In some Asia-Pacific countries, the unpleasant memory of the pandemic is receding; elsewhere, second or third waves of infections are raging. A recovery is underway, but the regional averages obscure wide differences within and across countries.

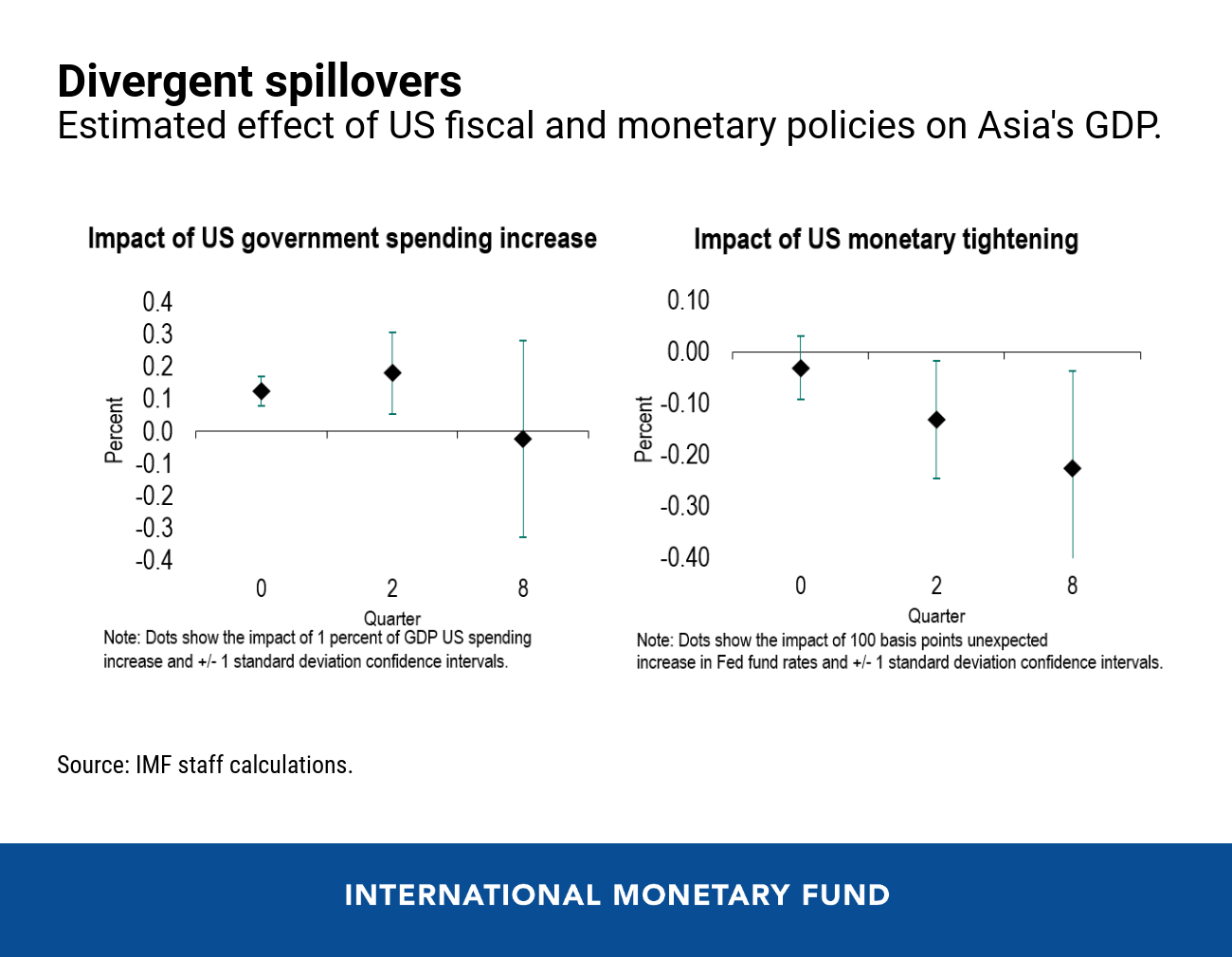

Asia is likely to benefit from the US fiscal expansion through trade channels, but could experience financial turbulence or capital outflows if US yields rise faster than markets expect.

