Growth in the euro area rebounded earlier this year, but it remains fragile, while risks have increased. Now is a good time for euro area economies to strengthen their ability to weather any future economic difficulties.

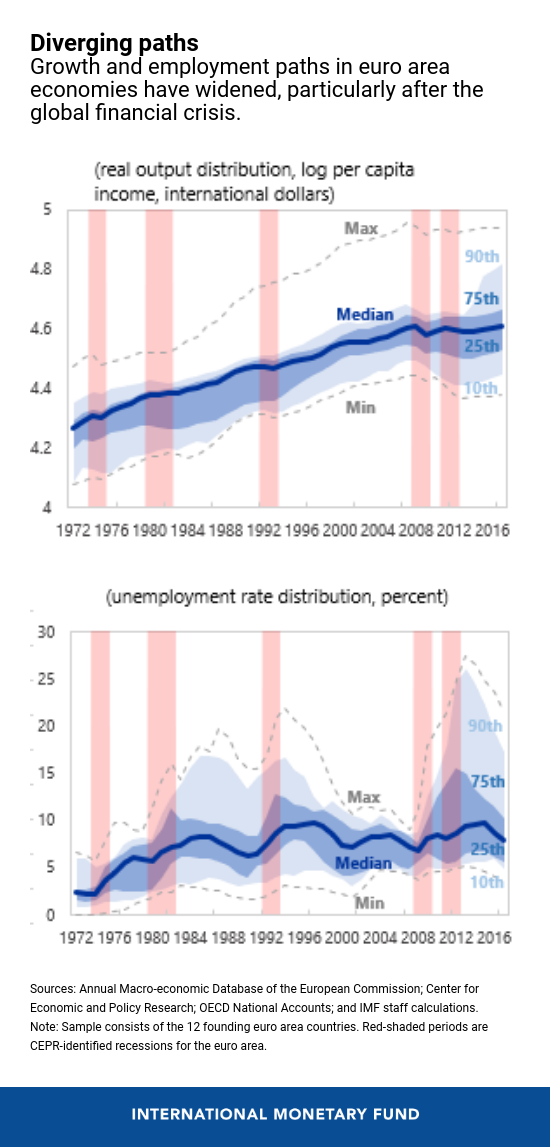

A new IMF staff paper looks at the resilience of euro area countries and finds that they have had more frequent and severe recessions than other advanced economies over the past 20 years. An even greater cause for concern is that differences between member countries’ growth and unemployment rates after euro area-wide downturns have widened. This widening was most stark following the 2008 global financial crisis.

While euro area countries have made substantial progress in improving fundamental aspects of the economic and monetary union since then, they have more to do: from completing the banking and capital markets unions to establishing a central fiscal capacity for macroeconomic stabilization. But euro area-wide architectural improvements cannot fully substitute for the economic flexibility provided by national structural reforms. These also have a vital role to play.

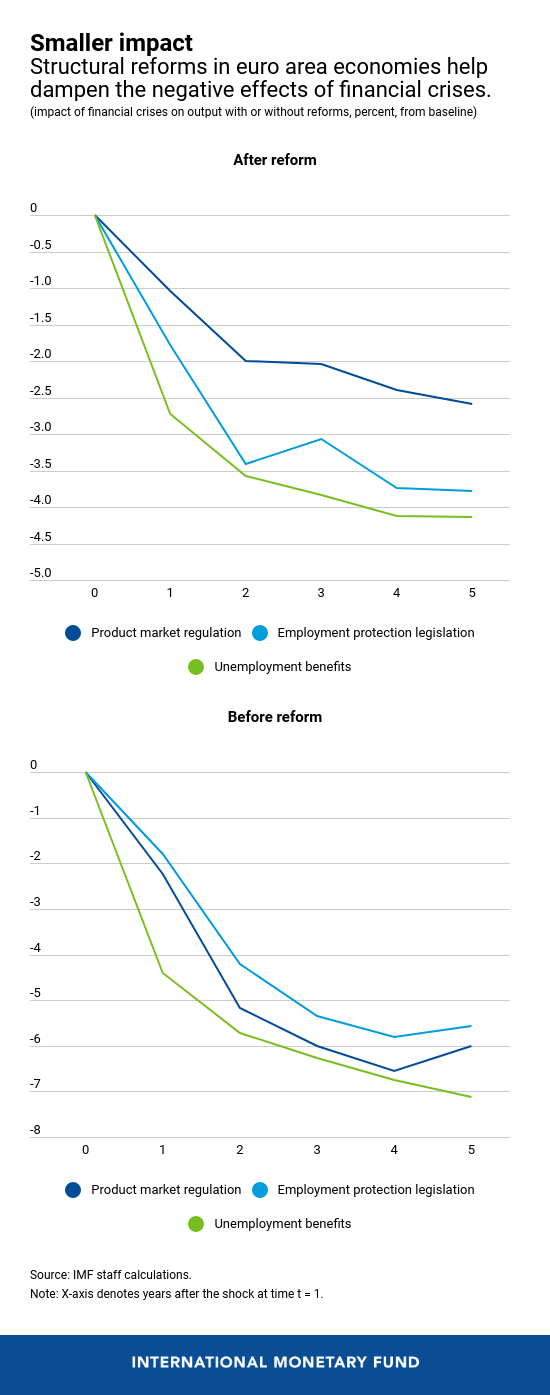

Our findings show that improvements in national labor market policies, product market regulations, and corporate insolvency regimes would make economies more resilient, and reduce the economic and social costs of adverse shocks. This would enable the euro area to fare better in the event of a major shock.

