Islamic Banking

Good for Growth?

Finance & Development, December 2010, Vol. 47, No. 4

Patrick Imam and Kangni Kpodar

The spread of Islamic banking can spur development in countries with large Muslim populations

Features of Islamic banking

Islamic banks serve Muslim customers, but are not religious institutions. They are profit-maximizing intermediaries between savers and investors and offer custodial and other traditional banking services. The constraints they face are, however, different and are based on Shariah law. Four features are unique to Islamic banking:

• Prohibition against interest (riba) is the major difference between Islamic and traditional banking. Islam prohibits riba on the grounds that interest is a form of exploitation, inconsistent with the notion of fairness. This implies that fixing in advance a positive return on a loan as a reward for the use of one’s money is not allowed.

• Prohibition against games of chance (maysir) and chance (gharar): Islamic banking bars speculation—increasing wealth by chance rather than productive effort. Maysir refers to avoidable uncertainty; for example, gambling at a casino. An example of gharar is undertaking a business venture without sufficient information.

• Prohibition against forbidden (haram) activities: Islamic banks may finance only permissible (halal) activities. Banks are not supposed to lend to companies or individuals involved in activities deemed to harm society (for example, gambling) or prohibited under Islamic law (for example, financing construction of a plant to make alcoholic beverages).

• Payment of some of a bank’s profits to benefit society (zakat): Muslims believe in justice and equality in opportunity (not outcome). One way to do this is to redistribute income to provide a minimum standard of living for the poor. Zakat is one of the five tenets of Islam. Where zakat is not collected by the state, Islamic banks donate directly to Islamic religious institutions.

IN Islamic countries, many of them poor and not highly developed, large segments of the Muslim population do not have access to adequate banking services—often because devout Muslims are unwilling to put their savings into a traditional financial system that runs counter to their religious principles (see box). Islamic banks seek to provide financial services in a way that is compatible with Islamic teaching, and if Islamic banks can tap that potential Muslim clientele, that could hasten economic development in these countries.

There is evidence of close correlation between financial sector development and growth. Countries whose financial systems offer a variety of services—including banking and insurance—tend to grow faster. Banks, whether Islamic or traditional, play a fundamental economic role as financial intermediaries and as facilitators of payments (King and Levine, 1993). They also help stimulate saving and allocate resources efficiently.

Globally, the assets of Islamic banks have been expanding at double-digit rates for a decade, and Islamic banking is an increasingly visible alternative to conventional banks in Islamic countries and countries with many Muslims. Our study identifies the sources of Islamic banking’s expansion and ways to stimulate its continued growth. Knowing what drives the development of Islamic banking will help developing countries in Africa, Asia, and the Middle East catch up.

The rise of Islamic banking

Four decades ago, Islamic banking emerged on a modest scale to fill a gap in a banking system not attuned to the needs of the devout. Two events were crucial to its development. First, the early 1960s appearance in rural Egyptian villages of microlending institutions following Islamic banking principles demonstrated the feasibility of Islamic banking. These experiments thrived and spread to Indonesia, Malaysia, and sub-Saharan Africa.

Second, top-down support following the 1975 establishment of the Islamic Development Bank in Jeddah, Saudi Arabia, further spurred diffusion of Islamic banking by centralizing expertise. In its infancy, Islamic banking required much interpretation of Shariah law by Islamic scholars. In the first few years, basic implementation tools—such as legislation allowing such banks to be set up and the training of staff—were key ingredients for the spread of Islamic banking. And the past few years have seen rapid innovation, most recently improved regulation of liquidity management and accounting.

Similarly, the development of sukuk (Islamic bonds) has revolutionized Islamic finance in recent years: Islam prohibits conventional fixed income interest-bearing bonds. Harnessing sophisticated financial engineering techniques, sukuk are now a multibillion-dollar industry.

