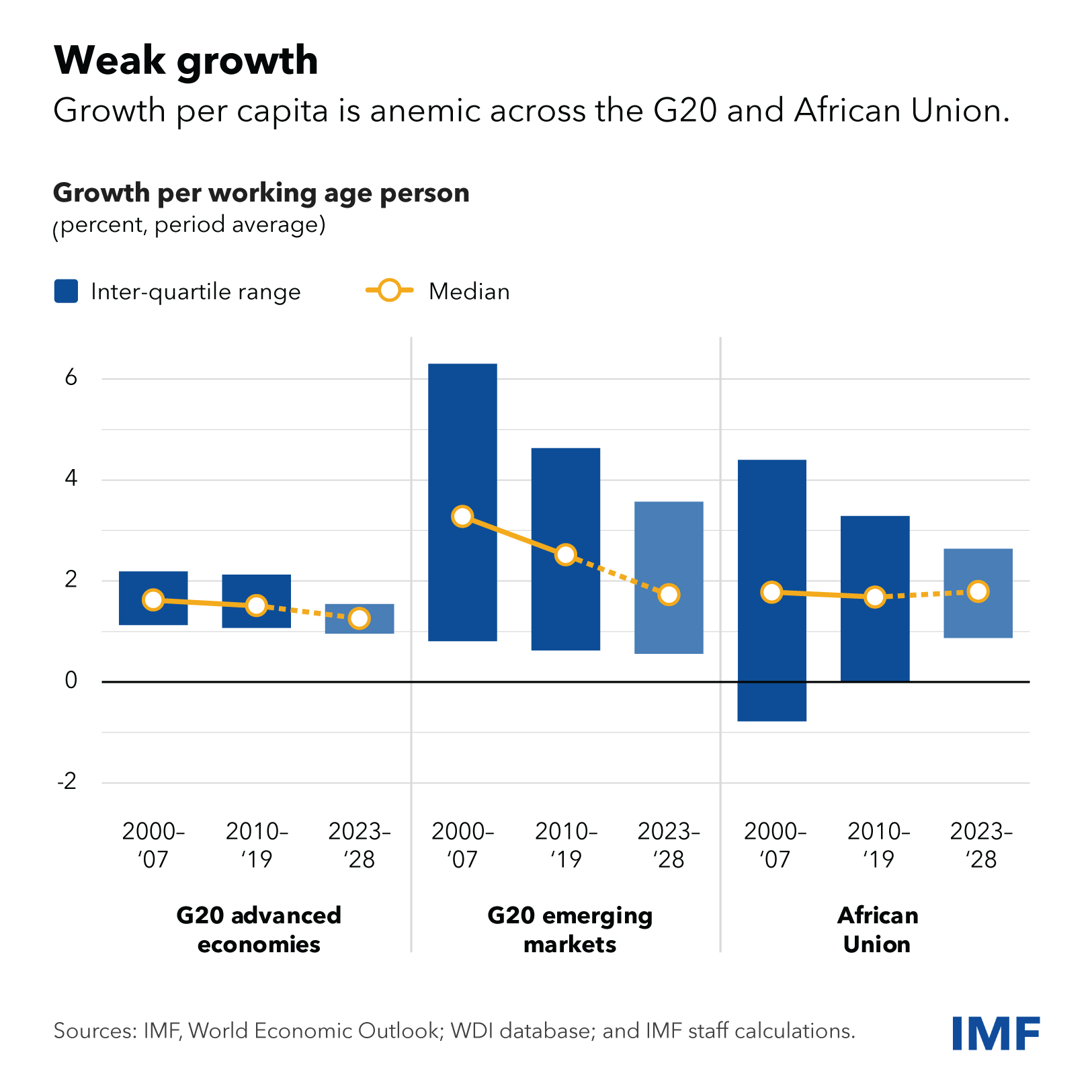

After several years of shocks, we expect global growth to reach 3.1 percent this year, with inflation falling and job markets holding up. This resilience provides a foundation to shift focus to the medium-term trends shaping the world economy. As our new report to the G20 makes clear, some of these trends—such as AI—hold promise to lift productivity and improve growth prospects. We badly need it—our projections for medium-term growth have declined to the lowest in decades.

Low global growth affects everyone, but has particularly troubling implications for emerging-market and developing economies. These countries impressively weathered successive global shocks, supported by stronger institutional and policy frameworks. But their slowing growth prospects have made convergence with advanced economies even more distant.

Other factors contribute to the complex global picture. Geoeconomic fragmentation is deepening as countries shift trade and capital flows. Climate risks are increasing and already affecting economic performance, from agricultural productivity to the reliability of transportation and the availability and cost of insurance. These risks may hold back regions with the most demographic potential, such as sub-Saharan Africa.

