The damage from the 2011 floods in Thailand amounted to around 10 percent of Thailand’s GDP, not even considering all the indirect costs through a loss in economic activity in the country and abroad. By some estimates, the total costs of the 2018 wildfires in California were up to $350 billion, or 1.7 percent of U.S. GDP. Every year, climatic disasters cause human suffering as well as large economic and ecological damage. Over the past decade, direct damages of such disasters are estimated to add up to around US$ 1.3 trillion (or around 0.2% of world GDP on average, per year).

Direct damage from climate disasters added up to $1.3 trillion over the past decade.

As scientists warn that global warming will increase the frequency and severity of such extreme weather events, the IMF’s latest Global Financial Stability Report examines the impact of climate change physical risk (loss of life and property as well as disruptions to economic activity) on financial stability, and finds that equity investors might not be pricing these risks adequately. The COVID-19 pandemic has shown how fast and extensive disruption of economic activity can be (even for well-known types of risks), underscoring the importance of preparedness and adequate risk assessment.

Some lessons from the past

Because of their central role in financial systems, equity markets provide a good setting for analyzing the financial stability implications of climate change physical risk, by gauging the impact on aggregate market indexes as well as on the financial sector specifically.

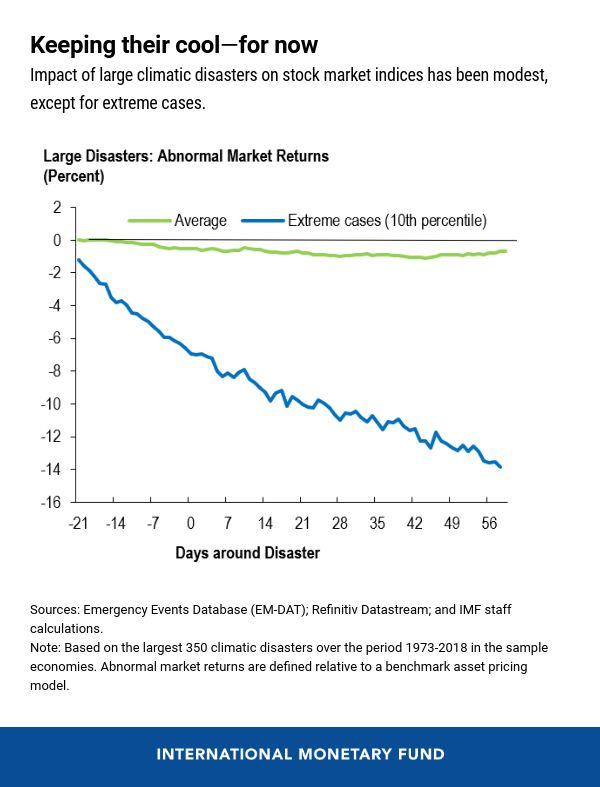

Looking back at around 350 large climatic disasters over the past 50 years (in a sample of 68 economies, representing 95 percent of global GDP), our team finds that the average impact has been modest: a drop of 2 percent for banking stocks and 1 percent for the whole market. In ten percent of cases, the impact on the aggregate market has been greater than 14 percent, indicating that some climatic disasters can have a meaningful effect on financial stability. For example, Hurricane Katrina, in 2005, with the largest damage in absolute terms in our sample (1 percent of U.S. GDP), had no discernible impact on the U.S. stock market index. The 2011 Thai floods, by contrast, with the largest damage relative to the economy’s size, caused a 30 percent drop in the stock market over 40 days.

Individual country characteristics matter. Countries with more fiscal space will be able to deploy a swift response to the disaster in the form of financial relief and reconstruction efforts. Also, well-developed risk-sharing mechanisms such as insurance reduce or redistribute the disasters’ losses and limit the impact on domestic equity prices.

