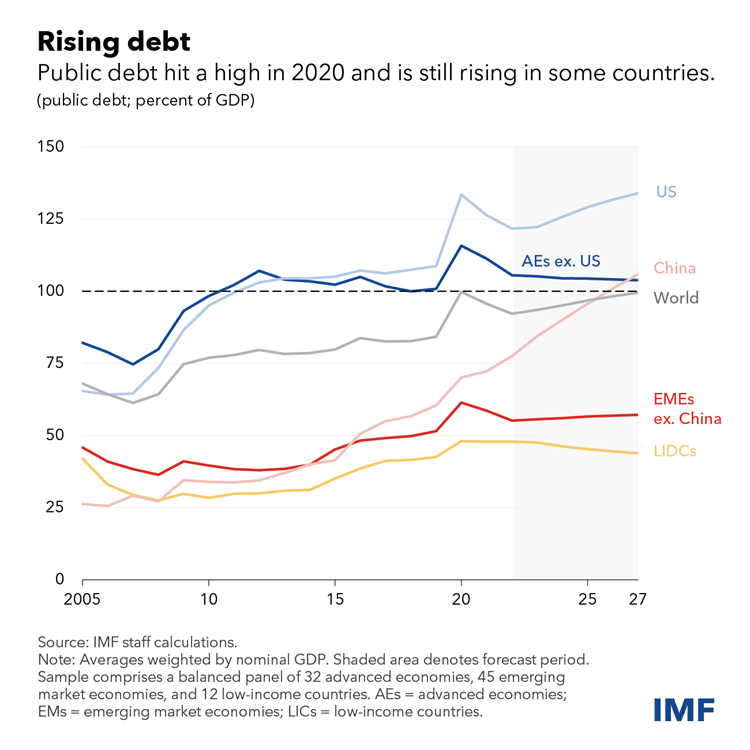

Public debt soared to a record during the pandemic, topping global gross domestic product. Now, with government debt still elevated, the rise in interest rates and the strong US dollar are adding to interest costs, in turn weighing on growth and fueling financial stability risks.

With several economies already in debt distress, we explore in an analytical chapter of our latest World Economic Outlook what policies work best to durably reduce public debt ratios (or debt to GDP).