Against this backdrop, Brazil’s G20 agenda highlights key issues such as inclusion, sustainability, and global governance, with a welcome emphasis on eradicating poverty and hunger. This ambitious agenda, which the IMF is working to support, can guide policymakers at this pivotal moment in the global recovery.

Finishing the Job on Inflation

Central bankers are rightly focused on finishing the job of bringing inflation back to target. That’s especially important for poor families and low-income countries who have been disproportionately hit by high prices. But the welcome progress on reducing inflation means that the question of when and how much to ease interest rates will need to be carefully considered by major central banks this year.

As core inflation remains elevated in many countries, and upside risks to inflation remain, policymakers must carefully track underlying inflation developments and avoid easing too soon or too fast.

But where inflation is clearly moving toward target, countries should ensure that interest rates are not kept high for too long. Brazil’s early and resolute response to surging inflation during the pandemic is a good example of how nimble policymaking can pay off. The Central Bank of Brazil was among the first central banks to raise its policy rate, then loosen policy as inflation fell back toward its target range.

Tackling Debt and Deficits

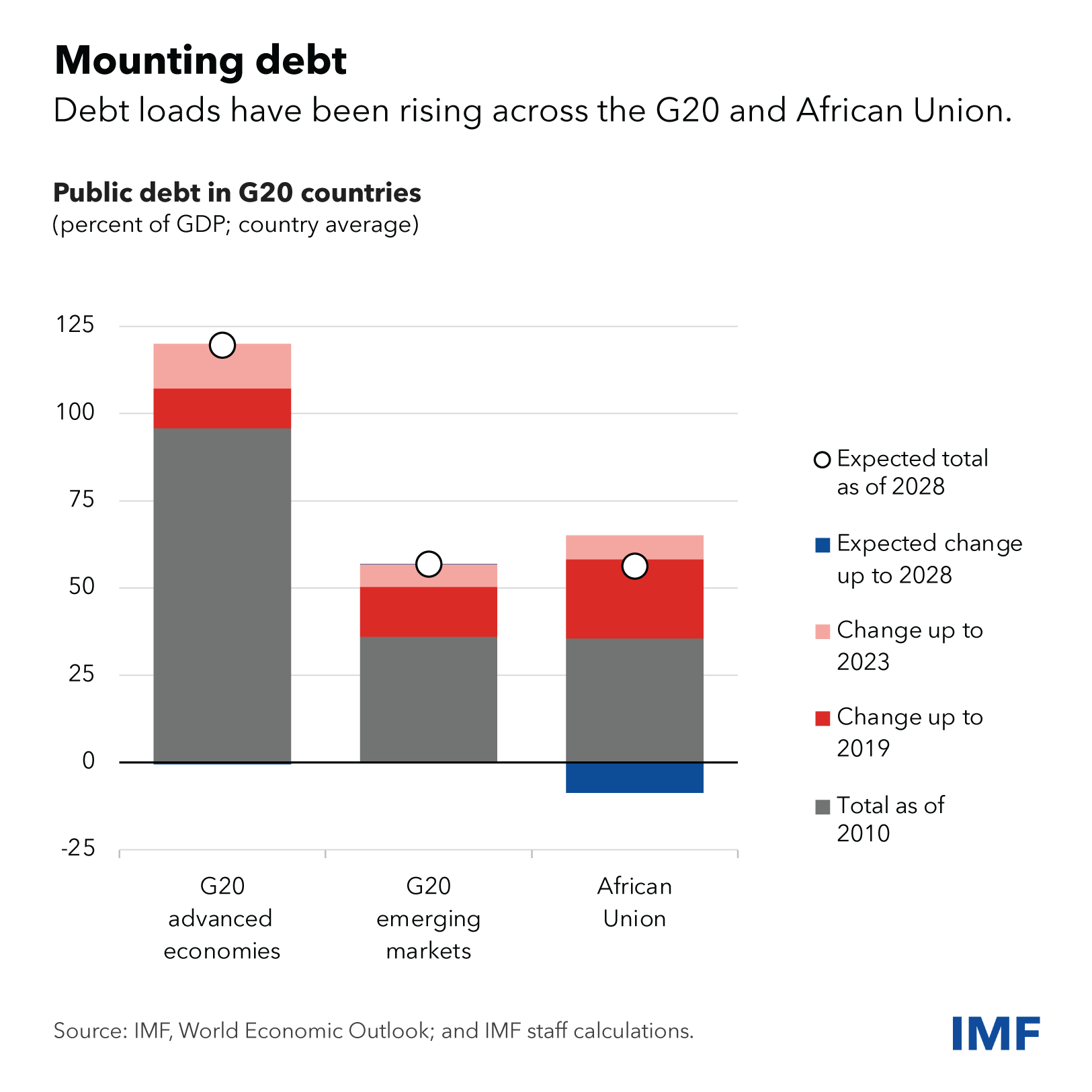

With inflation cooling and economies better placed to absorb a tighter fiscal stance, the time has come for a renewed focus to rebuild buffers against future shocks, curb the rise of public debt, and create space for new spending priorities. Waiting could force a painful adjustment later. But, for the benefits to be durable, tightening should proceed at a carefully calibrated pace.