Future risk and current valuations

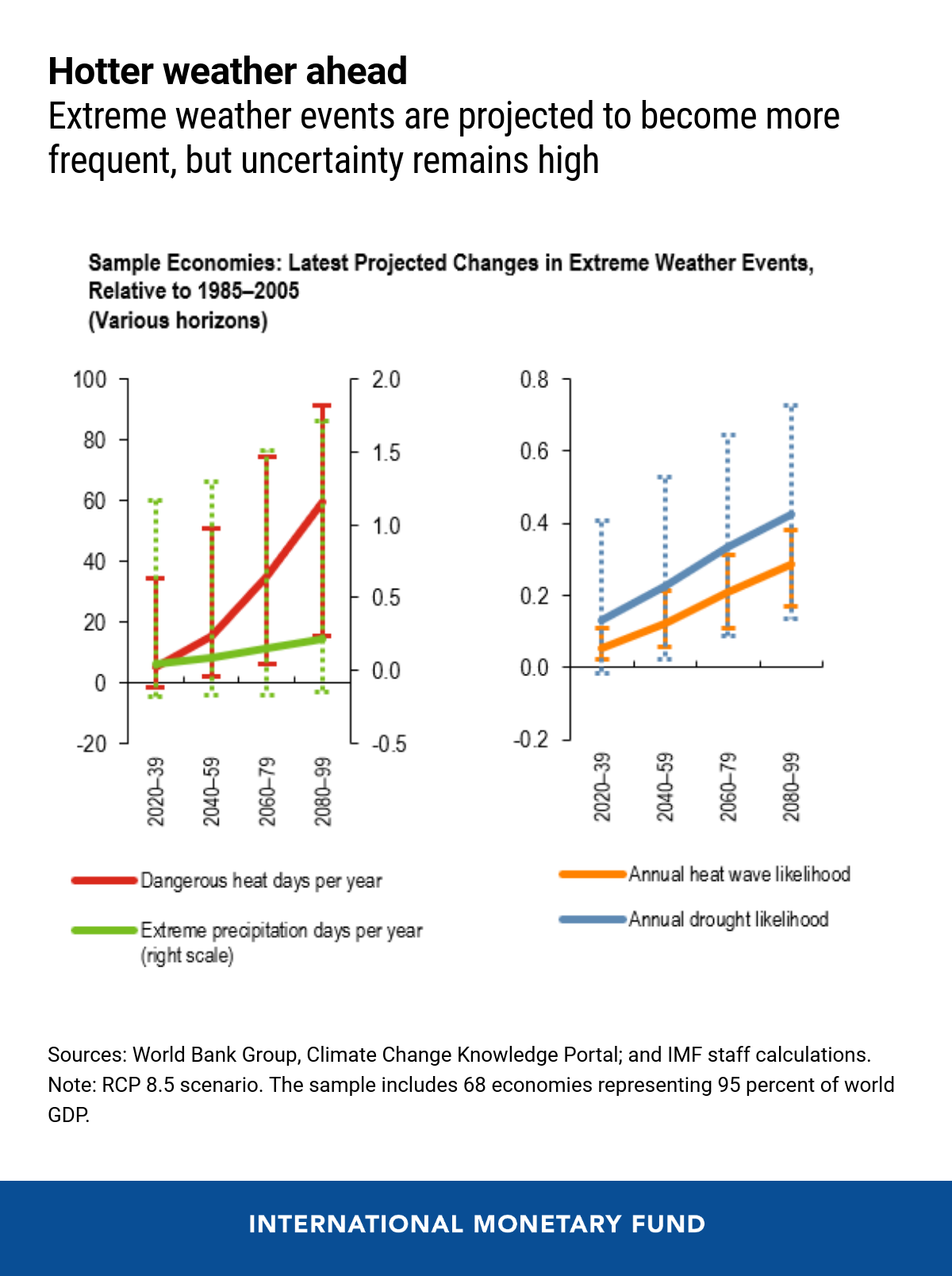

Climate change is expected to increase the probability and severity of many climatic hazards such as floods, heatwaves and droughts, subjecting economies and financial markets to greater shocks. Pricing this increase in physical risk is a daunting challenge for equity investors, who need to estimate the likelihood of various climate scenarios and their implications for physical risk at the firm level based on climate science, and expected mitigation and adaptation actions. In addition, the time horizon for these changes may be longer than even what long-term institutional investors are used to contemplating.

