About F&D Subscribe Back Issues Write Us Copyright Information Free Email Notification Receive emails when we post new

items of interest to you. |

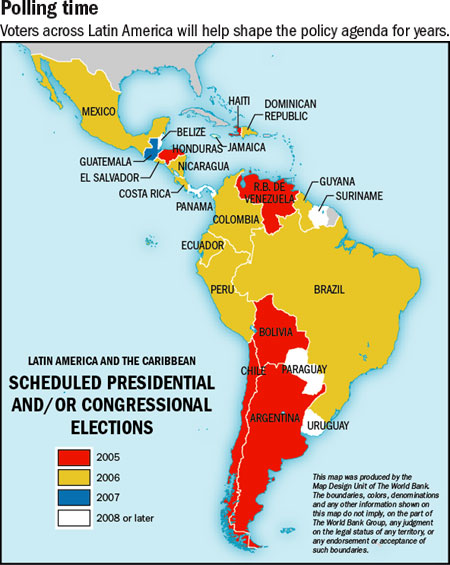

Region has fresh chance to entrench growth and break cycle of crises Latin America often appears to lurch from the cusp of success to the depths of crisis, so to talk about resurgence invites skepticism. Nevertheless, much of the region has witnessed a swift and robust recovery from the successive financial crises of 2001–02. Within two years, the region's economic growth reached 5.6 percent in 2004, a 24-year high. Growth rates of about 4 percent in 2005 and 3¾ percent projected for 2006 are well above historical averages. Since the so-called "lost decade" of the 1980s, Latin America has made progress on several fronts. Just 25 years ago, military dictatorships outnumbered civilian elected governments by two to one. Today the region is in the midst of an election cycle that will set the policy agenda and shape the continent for years to come. Destructive hyperinflation is becoming a dim memory, and Latin America is building resilience to external shocks by adopting market reforms and entrenching sound macroeconomic policies—raising the prospect that the current expansion will be more enduring than in previous cycles. However, persistently low per capita income growth, high or rising poverty, and rates of inequality that remain among the highest in the world (see "Stuck in a Rut" on page 18) have risked undermining popular support for reform programs launched during the 1990s that held out great promise but often yielded disappointing results—especially relative to other emerging market countries. Targeted social programs have helped meet specific needs, such as raising literacy and health standards, but interrupted reforms and growth, and recurring financial crises, meant that broader social improvements remained elusive—especially for the bulk of indigenous peoples (see "Latin America's Indigenous Peoples" on page 23). Thus, there has been a growing sense in many countries that the benefits of global integration have been unevenly distributed, accruing primarily to those in upper-income brackets, while the costs have been borne by the less-wealthy majority. In a few countries, there has even been a growing militancy among disenfranchised groups.

Given that many Latin American countries, including the largest, are holding elections over the next year or so (see map), the central question is whether the recent resurgence can be sustained once the global environment—still relatively benign despite high oil prices—becomes less friendly. After all, sustained, and even higher growth is critical to making a decisive impact on social and poverty indicators that remain weak with national poverty rates exceeding 40 percent of the population and secondary school enrollment averaging 62 percent. To provide perspective, this article draws on experience since the start of market-based reforms in the early 1990s to highlight policy priorities for the future. Better performance Latin American economies have generally performed well in the past two years. Growth has been significantly above historical averages, particularly in commodity-rich economies that have benefited from robust global demand (see Chart 1). Mexico and South American countries have gained, in particular, from the surge in fuel, food, and metals prices, and have generally been able to exploit these opportunities by expanding production—in some cases very substantially—although most oil exporters have not been able to do so. Inflation has stabilized in single digits, after a brief uptick. External positions have strengthened as booming exports have helped generate current account surpluses. Easy global liquidity conditions have contributed to capital inflows and rising international reserves (see Chart 2). And the recovery has also been better balanced than past episodes, with less reliance on domestic demand (see Chart 3).

This recent improvement in performance reflects policy efforts over a number of years that are now bearing fruit—with some countries, such as Brazil, Chile, and Mexico, leading the way (see box). What are the key elements? Every country is different, but there are several common factors.

Low inflation. The 1990s saw the establishment of low inflation, a striking achievement for Latin America, given its earlier record of high inflation. An important reason has been the emergence of widespread public awareness of the need to bring inflation down, leading to popular resistance to policies that would risk reigniting inflationary pressures, anchored by improved frameworks for monetary and fiscal policies. Policy flexibility. The adoption of market-determined exchange rates by many Latin American countries has greatly improved the flexibility and resilience of the macroeconomic policy frameworks. In parallel, the region has also successfully developed a more robust basis for monetary policy by moving away from exchange rate anchors and toward growing reliance on inflation-targeting regimes and autonomous central banks. The success of the region's inflation-targeting regimes and the willingness of country authorities to tackle inflationary pressures at an early stage have bolstered the credibility of monetary policy and contributed to prospects for a more durable recovery (see Chart 4).

