Sheltered from the Storm

Finance & Development, December 2012, Vol. 49, No. 4

Bas B. Bakker and Christoph Klingen

Europe’s central, eastern, and southeastern countries have been largely insulated from the ongoing euro area crisis, but that could change quickly

Central, eastern, and southeastern Europe have been notably absent from the euro area crisis. Financial markets have been very concerned about Greece, Ireland, Portugal, and—more recently—Italy and Spain. But they do not yet appear overly concerned about the 22 countries in central, eastern, and southeastern Europe (see box), despite their close ties with the euro area.

In a radical break with the past, investors are often demanding lower risk premiums for the debt of these smaller, less affluent European countries than for that of western European nations: Estonian risk premiums have at times been lower than those paid by the Netherlands and those of Bulgaria and Romania lower than for Italy and Spain.

On the euro border

Central, eastern, and southeastern Europe comprises the Baltic countries of Estonia, Latvia, and Lithuania; the central European Czech Republic, Hungary, Poland, and Slovak Republic; the southeastern European nations of Albania, Bosnia and Herzegovina, Bulgaria, Croatia, Kosovo, former Yugoslav Republic of Macedonia, Montenegro, Romania, Serbia, and Slovenia; and in the east Belarus, Moldova, Russia, and Ukraine. Turkey, which is in both Europe and Asia, is considered part of the region.

That wasn’t the case a few years ago, when the turmoil in western Europe that followed the onset of the global financial crisis in 2008 quickly spilled over to the central and eastern European economies. The region had many prosperous years, supported largely by easy credit from western Europe. But after the failure of Wall Street investment bank Lehman Brothers in September 2008, banks in the euro area countries abruptly stopped new lending, triggering a sharp contraction in domestic demand in most central and eastern European economies. A massive slump in global trade exacerbated the crisis, battering the region’s exports. As a result, the countries in the region suffered an unprecedented economic contraction in 2008 and 2009. By the time the region started to recover in 2010, GDP had declined by as much as 25 percent in some countries, although a few, such as Albania and Poland, escaped relatively unscathed.

Except for a scare in late 2011, countries in the region have been largely untouched by the euro area crisis that began two years ago—mainly because they rely far less today on easy credit from western European banks to support domestic spending and because they have taken steps to rein in government deficits.

Links still strong

This seeming ability to sidestep the euro area turmoil is occurring despite continued strong links between western and eastern countries. Since the Soviet Union dissolved two decades ago, western and eastern Europe have become increasingly interconnected, through both trade and financial channels.

Western Europe is the region’s largest export market. Some of the exports are inputs for western Europe’s exports. Many of the countries in the region have become part of a supply chain that provides inputs to final producers in western Europe. German car makers, for instance, have set up production facilities in central Europe and shifted part of their production to that region.

Trade linkages are especially important for central Europe. Although large commodity exporters such as Russia and Ukraine trade extensively with countries outside Europe, the prices their exports fetch in international markets are nonetheless linked to the well-being of the western European economies. By contrast, southeastern Europe is less integrated with western Europe.

But as central as trade is to the relationship, financial links—mainly through banks—are more important still. The region’s banking systems are tightly integrated with western European banks, both in terms of ownership and financing.

Foreign-owned banks (here meaning those in which a foreign entity has a stake of more than 25 percent and is the largest shareholder) account for about 35 percent of the market in Belarus, Russia, Slovenia, and Turkey, whereas in Bosnia and Herzegovina, Croatia, the Czech Republic, Estonia, Romania, and the Slovak Republic foreign banks have up to 80 percent of the market. By contrast, foreign banks on average account for less than 20 percent of the market in the euro area.

A foreign-owned bank, however, does not necessarily rely on foreign funding. For example, foreign-owned banks dominate in the Czech Republic, but their operations are locally funded, mostly through deposits. Such banks are less vulnerable to a sudden cutoff in foreign—in this case head office—funding.

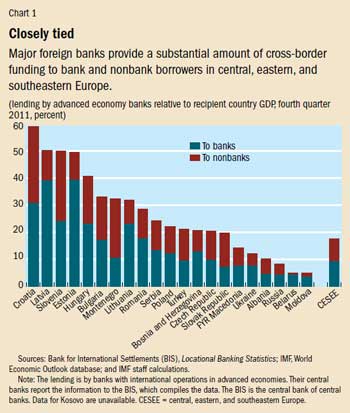

But cross-border funding by foreign banks is important in many economies in the region. It exceeded 30 percent of GDP in Bulgaria, Croatia, Estonia, Hungary, Latvia, Lithuania, Montenegro, and Slovenia at the end of 2011 (see Chart 1). This funding takes the form of western European parent banking groups financing the operations of their local affiliates, as well as direct cross-border lending to large corporations. In Russia and Turkey, even though market penetration of foreign banks is relatively low, local banks often supplement their deposits by borrowing in international interbank and bond markets to fund domestic lending.