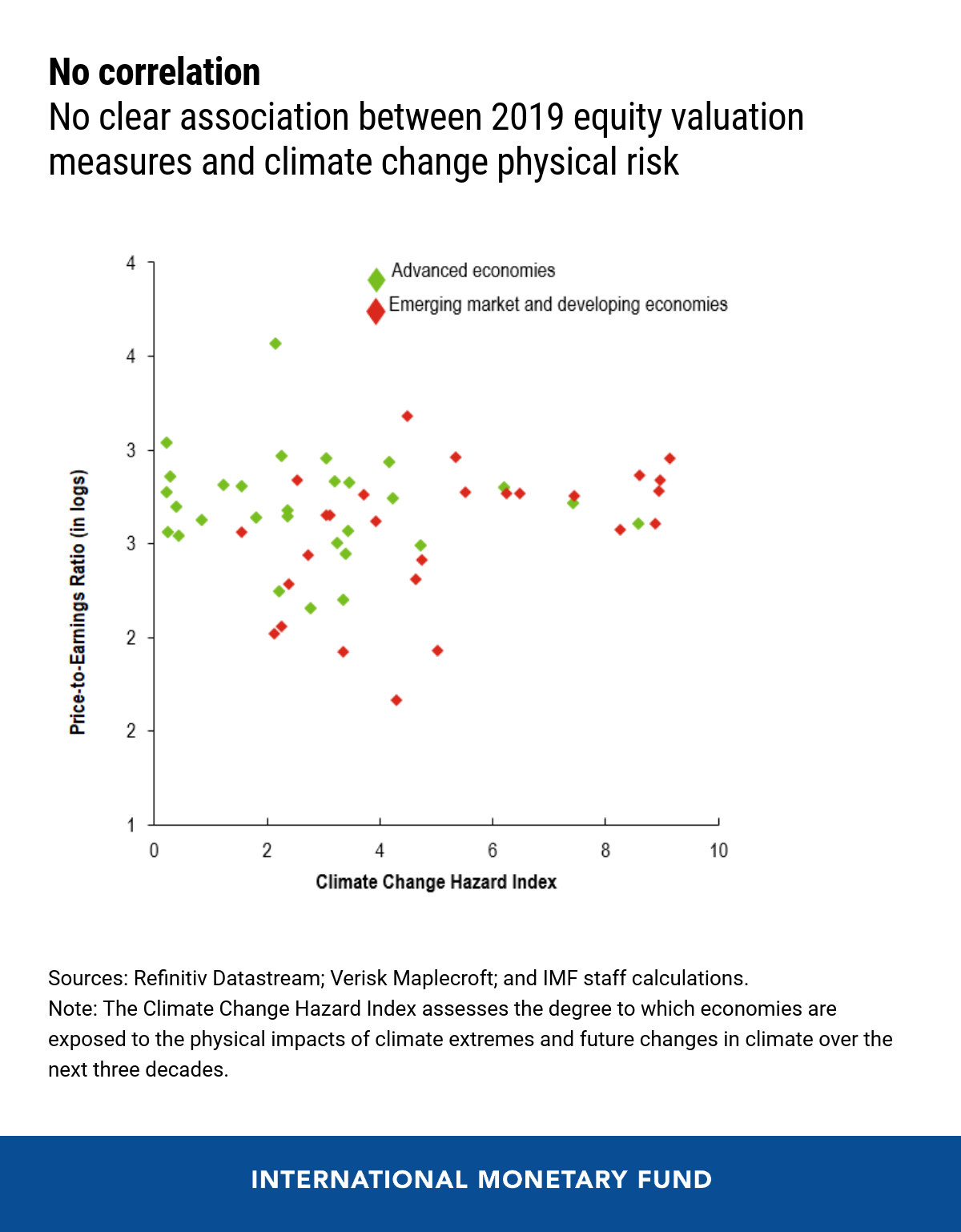

Looking retrospectively to 2019 equity valuations across countries, our study finds that they did not reflect any of the commonly discussed global warming scenarios and associated projected changes in hazard occurrence or incidence of physical risk. This apparent lack of attention could be a significant source of market risk looking forward.

What policymakers can do

The current COVID-19 pandemic is a reminder that crisis preparedness and resilience are essential to manage risks from highly uncertain events that can have extreme economic and human costs.

As mentioned above, expanding the availability of insurance and strengthening the sovereign’s overall financial strength can lessen the impact of climatic disasters and hence reduce financial stability risks.

Developing global mandatory climate change physical risk disclosure standards could be an important step to preserve financial stability too. Granular, firm-specific information on current and future exposures and vulnerabilities to climate shocks would help lenders, insurers, and investors to better grasp this risk.

Climate-change stress testing can provide financial firms and their supervisors with a better understanding of the size of their exposures and the associated physical risk. Over the past decade, one in five of the IMF’s own Financial Sector Assessment Programs considered physical risks related to climatic disasters. A recent example is the assessment published last year for the Bahamas.

Without a doubt, the most effective remedy will be strong global policy action to reduce greenhouse gas emissions, addressing the cause of global warming in a sustainable way, and conferring benefits that extend well beyond the realm of financial stability.