Everywhere, the pandemic has inflicted historic income losses borne mostly by the less advantaged: low-wage and informal workers, as well as youth and women. A region known for its trademark growth-with-equity model now runs the risk of entrenching excessive inequality. If policymakers do not act, they risk stunted opportunities, fragile growth, and even social unrest.

Divergence rules

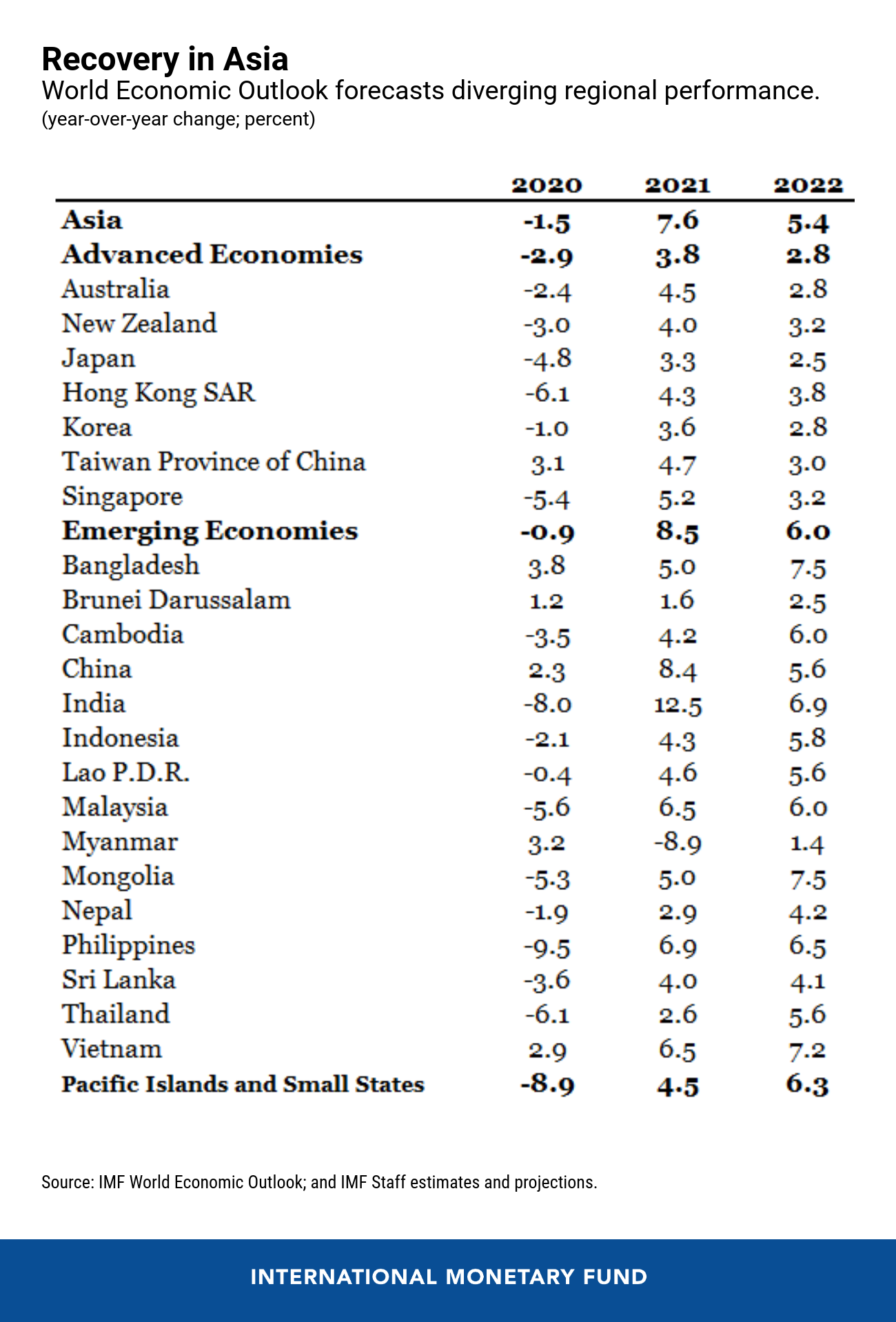

Overall, exports and manufacturing have benefited from surging global demand for pandemic-related supplies. But economies more dependent on services are mostly languishing. We project regional growth to rebound to 7.6 percent this year and 5.4 percent next year.

