Central banks will likely keep interest rates higher for longer in economies with persistently elevated core inflation (excluding food and energy prices). The high-interest-rate environment, which recently triggered banking sector stress in some advanced economies, could be a harbinger of more systemic risks. It could tighten financial conditions, trigger credit stress, and reduce funding for financial institutions, including in the Middle East, North Africa, and Pakistan. Such stress could threaten bank profits and willingness to lend, materially impacting financial stability and economic growth.

Financial stability risks such as a high reliance on external funding can leave banks in some countries vulnerable to sudden changes in investor sentiment. In addition, where lenders hold a significant share of domestic sovereign debt, a lengthy period of higher interest rates could lead to losses, particularly if the market value of that debt declines and the assets are at a lower price.

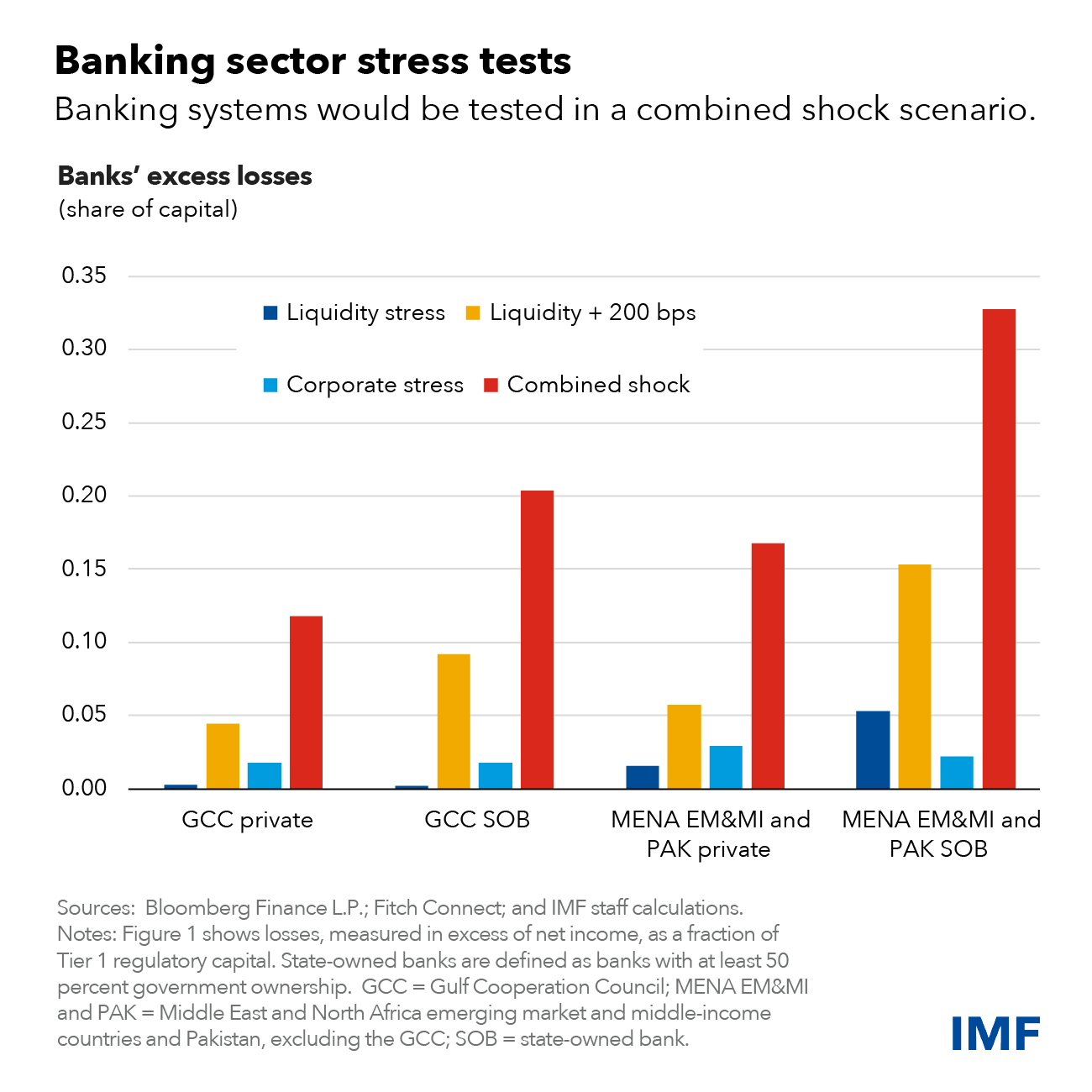

In our recently published Regional Economic Outlook for the Middle East and Central Asia, we detail the first region-wide stress test. It uses four scenarios to assess the risks of higher-for-longer interest rates in the region’s emerging market and middle-income countries and the six Gulf Cooperation Council economies.

The results suggest banks across most countries in the region would be able to withstand individual stress scenarios, but could be tested by a combination of higher interest rates, corporate sector stress, and liquidity pressures. Importantly, state-owned banks are more vulnerable than privately-owned banks. This is due to the lower profitability and higher securities holdings of state-owned banks, which raise interest-rate risk.

