Back to Basics Compilation | Finance & Development | PDF version

I. The Big Picture

Supply and Demand: Why Markets Tick

When buyers and sellers get together, the key outcome is a price

For economists, a market is determined by how supply and demand come together to determine a price. Supply and demand are in turn determined by technology and the conditions under which people operate. At one extreme, the market could be populated by a large number of virtually identical sellers and buyers (for example, the market for ballpoint pens). At the other extreme, there might be only one seller and one buyer (as would be the case if I want to barter my table for your quilt).

Perfect competition

Economists have formulated models to explain various types of markets. The most fundamental is perfect competition, in which there are large numbers of identical suppliers and demanders of the same product, buyers and sellers can find one another at no cost, and no barriers prevent new suppliers from entering the market. In perfect competition, no one has the ability to affect prices. Both sides take the market price as a given, and the market-clearing price is the one at which there is neither excess supply nor excess demand. Suppliers will keep producing as long as they can sell the good for a price that exceeds their cost of making one more (the marginal cost of production). Buyers will go on purchasing as long as the satisfaction they derive from consuming is greater than the price they pay (the marginal utility of consumption). If prices rise, additional suppliers will be enticed to enter the market. Supply will increase until a market-clearing price is reached again. If prices fall, suppliers who are unable to cover their costs will drop out.

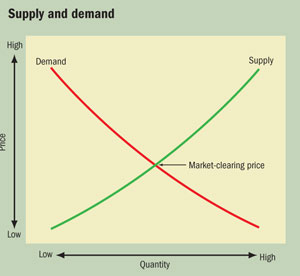

Economists generally lump together the quantities suppliers are willing to produce at each price into an equation called the supply curve. The higher the price, the more suppliers are likely to produce. Conversely, buyers tend to purchase more of a product the lower its price. The equation that spells out the quantities consumers are willing to buy at each price is called the demand curve.

Demand and supply curves can be charted on a graph, with prices on the vertical axis and quantities on the horizontal axis. Supply is generally considered to slope upward: as the price rises, suppliers are willing to produce more. Demand is generally considered to slope downward: at higher prices, consumers buy less. The point at which the two curves intersect represents the market-clearing price—the price at which demand and supply are the same (see chart).

Prices can change for many reasons (technology, consumer preference, weather conditions). The relationship between the supply and demand for a good (or service) and changes in price is called elasticity. Goods that are inelastic are relatively insensitive to changes in price, whereas elastic goods are very responsive to price. A classic example of an inelastic good (at least in the short term) is energy. Consumers require energy to get to and from work and to heat their houses. It may be difficult or impossible in the short term for them to buy cars or houses that are more energy efficient. On the other hand, demand for many goods is very sensitive to price. Think steak. If the price of steak rises, consumers may quickly buy a cheaper cut of beef or switch to another meat. Steak is an elastic good.

Of course, most markets are imperfect; they are not composed of unlimited buyers and sellers of virtually identical items who have perfect knowledge. At the other end of the spectrum from perfect competition is monopoly. In a monopoly, there is one supplier of a good for which there is no simple substitute. The supplier does not take the market price as a given. Instead, the monopolist can set it. (Monopoly’s twin is monopsony, in which there is only one buyer, usually a government, although there may be many suppliers.)

Barriers to competition

In monopoly situations, there usually is a barrier—natural or legal—to potential competitors. For example, utilities are often monopolies. It would be inefficient for two water companies to manage watersheds, negotiate usage rights, and lay pipes to households. But consumers have no choice except to buy from the monopolist, and access may be unaffordable for some. As a result, governments usually regulate such monopolies to ensure that they do not abuse their market power by setting prices too high. In return for allowing a company to operate as a sole provider, there may be requirements for minimum services to be provided to everyone or a cap on the prices that can be charged. These caps generally allow companies to recover fixed costs.

Monopolists cannot be oblivious to demand—which, as under perfect competition, varies, depending on price. The difference is that a producer in perfect competition fulfills only a portion of total demand, whereas the monopolist benefits from the demand curve of the entire market. So the unregulated monopolist can decide to produce a quantity that maximizes its profit—almost always at a higher price and in a smaller amount than in a perfectly competitive market.

In perfect competition a firm with lower costs can reduce its price and add enough customers to make up for lost revenue on existing sales. Suppose a firm earns 5 cents a unit selling 1,000 units—or $50—in a total market of 100,000 units. If it lowers its price by 1 cent and gains an additional 1,000 units in sales, its profits will be $80 on its new level of sales of 2,000 units.

Just one seller

But a monopolist controls all the sales—in this case 100,000 units at a nickel a share, earning a profit of $5,000. Lowering the price might increase total sales, but likely not enough to offset revenue lost on existing sales. Say it lowered the price (and profit per sale) by a penny, resulting in increased demand of 1,000 units. That would add $40 to revenues. But the monopolist would also lose a penny in profit on each of the 100,000 units it had been selling—or $1,000.

The key outcome of a monopoly is prices and profits that are higher than under perfect competition and supply that is often lower. There are other types of markets in which buyers and sellers have more market power than in perfect competition but less than under a monopoly. In those cases, prices are higher and production is lower than in cases of perfect competition. For example, if an airline had information on how much you valued a flight because it knew you were going to a friend’s wedding, it would know it could extract a higher price.

Supply and demand can also be affected by the product itself. In perfect competition, all producers make and buyers seek the same product—or close substitutes. In a monopoly, buyers lack easy substitutes. Variety, though, allows for substitution across types. For example, the market for tomatoes involves more than simply matching buyers and sellers of an idealized tomato. Consumers may want different types, and producers can respond. Market entrants could compete head to head with an existing producer by applying the same production technology, but they might instead introduce new varieties (cherry, beefsteak, heirloom) to cater to different tastes. As a result, producers have limited market power to set prices when markets are competitive but products are differentiated. Still, varieties of products can be substituted for one another, even if imperfectly, so prices cannot be as high as in monopolies.

A temporary monopoly

Complications arise when the main features distinguishing one product from another are expensive to create but cheap to imitate—for example, books, drugs, computer software. Writing a book can be difficult, but printing a copy has a low marginal cost. Consumers may buy many books, but if one becomes popular, competitors will have an incentive to undercut the publisher and sell their own copies. To allow the author and publisher to recoup fixed costs, governments often grant a temporary monopoly on that book (called a copyright) for the author and publisher. The price exceeds the marginal cost of production, but the copyright motivates authors to keep writing and publishers to produce and market books—ensuring future supply.

The market structures discussed here are a few of the ways supply and demand can differ according to context. Production technologies, consumer preferences, and difficulties in matching sellers with buyers are some of the factors that influence markets, and all play a role in determining the market-clearing price.