Global interest rates in recent months have gone on a rollercoaster, especially those on longer-term government bonds. Yields on 10-year US Treasuries are climbing again after pulling back from a 16-year high of 5 percent in October. Interest rate moves in other advanced economies had been equally prodigious.

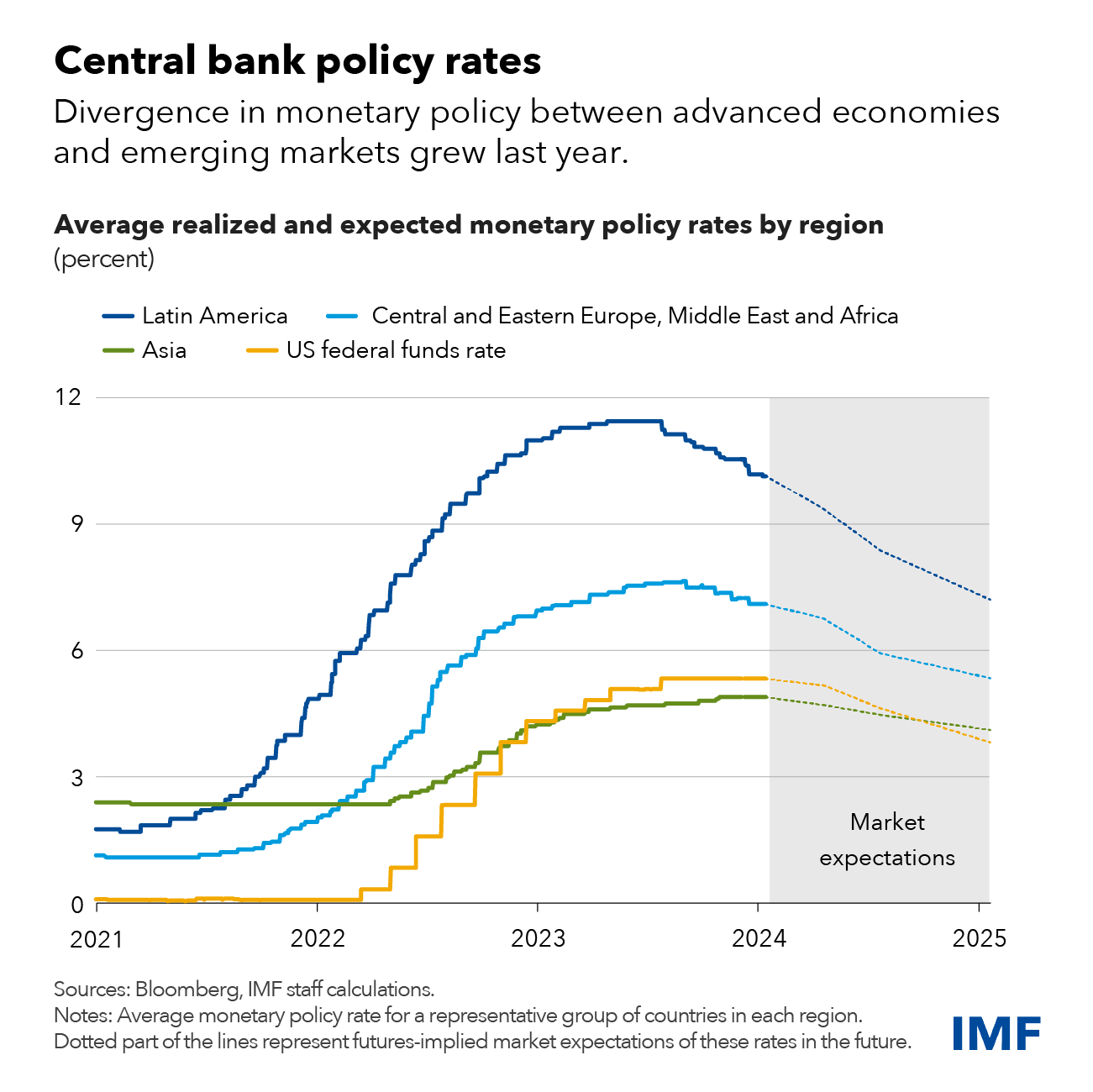

Emerging market economies, however, saw much milder rate moves. We take a longer-term perspective on this in our latest Global Financial Stability Report, demonstrating that the average sensitivity to US interest rates of 10-year sovereign yield of Latin American and Asian emerging markets declined by two-thirds and two-fifths, respectively, during the current monetary policy tightening cycle compared with the taper tantrum in 2013.