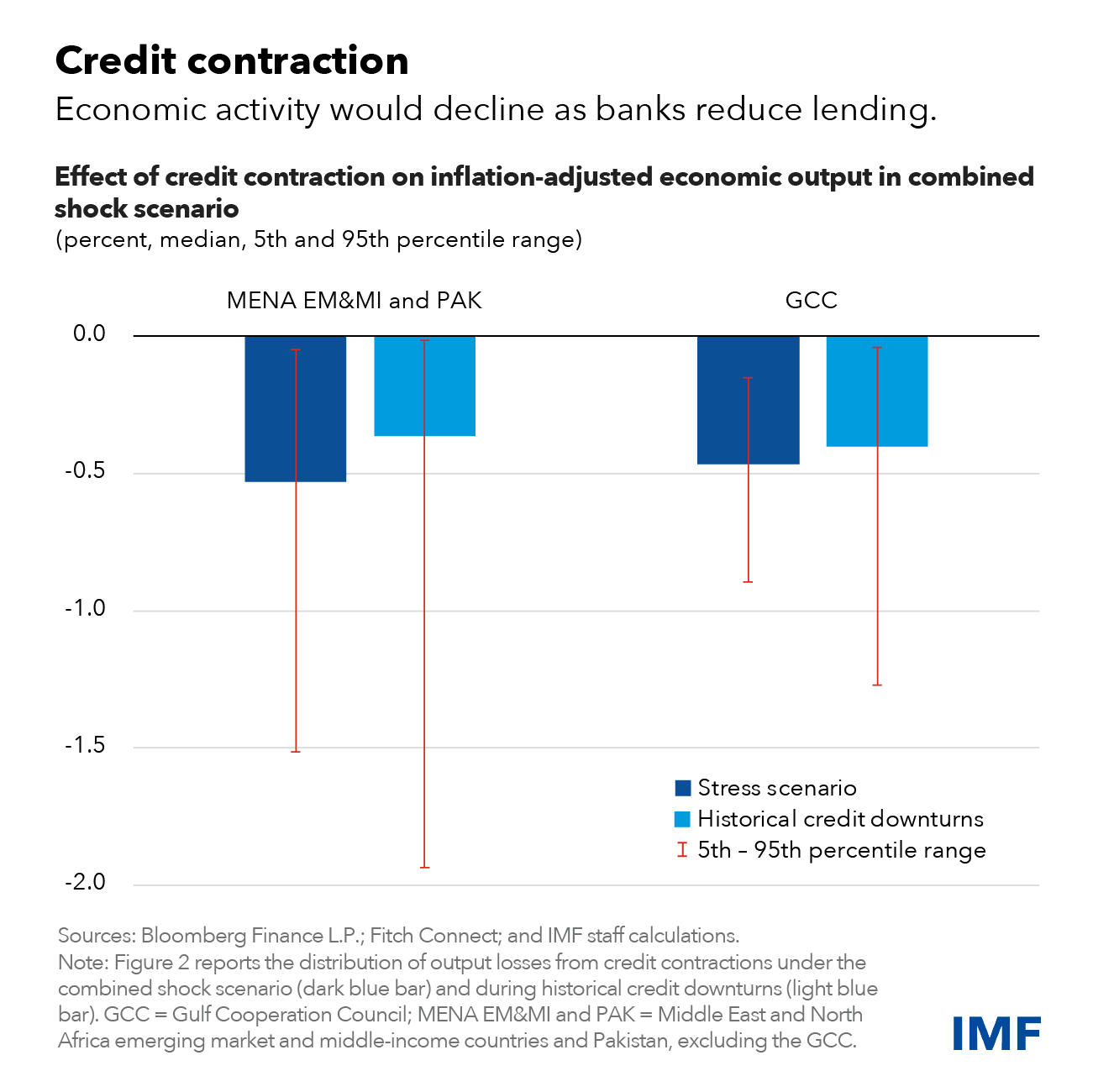

Few banks would breach minimum regulatory capital ratios in the combined shock scenario. Still, less capital would likely result in reduced lending to the private sector and a decline in economic activity, which is comparable to previous episodes of credit contraction. For example, the inflation-adjusted economic output loss in the combined shock scenario could be as high as 1.5 percent over two years. The estimated loss for the Gulf economies would be 0.9 percent.

Monetary policy is an important factor in these countries. Central banks are facing difficult policy tradeoffs at a time when measures of core inflation, which exclude volatile food and energy prices, remain above target in many countries.

In a low-inflation environment, central banks can respond to financial stress by cutting interest rates. However, when inflation is high during periods of stress, policymakers must balance safeguarding financial stability and keeping inflation under control.

Policymakers need appropriate tools to tackle banking sector turmoil that could impact financial stability. Strengthening prudential standards—for example, by encouraging banks to accumulate capital during expansions so that they can sustain lending during downturns—can better manage risk. Vulnerabilities from bank holdings of government debt should be accounted for in stress testing to improve resilience to shocks. Over the next few years, efforts by policymakers to foster a deep and diversified investor base to help reduce the interconnectedness between the health of the banking system and the sovereign should continue, especially where state-owned entities dominate the marketplace.

Establishing emergency liquidity tools, such as central bank emergency lending, to stem systemic financial stress is also critical. However, governments should communicate clearly to ensure that liquidity support is not perceived to be working at cross-purposes with monetary policy. Finally, developing effective plans to wind down firms in distress would reduce risks to financial stability and economic growth.

—This blog is based on Chapter 3 of the October 2023 Middle East and Central Asia Regional Economic Outlook, Higher for Longer: What are the Macrofinancial Risks? The report authors are Adrian Alter, Bashar Hlayhel, Thomas Kroen, Troy Matheson (co-lead), and Thomas Piontek (co-lead).