Finding the right balance is tricky, with higher interest rates and debt-servicing costs straining budgets—leaving less room for countries to provide essential services and invest in people and infrastructure. Any push to bring down debt and deficits should be grounded in credible medium-term fiscal plans. It should also include measures to minimize the impact on poor and vulnerable households while protecting priority investments.

It’s also vital for countries to continue making important strides in raising revenue and weeding out inefficiencies. Brazil has shown leadership in this area with its historic VAT reform. But many countries are lagging, with scope to broaden their tax base, close loopholes, and improve tax administration. This is why the G20 has asked us to launch a joint initiative with the World Bank to help countries boost domestic-resource mobilization.

In addition, countries should aim to build more inclusive and transparent tax systems, ensuring the international tax architecture takes into account the interests of developing countries.

Our work also continues under the Global Sovereign Debt Roundtable to come up with procedures to speed debt restructurings and make them more predictable. While progress has been made under the G20 Common Framework, with agreements on debt treatment by official creditors taking less time, faster improvements to the global debt-restructuring architecture may be required.

Growing the Economic Pie

Alongside monetary and fiscal measures that lay strong foundations, policymakers urgently need to address the drivers of medium-term growth.

In many countries, there are still opportunities to ease the most binding constraints to economic activity. For emerging-market economies, reforms in areas such as governance, business regulation and external sector policies could unleash productivity gains. But that’s only part of the story: economies must also prepare to harness structural forces that will define the coming decades.

Take the new climate economy. For some countries and regions, it will bring jobs, innovation, and investment. For those heavily reliant on fossil fuels, it could be more challenging. The question is how to maximize the opportunities and minimize the risks.

Policies to make polluters pay—such as carbon pricing—can create incentives to shift to low-carbon investments and consumption. IMF research shows that countries that take action on climate tend to stimulate green innovation and attract inflows of low-carbon technology and investment. Also, taxing the most polluting forms of international transportation could raise revenues that can be used to fight climate change, hunger and support the most vulnerable members of the population.

For many vulnerable countries, however, stronger growth alone will not be enough to realize their potential—they will need external support, both financial and technical.

This points to the importance of an international architecture that can meet the changing dynamics of the global economy.

A Stronger International System

As recent military conflicts have laid bare, we live in an increasingly polarized world. The tensions are fragmenting the global economy along geopolitical lines—around 3,000 trade-restricting measures were imposed in 2023, nearly three times the number in 2019. No country stands to gain from the splintering of the world economy into blocs. Restoring faith in international cooperation is critical.

In the eight decades since its founding, the Fund has continually evolved to meet the needs of its membership. Since the pandemic, we have deployed $354 billion in financing to 97 countries, including 57 low-income countries. With countries likely to face larger and more complex crises, countries must work together to reinforce the global financial safety net, with the IMF at its core.

Last year, our shareholders gave us a strong vote of confidence. Among other measures, they stepped up to meet our fundraising targets for the Poverty Reduction and Growth Trust, which provides interest-free loans to low-income countries. And our shareholders agreed to increase our permanent quota resources by 50 percent. G20 countries can lead the way by quickly ratifying the quota increase, which will allow us to maintain our lending capacity and reduce our reliance on borrowed resources.

But we can—and must—do more. Our membership also recognized the importance of realigning quota shares to better reflect members’ relative positions in the world economy, while protecting the voices of the poorest members. With that goal in mind, we are developing possible approaches to realignment, including through a new quota formula. This comes in addition to a third chair for Sub-Saharan Africa on our Executive Board for election at this year’s Annual Meetings—an important step that complements the African Union’s new status as a permanent member of the G20.

In the years ahead, global cooperation will be essential to manage geoeconomic fragmentation and reinvigorate trade, maximize the potential of AI without widening inequality, prevent bottlenecks on debt, and respond to climate change.

As Oscar Niemeyer once said, “architecture is invention.”

The founding of the global economic and financial architecture was a courageous feat of collective invention that lifted the lives of millions. Now the challenge is to make it stronger, more equitable, more balanced, and more sustainable, so millions more can benefit. To reach that goal, we must channel that inventive spirit once again.