Risky Business

Finance & Development, December 2010, Vol. 47, No. 4

İnci Ötker-Robe and Ceyla Pazarbasioglu

Global banks will adapt to the new international rules on capital and liquidity, but at what cost to investors and the safety of the financial system?

THE recent crisis revealed the significant risks posed by large, complex, and interconnected banks of all types and the fault lines in their regulation and oversight. Over the past two decades, financial institutions in advanced economies expanded significantly and increased their global outreach. Many moved away from the traditional banking model—taking deposits and lending at the local level—to become large and complex financial institutions (LCFIs). These global financial titans underwrite bonds and stocks, write and sell credit and other derivatives contracts, and engage in securitization and proprietary trading within and across borders. When they fail, as did the Lehman Brothers investment bank in 2008, their downfall can lead to plummeting asset prices and turmoil in financial markets and threaten the whole financial system.

International banking reforms, under what is commonly known as Basel III, will require banks to hold more and better-quality capital and liquid assets. The effect of these reforms will vary across regions and bank business models: banks with significant investment activities will face larger increases in capital requirements, and traditional commercial banks will be relatively less affected. The Basel III regulations will likely have the strongest impact on banks in Europe and North America.

These more stringent rules will affect LCFIs’ balance sheets and profitability. Banks will in turn adjust their business strategies, as they attempt to meet the tighter requirements and mitigate the effects of the regulatory reforms on their profitability. A key issue for policymakers is to ensure that the changes in banks’ business strategies do not result in a further buildup of systemic risk in the shadows of less-regulated or unregulated sectors (such as hedge funds, money market funds, special purpose vehicles) or in locations with less-onerous regulatory standards.

Tighter capital and liquidity rules

The new rules, approved by the leaders of the Group of Twenty advanced and emerging economies in November 2010, require, among other things

• higher and better-quality bank capital—mainly common equity—that can absorb greater losses during a crisis;

• better recognition of banks’ market and counterparty risks;

• a leverage ratio to limit excessive buildup of debt alongside the capital requirement;

• tighter liquidity standards, including through a liquid asset buffer for short-term liquidity stresses and better matching of asset and liability maturities; and

• buffers for conservation of capital.

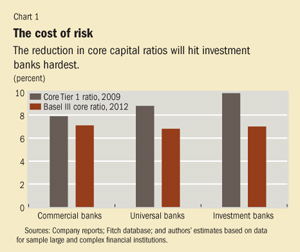

Our analysis of a sample of 62 LCFIs from 20 countries and covering three business models—commercial, universal, and investment banks—suggests that banks with significant investment banking activities, which derive earnings primarily from trading, advisory, and asset management income, will experience larger declines in regulatory capital ratios, mostly because of higher market risk weights for trading and securitization activities (see Chart 1).

Banks’ derivatives, trading, and securitization activities will be subject to tighter capital requirements as of end-2011 and, as a result, will be more costly. The goal is for tighter liquidity and capital requirements to ensure better coverage of the risk associated with those activities.

Universal banks, whose activities range from lending to investment banking, insurance, and other services, will also be affected by a combination of increased risk weights associated with their trading business and deductions from their capital as a result of their insurance business and minority interests related to third-party shareholdings in consolidated subsidiaries within a banking group.

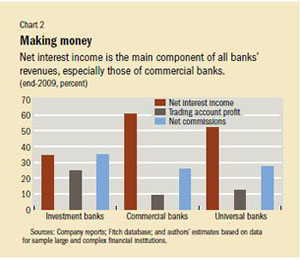

Traditional commercial banks whose principal source of income is lending activity (see Chart 2) will be the least affected, thanks to their simpler business focus and the gradual phase-in period.

Across regions, the regulations will have a greater effect on European and North American banks, reflecting the large concentration of universal banks in Europe and the impact of higher risk weights on trading and securitization activities.

Shaping banks’ business

Investment banking activities will also face regulatory reform initiatives beyond the Basel requirements that will raise their need for capital. The securitization business is subject to the U.S. Financial Accounting Standards Board’s new accounting rules, which require originators to consolidate some securitized transactions onto bank balance sheets. Moreover, the 5 percent risk-retention rule for all securitization tranches aims (for example, under the Dodd-Frank Act recently signed into law in the United States) will compel their originators to keep some skin in the game. Combined with higher Basel risk weights, these reforms are expected to limit the desirability and profitability of the securitization business.