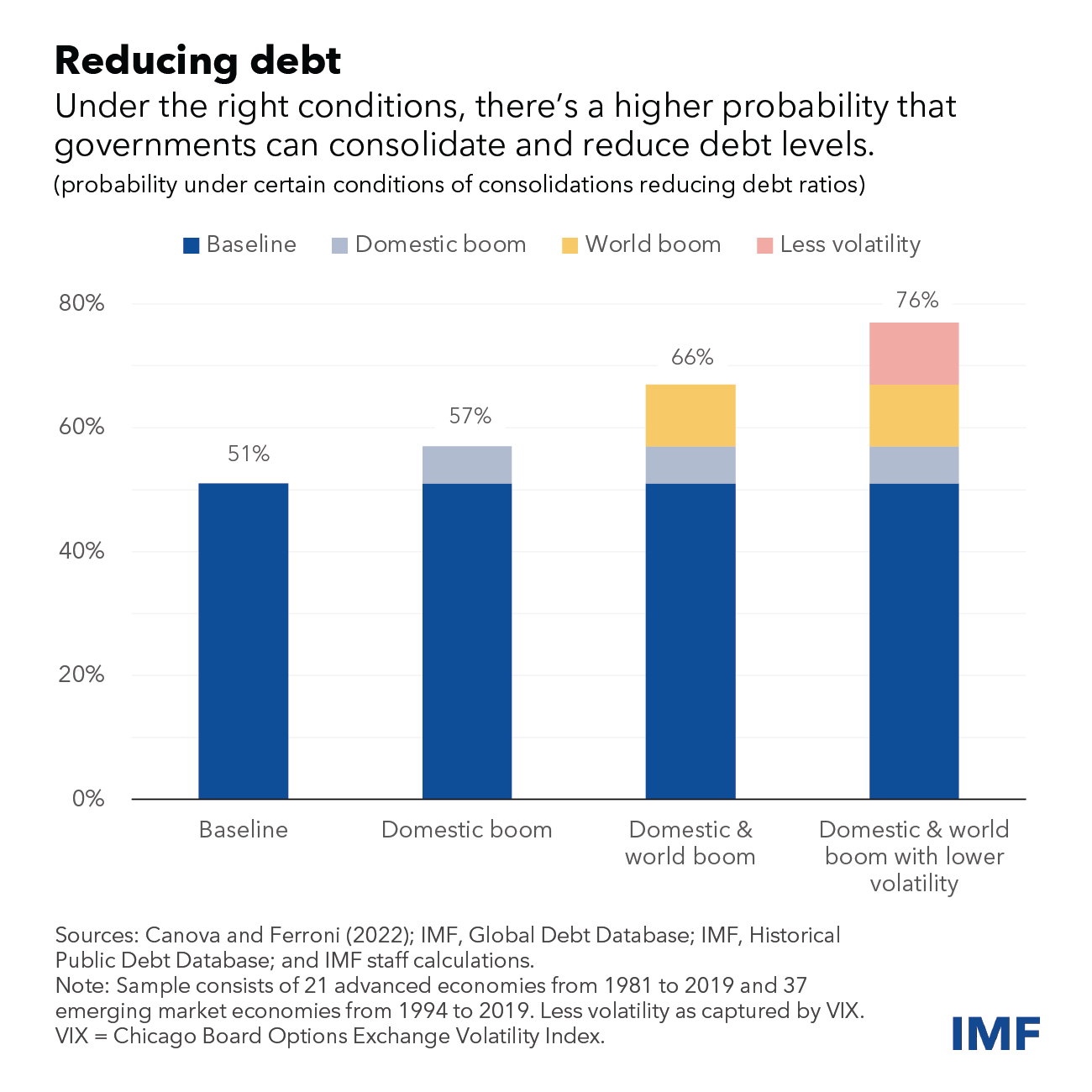

Using two decades of data, we find that an adequately tailored fiscal contraction of about 0.4 percentage point of GDP—the average size in our sample—lowers the debt ratio by 0.7 percentage point in the first year and up to 2.1 percentage points after five years.

But the timing of the adjustment can impact what effect it has. The

probability of reducing debt ratios through consolidation improves from the

baseline (average) of about half to three-quarters when undertaken during a

domestic and global boom or periods during which financial conditions are

loose and uncertainty is low.

Design also matters. In advanced economies, spending cuts are more likely to lower debt ratios than increasing revenues. Odds of success also improve when fiscal consolidation is reinforced by growth enhancing structural reforms and strong institutional frameworks.

This explains why fiscal consolidation hasn't typically reduced debt ratios in the past—the right conditions and accompanying policies weren’t present.

There are important factors for why fiscal consolidation alone didn’t reduce the debt ratio level in about half of the cases: first fiscal consolidation tends to slow GDP growth( see Chapter 3 of the 2010 WEO). Second, exchange rate fluctuations and transfers to state-owned enterprises or contingent liabilities can offset debt reduction efforts. These “below-the-line” operations can increase debt, despite improvements in the primary balance (which would ordinarily drive down debt). Examples include unexpected transfers that the government provided to state-owned enterprises in Mexico (2016), and clearance of payments past due by the government in Greece (2016), which were all recorded as below the line items in the fiscal account.

Debt restructuring

While well-designed fiscal consolidation and growth-friendly structural reforms can help reduce debt ratios, they may not be sufficient for countries in debt distress or facing increased rollover risks. In such cases, debt restructuring—a renegotiation of the terms of a loan—may be necessary.

Restructuring is typically used as a last resort. It’s a complex process that requires the agreement of domestic and foreign creditors and involves burden sharing between different parties (for example, between residents and banks in most domestic restructurings). It can incur significant economic costs and there are reputational risks and coordination challenges.