While the lower sensitivity is in part due to the divergence in monetary policy between advanced economies’ and emerging markets’ central banks over the past two years, it nonetheless challenges findings in the economic literature that show large spillovers from advanced economies’ interest rates to emerging markets. In particular, major emerging markets have been more insulated from global interest rate volatility than would be expected based on historical experience, especially in Asia.

There are other signs of resilience in major emerging markets during this period of volatility. Exchange rates, stock prices, and sovereign spreads fluctuated in a modest range. More remarkably, foreign investors did not leave their bond markets, in contrast to past episodes when large outflows ensued after surges in global interest rate volatility, including as recently as 2022.

This resilience was not just good luck. Many emerging markets have spent years improving policy frameworks to mitigate external pressures. They have built additional currency reserves over the last two decades. Many countries have refined exchange-rate arrangements and moved towards exchange-rate flexibility. Significant foreign exchange swings have contributed to macroeconomic stability in many cases. The structure of public debt has also become more resilient, and both domestic savers and domestic investors have become more confident investing in local-currency assets, reducing reliance on foreign capital.

Perhaps most importantly, and closely aligned with IMF advice, major emerging markets have enhanced central bank independence, improved policy frameworks, and gained progressively more credibility. We would also argue that central banks in these countries have gained additional credibility since the onset of the pandemic by tightening monetary policy in a timely manner and bringing inflation toward target as a result.

During the post-pandemic era, many central banks hiked interest rates earlier than counterparts in advanced economies—on average, emerging markets added 780 basis points to monetary policy rates compared to an increase of 400 basis points for advanced economies. The wider interest differentials for those emerging markets that hiked rates created buffers for emerging markets that kept external pressures at bay. In addition, the rise in prices of commodities during the pandemic also helped the external positions of commodity-producing emerging markets.

Global financial conditions too have remained quite benign during the current global monetary policy tightening cycle, especially last year. This contrasts with previous hiking episodes in advanced economies, which were accompanied by a much more pronounced tightening of global financial conditions.

Looking ahead

Despite reaping rewards from years of building buffers and pursuing proactive policies, policymakers in major emerging markets need to stay vigilant with an eye on the challenges inherent in the “last mile” of disinflation and rising economic and financial fragmentation. Three challenges stand out:

- Interest rate differentials are narrowing as some emerging markets

are anticipated by investors to cut rates faster than advanced economies,

which could entice capital to leave emerging market assets in favor of

assets in advanced economies;

- Quantitative tightening by major advanced economies continues to

withdraw liquidity from financial markets, which could additionally weigh

on emerging market capital flows;

- Global interest rates remain volatile, as investors—reacting to central banks emphasizing data-dependency—have grown more attentive to surprises in economic data. Perilous for emerging markets are market projections that central banks in advanced economies will materially cut rates this year. Should this prove wrong, investors may once again reprice in higher-for-longer rates, weighing on risky asset prices, including emerging market stocks and bonds.

A slowdown in emerging markets, as projected by the latest World Economic Outlook update, operates not only through traditional trade channels, but also through financial channels. This is particularly relevant now, as more borrowers globally are defaulting on loans, in turn weakening banks’ balance sheets. Emerging market bank loan losses are sensitive to weak economic growth, as we showed in a chapter of the October Global Financial Stability Report.

Frontier emerging markets—developing economies with small-but-investable financial markets—and lower-income countries face greater challenges, the primary one being the lack of external financing. Borrowing costs are still high enough to effectively prohibit these economies from obtaining new financing or rolling over existing debt with foreign investors.

