A Fork in the Road

Finance & Development, June 2016, Vol. 53, No. 2

China’s new growth strategy could hurt Africa’s commodity-dependent economies

China’s breakneck growth is slowing, and the drivers of that growth are changing from investment and exports to domestic consumption. This shift is affecting the global economy—but especially commodity exporters, many of which are in Africa. The Chinese Customs office announced recently that China’s imports from Africa fell by almost 40 percent in 2015. Slumping Chinese demand has led to precipitous price declines, putting pressure on the fiscal and external accounts of many African countries. Economic growth in sub-Saharan Africa, which averaged 5 to 6 percent over the past two decades, fell below 4 percent in 2015 and is expected to decline further in 2016.

Yet, despite the uncertain economic environment, in December 2015 Chinese President Xi Jinping promised $60 billion in financing for Africa over the next three years, which is more than twice the amount China pledged three years earlier.

Does China’s new growth model mean that Africa’s economic renaissance is over? Or can Africa adapt to the new realities and seize new opportunities, including in its engagement with China? In attempting to answer these questions, we first look back at the extraordinary growth in the economic ties between China and Africa.

China’s rapid growth over the past 40 years has turned it into a major trading hub for most countries in the world—directly, or indirectly through other trading partners.

A dramatic shift

This is the case in sub-Saharan Africa, where a remarkable shift in trade has taken place in the past two decades. Advanced economies accounted for close to 90 percent of sub-Saharan Africa’s exports in 1995; today new partners—including Brazil, China, and India—account for over 50 percent, with China responsible for about half of that. Similarly, in 2014, China became the single largest source of imports in sub-Saharan Africa.

Metal and mineral products and fuel represent 70 percent of sub-Saharan African exports to China. On the other hand, the majority of sub-Saharan Africa’s imports from China are manufactured goods and machinery.

Access to new markets for its raw materials has spurred Africa’s exports, which quintupled in real value over the past two decades. And by diversifying its trading partners, sub-Saharan Africa has reduced the volatility of its exports, which helped cushion the impact of the global financial crisis in 2008–09. When recession-ravaged advanced economies cut back imports, China increased its share of exports from sub-Saharan Africa, allowing most of the region to sustain robust economic growth. Trade has also boosted living standards in Africa through access to cheap Chinese consumer goods and has contributed to low and stable inflation.

Investor and lender

Sub-Saharan Africa has also diversified its sources of capital.

China’s foreign direct investment (FDI) in sub-Saharan Africa has increased significantly since 2006. Although the latest official statistics (2012) indicate that it is less than 5 percent of the region’s total FDI, which usually involves some form of control of an enterprise, anecdotal evidence suggests that the reality may be much higher. Many small-scale Chinese entrepreneurs have established themselves in Africa.

In addition, Chinese loans to sub-Saharan Africa—many of them financing public infrastructure projects—have risen rapidly (see “Impediment to Growth” in this issue of F&D), and China’s share of total sub-Saharan African external debt rose from less than 2 percent before 2005 to about 15 percent in 2012. This has provided many African countries with a welcome new source of project financing. And increasingly, China is relying on Africa, which is a large source of engineering contracts to build roads and hydropower projects.

China’s investment-heavy, export-oriented economic growth model made it a growing importer of commodities for most of this century. Chinese demand dramatically drove up the prices of metals, energy, and agricultural commodities to the benefit of sub-Saharan Africa’s many commodity exporters.

But that has changed. Reduced investment in China has curbed its appetite for raw materials, resulting in a sharp swing in its trade balance with sub-Saharan Africa. Iron ore and oil prices, for example, have fallen by more than half from their recent peaks, and many other commodities have also suffered sharp declines. Futures markets suggest further declines in 2016 and little recovery before 2020.

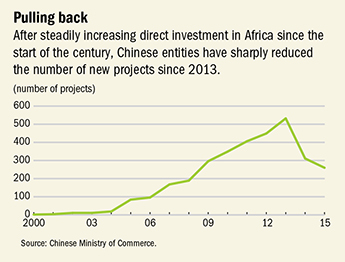

FDI is less cyclical and driven more by medium-term considerations than many other types of investment. But recent Chinese mine closures in sub-Saharan Africa (copper mines in Zambia, iron ore mines in South Africa, and the cancellation of an iron ore project in Cameroon, for example) suggest that returns on investment in the traditional commodity sectors are falling. In May 2015, China’s Ministry of Commerce estimated that the value of China’s FDI flows to Africa fell 45.9 percent in the first quarter of 2015 compared with the same period in 2014. The number of approved projects has also been falling since 2013 (see chart).

The immediate impact on commodity exporters has been severe. Oil exporters, in particular, are experiencing sharp declines in exports, putting pressure on foreign exchange reserves and exchange rates. Many commodity exporters also derive significant government revenue from natural resources and now face growing budget deficits and pressure to reduce spending. In Angola, for example, the fall in oil prices wiped out about half of its revenue base, with a loss of more than 20 percent of GDP. Lower spending levels, in both the public and private sectors, have led to sharply lower growth for oil-exporting countries, now expected to average barely 2 percent in 2015–16, compared with an average of more than 7 percent in the preceding decade.

The spillovers from China are not limited to direct channels such as lower export demand and global commodity price declines. There are also effects from one African economy on another. Slowdowns in large economies in sub-Saharan Africa, such as South Africa and Nigeria, affect smaller neighbors with which they trade. Uganda, which is not a commodity exporter, is affected by the economic contraction in South Sudan, which had become an important destination for Uganda’s regional exports. Countries such as South Africa, Zambia, and the Democratic Republic of Congo are important exporters to China and also are large importers from other African countries.

A silver lining

But the dark clouds have at least two silver linings. China’s recent pledge to more than double the financing for Africa to $60 billion over the coming three years reflects both a strong commitment to the continent and the continued availability of ample financing for Chinese investors. Of course, it will require identifying new commercial opportunities, likely outside of the traditional natural resources sectors. But the recent surge in Chinese outward capital flows, especially from Chinese businesses, signals a continued appetite among Chinese investors to make investments and seek high returns outside their economy. Africa’s non-commodity-dependent frontier economies in east Africa, for example, could be attractive new growth markets.

Moreover, global demographic trends provide an opportunity for sub-Saharan Africa to benefit from China’s new growth model (See “Surf the Demographic Wave,” in the March 2016 F&D). Bangladesh and Vietnam have already stepped into the global garment and textile value chains once dominated by China, which is moving up to other higher-value-added supply chains. In a supply chain, various stages of making a product, from extracting raw materials to final assembly, are performed in firms located in several countries. By 2035, the number of sub-Saharan Africans reaching working age (15–64) will exceed that of the rest of the world combined. If sub-Saharan Africa countries can reduce infrastructure bottlenecks, improve the business climate, and diversify their economies and increase their integration into global value chains over the coming decades, they will have a historic opportunity to decisively boost growth and reduce poverty on the continent. It will be up to the continent’s policymakers to seize this opportunity. ■

Wenjie Chen is an Economist and Roger Nord is Deputy Director, both in the IMF’s African Department.

Opinions expressed in articles and other materials are those of the authors; they do not necessarily reflect IMF policy.

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org