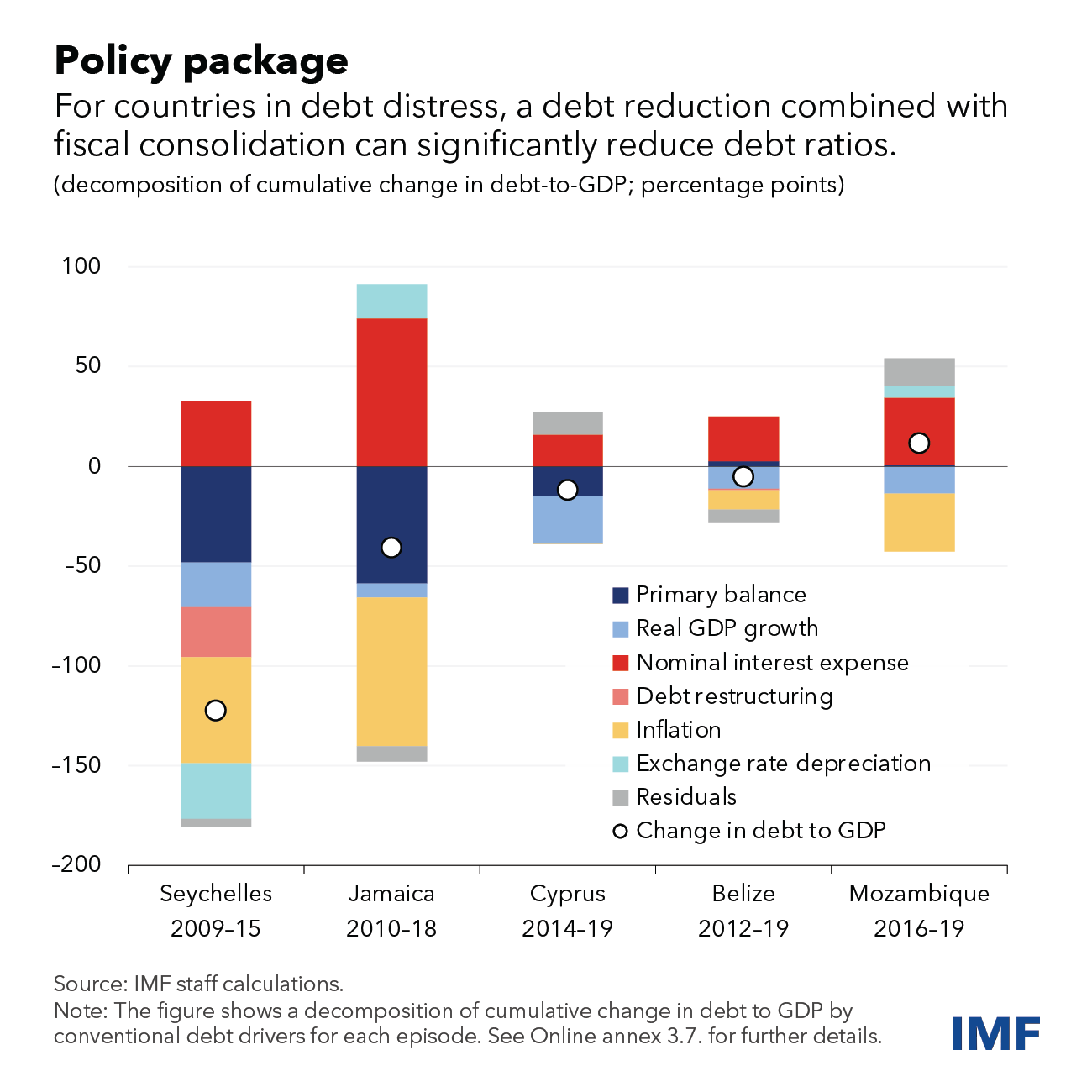

But when combined with fiscal consolidation, it can significantly reduce debt ratios—on average, up to 8 percentage points or more after 5 years in emerging markets and low-income countries.

Seychelles, for example, had a debt ratio of over 180 percent in 2008, when the global financial crisis hit. After debt restructurings with both official Paris Club and private external creditors that involved a large reduction in face value of debt, this ratio sharply declined to 84 percent in 2010. Prudent fiscal policy combined with high GDP growth helped sustain the reduction in debt ratios.

We also found that it matters how deep the restructuring is. Public debt in

Belize remained elevated despite two sequential restructurings, suggesting

that even when done early, debt will stay high if the treatment is not deep

enough. By contrast, debt ratios in Jamaica were significantly reduced with

early and deep restructurings that were executed through an extension of

maturity and a reduction in coupon payments rather than a reduction in the

face value of debt. Notably, the fiscal space created by the debt service

relief from restructuring was saved, as reflected in its strong fiscal

consolidation.

For countries that can afford a moderate and gradual reduction in debt ratios, it’s best to undertake fiscal consolidation when conditions are favorable, along with policies that include structural reforms aimed at promoting growth. Having strong institutional frameworks can prevent "below the line" operations that undermine debt reduction efforts and ensure that countries indeed build buffers and reduce debt during good times.

Countries facing increased funding pressures or already in debt distress may have no viable alternative than a substantial or rapid debt reduction. Fiscal consolidation will likely be needed to regain market confidence and recover macroeconomic stability in these countries. In addition, policymakers should also consider timely debt restructuring. If pursued, the restructuring will need to be deep to reduce debt ratios.

For restructurings to succeed, global policymakers must also promote mechanisms to enhance coordination and confidence among creditors and debtors. The Group of Twenty Common Framework should be improved to bring greater predictability, earlier engagement, a payment standstill, and further clarification on comparability of treatment.

This blog is based on Chapter 3 of the April 2023 World Economic Outlook, “How to Tackle Soaring Public Debt.” The authors of the chapter are Sakai Ando, Tamon Asonuma, Alexandre Balduino Sollaci, Giovanni Ganelli, Prachi Mishra (co-lead), Nikhil Patel, Adrian Peralta-Alva (co-lead) and Andrea Presbitero, with support from Carlos Angulo, Zhuo Chen, Sergio Garcia and Youyou Huang.