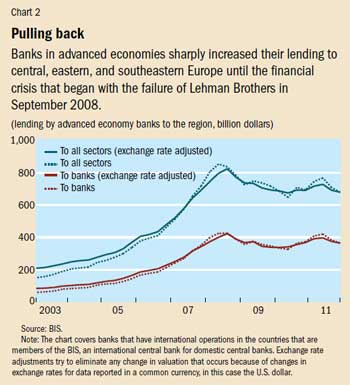

These tight financial linkages portended a big impact on central, eastern, and southeastern Europe from shocks originating in western Europe. That is what happened during 2008–09. Before the Lehman Brothers failure, western European parent banks financed the rapid expansion of domestic credit, which fueled an asset price and domestic demand boom. But when the global crisis hit western Europe, those flows suddenly stopped, plunging the region into a deep recession, which began to abate only after a revival of exports to western Europe in 2010 (see Chart 2).

Despite these strong continuing connections between eastern and western Europe, the euro area crisis that began two years ago has not had the same impact as the 2008–09 financial crisis. While borrowing costs in the countries in the euro area periphery—first Greece, then Ireland, then Portugal—rose relentlessly to reflect rising concerns of investors, relative borrowing costs for countries in central and eastern Europe remained flat or continued to decline as the region climbed out of the deep recession.

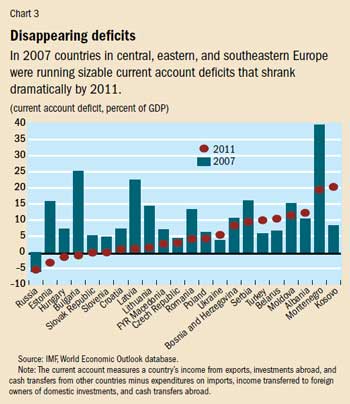

The main reason the region was so little affected by the current euro area crisis this time is the absence of large imbalances. In 2007 and 2008, the region was vulnerable to a sudden stop in capital inflows because countries were borrowing considerable amounts from abroad (mainly from banks in western Europe) to finance their large current account deficits. By 2011, a large portion of these imbalances had disappeared (see Chart 3). Today, economies are not overheating, and growth is increasingly driven by exports rather than domestic demand booms fueled by inflows of foreign capital.

Countries have also embarked on programs to reduce their fiscal deficits. In the run-up to the 2008–09 crisis, public finances were weak, although a rise in boom-related tax revenues created the illusion of a strong fiscal position. The end of the boom made it clear that the tax revenues were largely temporary: in 2009 the region’s fiscal balance swung from a surplus of 2 percent of GDP to a deficit of 6 percent. But by 2011, after most countries implemented large-scale fiscal consolidation, the region’s deficit was reduced to ½ percent of GDP.

Still, many countries face considerable risks. The need to refinance large external debt keeps borrowing requirements high. Large stocks of foreign currency loans constrain exchange rate and monetary policy. And Russia and Ukraine remain susceptible to declines in commodity prices. Fiscal deficits are still substantial in a number of countries, despite fiscal consolidation efforts to reduce deficits and debt. And banking systems are saddled with a large stock of nonperforming loans—a problem that did not exist prior to 2008.

A whiff of contagion

The limits to the region’s resilience were tested in the second half of 2011, when the problems in the euro area escalated. Euro area banks came under significant funding pressure. In response they pulled back on foreign funding operations. Foreign banks reduced their financing to central, eastern, and southeastern Europe by 6½ percent between June and December—compared with about a 3 percent reduction for Africa, the Middle East, and the Asia Pacific region and an increase of 2 percent for Latin America and the Caribbean.

Although that funding squeeze was partly offset by local deposit growth and an increase in lending by local banks, credit growth was negative in the Baltic countries, Hungary, Montenegro, and Slovenia.

The funding squeeze for the region eased when the European Central Bank (ECB) offered banks unlimited liquidity at low interest for a period of three years in late 2011 and early 2012. The July 2012 commitment by ECB President Mario Draghi to “do whatever it takes to preserve the euro” further eased market anxieties and helped relieve funding pressure.

Despite the recent improvements in financial markets, growth in the region has slowed sharply this year—a spillover from the recession in the euro area. The IMF, in its October 2012 World Economic Outlook, projects growth in central, eastern, and southeastern Europe of only 2.8 percent, down from 4.9 percent in 2011.

Moreover, tight trade and financial linkages keep the region at risk from renewed deterioration in the euro area. If the euro area crisis were to intensify, central, eastern, and southeastern Europe would be severely affected through both trade and financial channels. Exports would suffer if euro area growth declined rapidly, financial markets strains would intensify, parent bank funding would likely be scaled back, and capital inflows would drop—further affecting domestic demand.

The region is in better shape than in 2008, when it was an accident waiting to happen. Large imbalances had made the area very vulnerable to a sudden stop in capital inflows. This is no longer the case—the likelihood of home-grown crises is much reduced.

But this does not mean that the region is fully sheltered—it could still be affected by what happens in the euro area. Despite its newfound resilience, the region could be quickly overwhelmed by a worsening of the euro area crisis. That underscores the continuing need to rebuild buffers and hone crisis preparedness. ■

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org