عربي, 中文, Español, Français, 日本語, Português, Русский

The world is in the grip of the COVID-19 pandemic and the ensuing Great Lockdown has pushed many countries into deep recessions—worse than during the 2008–09 global financial crisis. In response, governments and central banks all over the world have introduced strong discretionary (one-off and specific) fiscal and monetary measures to counteract the economic fallout caused by the spread of the coronavirus. Existing automatic stabilizers (such as income-based taxes and unemployment and household benefits), which differ across countries, have generally operated freely, providing some further cushion.

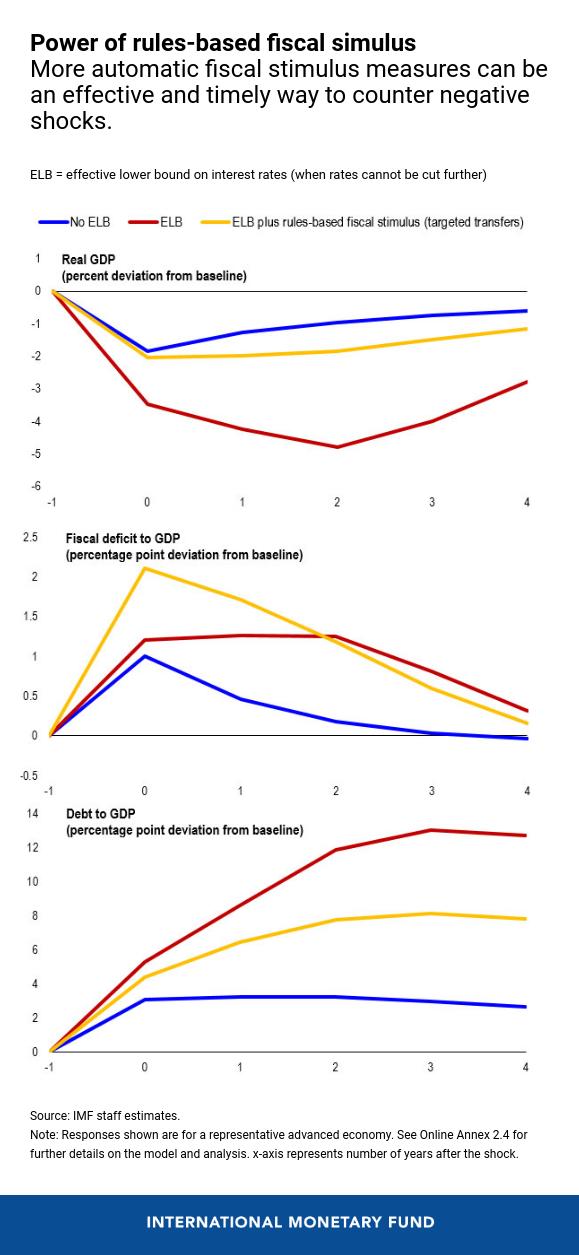

But with interest rates at record lows and public debts at historical highs in many countries, how can advanced economies best prepare for and respond to future downturns? Analysis in our recent World Economic Outlook completed before the pandemic looks at how advanced economies could build their resilience to negative shocks in such an environment. It finds that rules-based fiscal stimulus—where the stimulus is automatically triggered by deteriorating macroeconomic indicators—can be highly effective in countering a downturn under such conditions.

Rules-based fiscal stimulus can be highly effective in countering a downturn.

A larger role for fiscal policy

With interest rates at or near zero in advanced economies, the scope for further conventional rate cuts is limited. But central banks may still use unconventional monetary policy tools more intensively—like large-scale asset purchases—to deliver additional support, as they have recently in response to the pandemic. However, relying on monetary policy alone to respond to shocks might not be enough and also raises questions about side effects on future financial stability and threats to central bank independence.

While keeping an eye on debt sustainability concerns over the long term, fiscal policy needs to play a larger role. Putting in place more automatic fiscal responses in advanced economies could help build their resilience to future adverse shocks. If rules for fiscal stimulus are well communicated and established before shocks occur, they can help shape expectations and reduce uncertainty, thereby dampening the drop in activity once a negative shock materializes.