Similarly, the derivatives business will be affected by the global proposals made by the Financial Stability Board—an international group of central bankers and regulators—on exchange trading and central counterparty clearing of over-the-counter (OTC) derivatives. Moreover, national initiatives, such as the U.S. requirement to move some banks’ derivatives business to separately capitalized nonbank subsidiaries, will have an impact. These regulations will affect investment banks and universal banks that are most active in derivatives business, while attempting to limit, through various exemptions, adverse effects on legitimate transactions, such as hedging.

The cost and profitability of the trading business, which boosted investment bank revenue in 2009, are also affected by higher Basel risk weights for the trading book and various global and national proposals (including the Volcker rule in the United States, which limits proprietary trading and investment in, or sponsorship of, private equity and hedge funds) and market infrastructure reforms that regulate OTC derivatives trading.

Basel III also affects banks with a universal banking focus. Banking groups undertaking a combination of commercial and investment banking activities will be affected by reform measures that target investment activities or systemically important institutions, including reforms that propose to break up banks or prohibit certain activities. While limiting these activities may not be costly from an economic perspective, the reduced ability to benefit from diversification and compensate low-margin activities with investment income could reduce banks’ ability to generate retained earnings, which add to a bank’s capital requirements and its resilience to adverse economic shocks.

Rules galore

Groups that carry out insurance and banking business under one roof, such as under the European bancassurance model, will feel the combined impact of the new Basel rules and Solvency II, an updated set of rules for European Union insurance firms set to take effect in late 2012. These will likely lower the capital benefits associated with this model—an intended consequence of the Basel reform measures. Partial recognition of insurance participation in common equity may help smooth out the real-sector implications for banking systems that rely heavily on the bancassurance model.

Globalized banks with a diversified set of business lines may also be affected by national-level structural reform proposals, including stand-alone subsidiarization (SAS) and living wills (that is, recovery and resolution plans for large banks that map out how to safely wind down institutions in case of failure). These reforms, by encouraging simpler and more streamlined corporate structures, may limit the diversification benefits of groups with different business lines. The key objective of the two proposed reforms is easier and less-costly resolution of large banking groups as a result of compartmentalized risk and individual group parts that are more resilient to shocks. By establishing effective firewalls between various parts of a banking group, SAS may affect the group’s ability to manage liquidity and capital and may hurt its ability to sustain a diversified corporate structure. This may have a greater impact on global banks with a centralized business model than on those with a decentralized or retail orientation.

Surviving by adapting

The combined effect of the various reform measures will therefore depend on how financial institutions react to the additional costs imposed on them—whether by shrinking their assets, repositioning across business lines, transferring the costs to customers through changes in margins and spreads, or restructuring their cost base and lowering dividends paid to shareholders.

Ultimately, the impact of the reforms on LCFIs will depend on the flexibility of their business model and how they adjust to the changes. Banks with a major investment banking focus could restructure their activities to reduce the effects of the regulatory reforms. With their flexible balance sheet structures, they can capture the most profitable segments to generate robust cash flows and earnings, buy or sell assets with relative ease, shift their operations rapidly, and manage capital by shrinking assets and repositioning their portfolios away from the most capital-intensive assets.

Such adjustments in business strategies could, however, have unintended consequences that increase systemic risk. As risky activities become more costly (for example, derivatives and trading activities, some types of securitization, and lending to high-risk borrowers), this business may shift to the less-regulated shadow banking sector. The risk to the financial system, however, may remain, given the funding and ownership linkages between banks and nonbanks.

Although supervision could help contain this vulnerability, its ability to do so may be limited without a widening of the scope of regulation. Moreover, absent careful global coordination of the implementation of tighter rules, some businesses may be prompted to move to locations with weaker regulatory frameworks to minimize regulatory costs. This may affect the capacity to monitor and manage systemic risk.

Safeguards are needed to mitigate the new rules’ unintended consequences and minimize the danger to banks’ ability to support economic recovery. Most important, supervisors must understand banks’ business models and have increased oversight in order to monitor and limit excessive risk taking. Stronger market infrastructure and risk management by financial institutions should accompany these efforts. Policies and their implementation need to be coordinated among national authorities and standard setters, given the global reach of many of these institutions. ■

İnci Ötker-Robe is a Division Chief and Ceyla Pazarbasioglu is an Assistant Director, both in the IMF’s Monetary and Capital Markets Department.

This article is based on IMF Staff Position Note 10/16, “Impact of Regulatory Reforms on Large and Complex Financial Institutions,” by İnci Ötker-Robe and Ceyla Pazarbasioglu with Alberto Buffa di Perrero, Silvia Iorgova, Turgut KıŞınbay, Vanessa Le Leslé, Fabiana Melo, Jiri Podpiera, Noel Sacasa, and André Santos.

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org