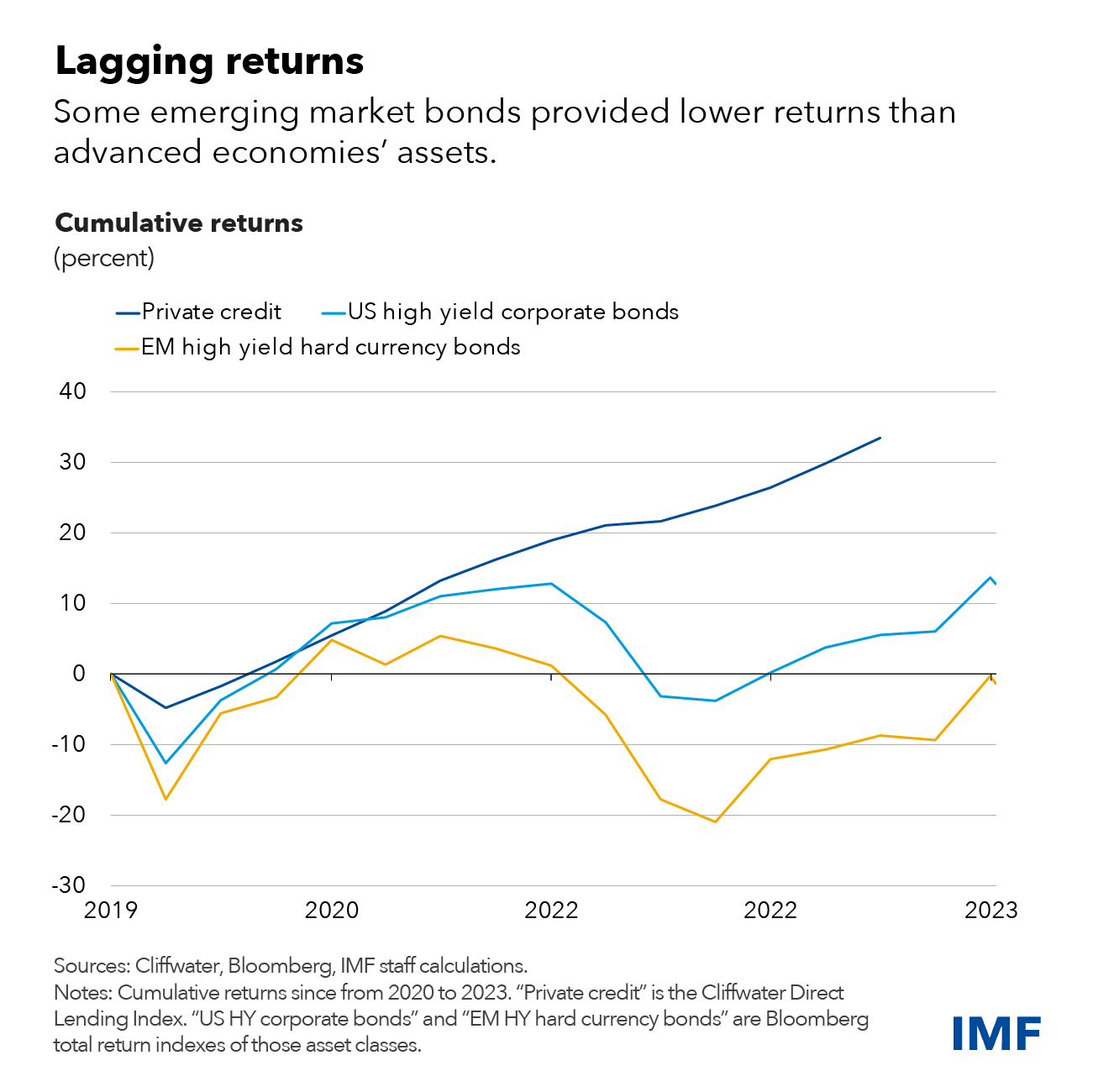

High financing costs reflect the risks associated with emerging market assets. Indeed, the dollar returns on these assets have lagged similar advanced economies’ assets during this high-rate environment. For instance, emerging market bonds for high-yield, or lower-rated, issuers have returned about zero percent on net over the past four years, while US high-yield bonds have provided 10 percent. So-called private credit loans provided by nonbanks to lower-rated US companies have returned even more. The sizable differences in returns may not bode well for emerging markets’ external financing prospects as foreign investors with mandates that allow for investments across asset classes can find more-profitable alternative assets in advanced economies.

While these challenges for emerging market and frontier economies require close attention by policymakers, there are also many opportunities. Emerging markets continue to see significantly higher expected growth rates than advanced economies; capital flows to stock and bond markets remain strong; and policy frameworks are improving in many countries. Hence the resilience of major emerging markets that has been important for global investors since the pandemic may continue.

Vigilant policies

Emerging markets should continue to build on the policy credibility they have gained and be vigilant. Facing elevated global interest rate volatility, their central banks should continue to commit to inflation targeting, while remaining data dependent in their inflation objectives.

Keeping monetary policy focused on price stability also means using the full spate of macroeconomic tools to fend off external pressures, with the IMF’s Integrated Policy Framework providing guidance on the use of currency intervention and macroprudential measures.

Frontier economies and low-income countries could strengthen engagement with creditors—including through multilateral cooperation—and rebuild financial buffers to regain access to global capital. In the bigger picture, countries with credible medium-term fiscal plans and monetary policy frameworks will be better positioned to navigate periods of global interest rate volatility.

—Subscribe to the blog and other IMF publications via this link.