Sound labor and product market regulations can strengthen resilience

For euro area economies to be more resilient, they need to be able to weather temporary shocks, such as a credit crunch or supply disruption. They also need workers and capital to move into their most productive uses more swiftly in the wake of permanent shocks, such as a long-lasting loss in the external competitiveness of domestic industries.

Labor and product market regulations can help on both fronts. Over the past four decades, deep recessions resulted in smaller and less persistent output losses in those economies that had reformed their labor and product market regulations, compared with those that had not.

Improvements in national labor market policies, product market regulations and corporate insolvency regimes would make euro area economies more resilient.

For example, wage bargaining and benefit systems that make labor costs—hourly wages or hours worked—more responsive to labor market conditions can reduce job losses in bad times. Less cumbersome and more predictable layoff procedures for regular workers can help companies adjust and speed up the reallocation of workers away from declining firms and industries toward more promising ones. At the same time, carefully designed unemployment insurance schemes supplemented by strong job search support and incentives can provide the needed security to workers.

As for product market regulations, lower administrative barriers and startup costs can enable the economy to adapt more quickly to changing economic circumstances.

Our analysis suggests that getting labor and product market regulations right matters much more for the resilience of economies that lack independent national monetary policy and nominal exchange rates, like monetary union member countries.

Germany after the 2008 financial crisis is a case in point. Despite a major recession, unemployment barely increased. Firms were better able to adjust their labor costs through wages and—primarily—hours, partly reflecting the changes to the collective bargaining and benefit schemes that had taken place earlier in the decade, but also the effectiveness of a government scheme (“Kurzarbeit”) that financially compensated employees for lost hours at no cost to firms. The German economy recovered quicker than most of its European peers.

By contrast, in Portugal and Spain companies had much less flexibility, leading them to rely on the elimination of a large number of temporary jobs—themselves in part an outcome of stringent protection of regular contracts. Consequently, unemployment shot up in 2009, further amplifying the impact of the recession and the subsequent euro area crisis.

Better labor market policies need not mean across-the-board deregulation and weaker protections for all. Countries can design different packages that reflect their social preferences. For example, the “Anglo Saxon” and “Nordic” approaches to labor market institutions can deliver the needed flexibility. Both feature limited job protection, but they entail different worker protection and fiscal costs, with the “Nordic” approach relying on more generous unemployment benefits paired with strong job search assistance.

Better insolvency procedures

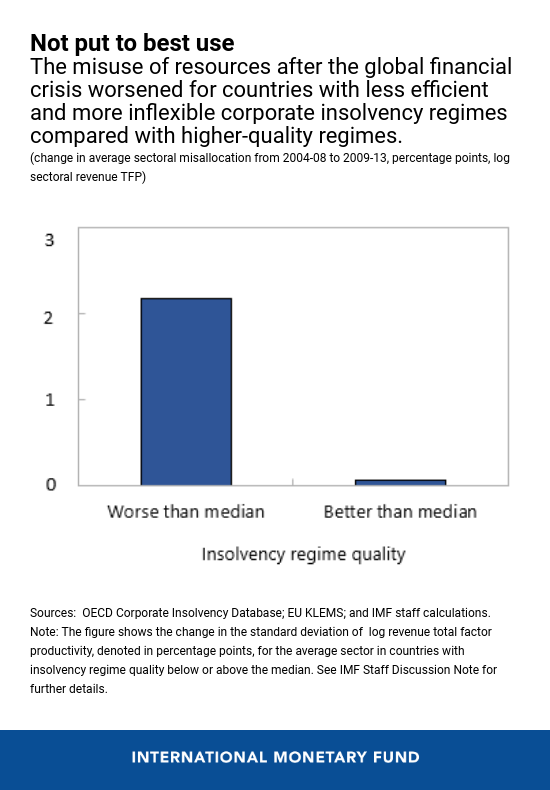

Lowering the cost and increasing the flexibility of insolvency procedures for companies is another type of national structural reform that can enhance resilience. Viable companies can restructure and recover more quickly, while so-called zombie firms that are not productive are eliminated. Some countries have made progress over the past decade—for example, Portugal—but there is scope for further improvement in many cases.

Efficient corporate insolvency laws hasten the reallocation of capital and workers toward more productive activities after deep downturns, alleviating misuse of resources and speeding up recovery. Indeed, after the 2008 global financial crisis, resource misallocation across industries rose on average in economies with a less efficient and more inflexible insolvency regime, while it barely budged in economies with a better-quality regime.

Reducing the burden on cyclical policies

Finally, by improving countries’ resilience, national structural reforms can also reduce the burden on cyclical policies—either national fiscal or common monetary policies to stabilize euro area member economies in difficult times. What about the effectiveness of those policies? In and of themselves, greater rigidities make economies more sensitive to shocks and hence tend to make countercyclical policies (policies that smooth the business cycle) more powerful. But if a country has limited fiscal space—for example, because of a high debt burden—then confidence can weaken if it attempts fiscal expansion. This can undo the typical expansionary effects of fiscal stimulus, raising the debt burden further for no return. This finding underscores the need for euro area economies not only to undertake reforms, but also to rebuild fiscal space as insurance against future downturns.

Fostering structural reforms should therefore be the key priority for the next European Commission. Not only would such reforms improve productivity, growth, and economic convergence, but—as suggested by our work—they would also build macroeconomic resilience against future downturns. This is an important task in a climate of increasing uncertainty, with mounting global and domestic risks.