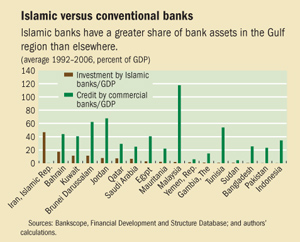

Rising oil prices since 2000 were also a catalyst, leading to a massive transfer of resources toward the large oil-producing countries, which have been more inclined to adopt Islamic banking. During the past decade, Islamic banking industry assets grew at an average 15 percent annually, and more than 300 Islamic institutions claim total assets of several hundred billion dollars. Two-thirds of Islamic banks are in the Middle East and North Africa, with the rest mainly in southeast Asia and sub-Saharan Africa. But even in countries with many Islamic banks, they are overshadowed by conventional banks. In the Gulf region, Islamic banks—in terms of their assets—account for one-quarter of the industry (see chart). Elsewhere, their share is in the single digits.

Islamic banking and development

The rise of Islamic banking has contributed to economic development in two main ways. One key benefit is increased financial intermediation. In Islamic countries and regions, large segments of the population do not use banks. The Islamic world, as a whole, has a lower level of financial development than other regions—in part because conventional banks do not satisfy the needs of devout Muslims. This “underbanking” means savings are not used as efficiently as they could be.

Moreover, because Islamic banking requires borrowers and lenders to share the risk of failure, it provides a shock-absorbing mechanism that is essential in developing economies. These economies—whether in the Middle East, Africa, or east Asia—are often large, undiversified commodity producers (mainly of oil) subject to boom-bust cycles and the vagaries of export and import price changes. In addition, most tend to have fixed or highly managed exchange rates, so the exchange rate is less able to absorb shocks. A mechanism that allows the sharing of business risk in return for a stake in the profits encourages investment in such an uncertain environment and satisfies Islam’s core tenet of social justice.

How Islamic banking spreads

Islamic banking is likely to continue to grow, because many of the world’s 1.6 billion Muslims are underbanked; understanding how Islamic banking spreads will help guide the formulation of policy recommendations. To that end, we estimated the factors behind the diffusion of Islamic banking around the world using a sample of 117 countries during 1992–2006. We also tested for whether it substitutes for—or complements—conventional banking.

We found, unsurprisingly, that the probability of increased Islamic banking in a given country rises with the share of Muslims in the population, income per capita, the price of oil, and macroeconomic stability. Proximity to Malaysia and Bahrain (the two main Islamic financial centers) and trade integration with Middle Eastern countries also make diffusion more likely.

Interest rates negatively affect the diffusion of Islamic banking, reflecting the implicit benchmark they pose for Islamic banks. Although pious individuals may have accounts only with Islamic banks, other consumers allocate their savings based on interest rates set by conventional banks. High interest rates hinder the diffusion of Islamic banking by raising the opportunity cost for the less pious (and individuals from other denominations who are increasingly attracted to Islamic banking) to put their savings in Islamic banks.

Some results, however, were unanticipated. First, Islamic banks spread more rapidly in countries with established banking systems. Islamic banks offer products not delivered by conventional banks and thus complement rather than substitute for conventional banks.

Second, we found that the quality of a country’s institutions, such as the rule of law or the quality of the bureaucracy, was not statistically significant in explaining the diffusion of Islamic banking. This is not true for conventional banking. Because Islamic banking is guided by Shariah, it is largely immune to weak institutions: disputes can be settled within Islamic jurisprudence.

Third, the September 11, 2001, attacks on the United States were not an important factor in the diffusion of Islamic banking. These events simply coincided with rising oil prices, which appear to be the actual driver of Islamic banking.

Policy implications

During the past decade, Islamic banking has grown from a niche market into a mainstream industry, and has likely helped drive growth in the Islamic world by drawing underbanked populations into the financial system and allowing risk sharing in regions subject to large shocks.

Even though our findings suggest little need for institutional reform, policy changes can still boost the spread of Islamic banking. Encouraging regional integration through free-trade agreements, maintaining a stable macroeconomic environment that helps keep interest rates low, and raising per capita income through structural reforms will lead to further expansion. The spread of Islamic banking is not, however, a panacea—it is merely one of many elements needed to sustain growth and development. ■

Patrick Imam is an Economist in the IMF’s Monetary and Capital Markets Department and Kangni Kpodar is an Economist in the IMF’s African Department.

This article is based on the authors’ IMF Working Paper 10/195, “Islamic Banking: How Has It Diffused?”

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org