Advanced economies (Australia, Japan, Korea) are benefiting from positive growth surprises late last year, strong policy responses, and spillovers from the large US fiscal package.

Some emerging markets, notably Indonesia, Malaysia, and the Philippines, are contending with increased coronavirus cases and renewed lockdowns, and therefore face a weaker recovery.

Growth in China and India has been revised up. For China, the markup to 8.4 percent this year reflects stronger net exports and the US fiscal stimulus, while the revision to 12.5 percent for India is driven by continued normalization of its economy and a more growth-friendly fiscal policy, even as the number of active cases has ticked up sharply in recent weeks.

Pacific Islands and other small states have been hit hard by the collapse in tourism and the sharp contraction in demand for commodities.

Disease variants looming

Wherever populations have received rapid and broad vaccine rollouts, health conditions have improved and propelled stronger recoveries. But the emergence of new variants and waves of infection, and questions about vaccine efficacy, remind us that the health crisis is far from over and that there is huge uncertainty surrounding the outlook.

The changing external environment is a central driver of risk in the region, given Asia’s outward orientation to trade and capital flows. The combination of expansionary fiscal policy in the United States with the marked increase in US 10-year government bond yields is reverberating in the region. Our analysis highlights important spillovers for Asian economies.

- Asia is likely to experience favorable spillovers through trade channels as US fiscal expansion boosts growth and imports—that’s the good news for the region.

- But if US yields rise faster than markets expect, or if there is miscommunication about future US monetary policy, adverse spillovers through financial channels and capital outflows, as during the 2013 taper tantrum, could compromise macrofinancial stability.