A case for more automatic fiscal stimulus

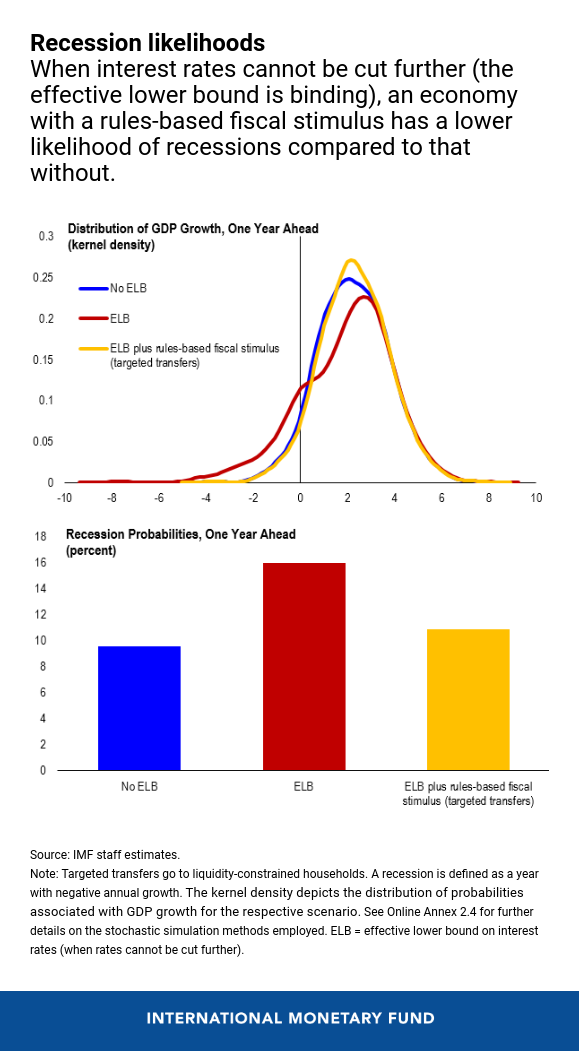

Our study shows that rules-based fiscal stimulus measures—such as temporary targeted cash transfers to liquidity-constrained, low-income households that kick in when the unemployment rate rises above a certain threshold—could be highly effective in countering a downturn caused by a typical demand shortfall. Although these stimulus measures would be automatic, they are very different from traditional automatic stabilizers, which instead respond to an individual’s circumstances (for example, being laid-off in the case of unemployment insurance or lower incomes in the case of progressive income taxes). Rules-based fiscal stimulus is particularly effective when interest rates are at their effective lower bound (when rates cannot be cut further) and discretionary fiscal policy lags are long. Moreover, fiscal stimulus after demand shocks tend to be especially powerful when the economy has unemployed resources and monetary policy is accommodative.

When demand falls suddenly, the fall in output and rise in debt ratios are smaller when a rules-based fiscal stimulus is in place to support the economy. In fact, our findings suggest that when rules-based fiscal stimulus measures are adopted, economic downturns can be countered nearly as effectively as when monetary policy is able to operate at full strength.

The current economic shock from the pandemic is unusual as it has affected both supply and demand. Even though the political will for action has rapidly coalesced in response to the current shock, its unrivaled speed and depth have complicated the design and timely delivery of discretionary fiscal support. When workers and firms are unable to operate while the epidemic is active, the effectiveness of fiscal stimulus to boost output (the multiplier) is low. Nonetheless, even in these circumstances, a rules-based fiscal stimulus implemented ahead of time could have been helpful, especially in the form of targeted transfers. These measures could provide further income insurance and strengthen the social safety net for the vulnerable.

Our findings suggest that policymakers should consider enhancing fiscal policy’s automatic response to negative shocks, helping to improve the economy’s resilience. In parallel, even if interest rates cannot be cut further, monetary policy can support fiscal stimulus in a recession by maintaining an accommodative stance, including by easing financial market conditions.

Designing and adopting new fiscal tools—like rules-based fiscal stimulus measures—and improving existing automatic stabilizers will take time and require political agreement. But with automatic policies for fiscal stimulus in place, the risks that political hurdles delay responses when economic conditions deteriorate are lower. Moreover, when monetary policy is constrained, having in place rules-based fiscal stimulus measures can markedly reduce the likelihood of demand-driven recessions.

This does not mean that discretionary fiscal policy becomes redundant. In fact, discretionary fiscal measures, appropriately tailored to the specific circumstances and the nature of the negative shock—like the pandemic shock—are essential to provide powerful countercyclical support. But they must be adopted and deployed in a timely manner.

A more agile response to future recessions

Given historical delays in the implementation of discretionary fiscal stimulus and the helpful effects of setting expectations by adopting rules for action in advance, there is a strong case for a more automatic fiscal response to economic downturns. Our analysis shows that adopting rules-based fiscal stimulus measures can be highly effective and more timely, particularly when central bank interest rates are close to or at their effective lower bound and monetary policy is constrained.

Based on Chapter 2 of the World Economic Outlook, “Countering Future Recessions in Advanced Economies: Cyclical Policies in an Era of Low Rates and High Debt,” by Michal Andrle, Philip Barrett, John Bluedorn (co-lead), Francesca Caselli, and Wenjie Chen (co-lead).