The global financial crisis and its aftermath saw boom-bust cycles in capital flows of unprecedented magnitude. Traditionally, emerging market economies were counselled not to impede capital flows. In recent years, however, there has been growing recognition that emerging market economies may benefit from more proactive management to avoid crisis when flows eventually recede. But do they adopt such a proactive approach in practice?

In recent research, we analyze the policy response of emerging markets to capital inflows using quarterly data over 2005–13. Our analysis shows that emerging markets do react to capital flows—most commonly through foreign exchange intervention and monetary policy, but also using macroprudential measures and capital controls. Ironically, the most commonly prescribed instrument for coping with capital flows—tighter fiscal policy—is the least deployed in practice.

Menu of policies

Policymakers in emerging market economies have potentially five tools to manage capital flows: monetary policy; fiscal policy; exchange rate policy; macro-prudential measures; and capital controls. In deploying these, there is a natural correspondence (or mapping) between risks and instruments.

Monetary and fiscal policies can help address the inflation and economic overheating concerns raised by capital inflows. When the currency is not undervalued, foreign exchange intervention can be used to limit currency appreciation that threatens competitiveness; and macroprudential measures (such as reserve requirements, capital adequacy ratios, dynamic loan loss provisioning, etc.) can be applied to curb excessive credit growth and related financial stability risks.

Capital inflow controls can buttress these policies by limiting the volume of capital inflows or by tilting the composition of flows toward less risky types of liabilities. Countries with controls on capital outflows can also relax these restrictions to lower the volume of net flows, reducing overheating and currency appreciation pressures.

Proactive central bank response

Capital flows to emerging markets have been particularly volatile over the last decade. But emerging markets’ central banks have not been indifferent to this volatility.

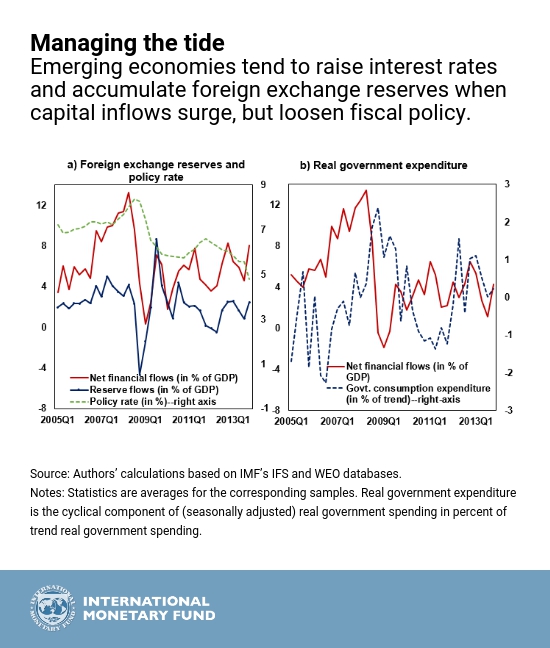

Foreign exchange intervention, for example, follows the ebbs and flows of capital, with a strong correspondence between reserve accumulation and net inflows. On average, emerging markets’ central banks purchase some 30–40 percent of the inflow, but some central banks, especially those in Asia (such as India, Indonesia, Malaysia) and Latin America (Brazil, Peru) tend to intervene more heavily, while others (such as Mexico and South Africa) tend to intervene less.

In terms of monetary policy, capital inflows elicit higher policy rates in emerging markets on average, though the impact depends on the behavior of inflation, the output gap (a measure of economic slack), and the real exchange rate. Policy rates are thus raised in response to higher inflation or a larger output gap—implying a counter-cyclical monetary policy stance—but lowered in response to real exchange rate appreciation.

Procyclical fiscal policy

When it comes to fiscal policy, however, the stance is strongly procyclical in the face of capital inflows. Thus, government consumption expenditure rises as capital inflows surge, and falls as capital inflows decrease—presumably because of political economy constraints, and/or because emerging markets face difficulty in accessing international credit markets in bad times.

Less orthodox policies

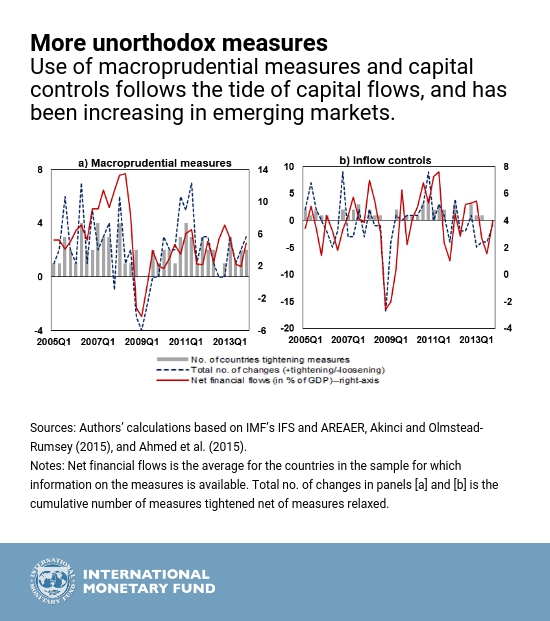

Turning to macroprudential measures and capital controls on inflows, our analysis shows that these measures are generally tightened as inflows surge and relaxed when flows recede. There is, however, considerable cross-country variation in response. Some countries, such as Brazil, Korea, Turkey, tend to use these measures more often than others.

For capital outflow controls, the reverse is true. Measures are relaxed when inflows surge—though it is only countries without fully open capital accounts, for example, India and South Africa, that tend to do so.

Natural mapping

Not only do emerging markets respond to inflows through various tools, their choice of the policy instrument also corresponds to the nature of the risk posed by capital flows.

Thus, foreign exchange intervention is generally used when the real effective exchange rate is appreciating, while what matters more for monetary policy tightening is the output gap. Macroprudential measures are typically deployed in the face of rapid domestic credit growth, while inflow controls are tightened when both credit growth and currency appreciation combine as a concern.

Bottom line

Following the repeated boom-bust cycles in capital flows, many emerging markets have internalized the lessons that they must manage capital flows if they are to reap the benefits of financial globalization, while minimizing the risks. They typically deploy a combination of instruments, with some correspondence between the nature of the risk and the tool deployed.

Nevertheless, there are important differences in policy response across countries, even in similar macroeconomic circumstances. This suggests that structural characteristics and political economy considerations may be at play in shaping a country’s specific policy response. An equally relevant question is whether the active policy management pursued by emerging economies has contributed to fewer financial crises in recent years. We hope that future research can shed light on these issues.