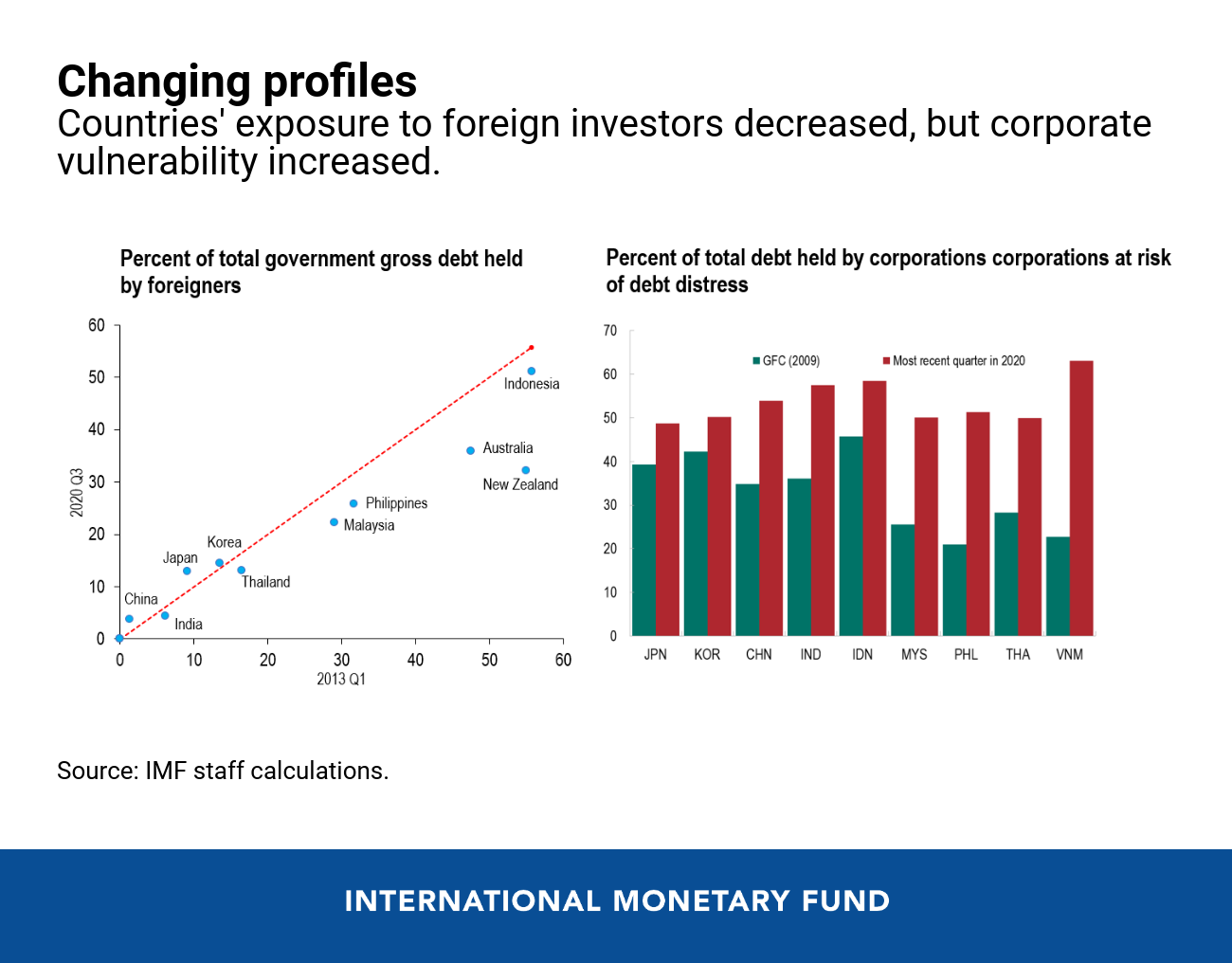

The consequences will thus vary according to country-specific trade and financial linkages. The share of foreign holdings of Asia’s government debt has diminished in recent years, reducing exposure to nonresident investors. In addition, greater official reserve holdings, more flexible exchange rates, stronger supervision over bank balance sheets, and better anchored inflationary expectations should dampen the impact of any faltering in foreign investors’ risk appetite.

However, the increase in debt across government, household, and corporate balance sheets means that higher borrowing costs—when they come—will hurt. Managing the risks and laying the foundation for a sustainable inclusive post-pandemic recovery requires deft policies today.

Agenda for the post-pandemic

Ensuring that vaccines are widely available in all countries remains the first priority. Boosting supply and administration capacity is essential, and international cooperation is needed to ensure universal distribution at affordable prices.

Fiscal support, targeted to those in need, should remain in place until the pandemic is behind us and private demand recovers. Broad lifelines should be phased out only gradually as the pandemic recedes and future support should then be geared to achieve needed reallocation of resources toward new dynamic (green and digital) sectors. Even now, policymakers need to be attentive to anchoring public debt in credible medium-term frameworks, especially where fiscal space and buffers have been eroded.

Monetary policy should continue to be data-dependent and attendant to macroeconomic and financial stability risks. The challenges going forward may be significant given the possibility of renewed bouts of capital outflows, and risks from inflated house prices in some countries. Policymakers will have to rely on monetary policy and other instruments to safeguard macrofinancial stability in this challenging environment.

But stability is only one objective. Growth productivity and the size of the pie, and giving all citizens a fair shot at this growing pie, are equally important. Policymakers must recommit to a greener and more inclusive recovery that ensures equality of opportunity in Asia’s growing and more sustainable economy.

Trade has historically been an engine of growth in this region, boosting incomes and living standards and lifting millions out of poverty. Since the mid-1990s, however, the pace of trade liberalization has stalled and too many tariffs and nontariff barriers are in place. Broad liberalization would deliver sizeable output gains in the medium term and help to offset the scars from the current crisis.

Corporate debt, already high before, has increased further with the pandemic, despite exceptional fiscal and monetary policy support. Corporate sector policies must now pivot from liquidity to solvency support: streamlining insolvency procedures; maintaining credit to allow viable firms to recover; and facilitating fresh equity capital to help firms reduce debt and grow.

The Asian recovery stands out because of prompt and effective policies during pandemic’s acute phase. The next phase is even more challenging: to lay the foundation for a more inclusive, greener, and resilient region.