Stronger fiscal positions and lower public debt. From 2002 to end-2005, the public debt-to-GDP ratio for the region is projected to fall by about 19 percent of GDP, with declines in virtually all the major countries (see Chart 5). The strengthening of fiscal positions through the generation of primary surpluses has been a major step forward—in contrast to the expansionary policies that led to large deficits during previous periods of easy access to international capital markets. Lower debt ratios have been supported by buoyant economic activity, exchange rate appreciations, and—in the case of Argentina—debt restructuring.

Improved external positions. The present upturn has been driven by strong and geographically more diversified exports and terms-of-trade gains. The resulting current account surpluses have raised reserves markedly and have significantly cut dependence on external capital inflows. This contrasts with earlier episodes, when capital inflows and domestic demand fueled much of the upswing, leading to wider current account deficits and overvalued currencies. Reduced external financing vulnerabilities. The better fiscal and current account positions have helped Latin America keep external issuance of bonds, equities, and loans well below the peaks of the late 1990s. Near-term vulnerabilities have also been reduced, as many governments in the region have taken advantage of the current benign international financial conditions to prefinance coming debt payments ahead of a full election calendar, and potentially less favorable global market conditions, in 2006. Expanded domestic capital market role. Several countries—notably Brazil, Chile, Colombia, Mexico, and Peru—have increased their reliance on domestic debt issuance, reducing their vulnerability to exchange rate risk and increasing liquidity in local currency markets (see Chart 6). Some countries, including Brazil, Colombia, and Uruguay, have also issued external bonds in local currency.

Institutional development. Economic institutions have become stronger, although the experience is highly differentiated by country and has not been uniformly sustained. The most rapid improvement was in the early 1990s, with some regression during the financial turbulence of 2000–02. Improvements include the evolution of more autonomous central banks (see "Taming the Monster" on page 26), stronger fiscal management in a growing number of countries, better management of public enterprises (including through privatization), and stronger financial regulation and supervision. Perceptions: falling short Yet despite the better economic conditions, Latin Americans continue to express a high degree of frustration with results that fall short of their expectations. Successive surveys by the opinion research group Latinobarómetro show that while there is strong support for democratic governments over authoritarian regimes—as well as for maintaining market economies—people are dissatisfied with the level of economic progress, the privatization of public services, the trustworthiness of public institutions, overall governance, and the amount of corruption. Many feel that their country has been governed for the benefit of a few powerful interests. And well over half believe that it would take more than 10 years to tackle corruption in the region, with a third believing that corruption will never be eliminated. Foreign investors are similarly frustrated with the high level of corruption. Indeed, cross-regional comparisons of the business climate generally portray Latin America in a poor light. The World Economic Forum's Global Competitiveness Report suggests that Latin America ranks well behind emerging Asia and Europe, and is falling further behind, especially on the quality of public institutions and technical innovation—shortcomings that reduce incentives for investment and entrepreneurship. Setting priorities Going forward, it is vital to build on the foundations for higher sustained growth, not only to insure against external risks—the strong global commodity prices and demand that have partly underpinned strong export growth may not last—but also to close the gap in growth performance with other dynamic emerging market regions and reduce poverty. While the overall impact of the recent increases in oil prices on the region's growth prospects has been small thus far, a further surge in oil prices could weigh on growth in partner industrial countries, weaken robust world demand for nonfuel commodities, and reverse some of the improvements to the trade balance realized since 2002. Oil-importing countries, especially those in Central America, have already been particularly affected. For the region as a whole, the risks related to a slowdown in growth in China are rising—even though China's share of total regional exports is still modest. Exporters of some key products (such as iron ore, soybeans, and copper) would be particularly exposed since China constitutes a significant proportion of their world consumption. Widening risk spreads for emerging market countries would also harm fiscal and external positions in many countries. The region has benefited from the unusually low level of global interest rates, which has encouraged a "search for yield" and bid down spreads on emerging market debt. Although countries in the region have used this favorable environment to strengthen fiscal positions and debt management, debt-to-GDP ratios in many countries remain very high—generally above 50 percent of GDP—and there remains a high dependence on exchange rate-linked and short-term instruments. Thus, Latin America is vulnerable to sudden shifts in global capital market conditions. To counter these risks, Latin American governments need to act on several fronts. First, to reduce macroeconomic vulnerabilities, policymakers should focus on: Reducing public debt. Despite recent progress, debt ratios continue to exceed the average of the mid–1990s, and generally remain above levels deemed conducive to sustained growth and broader macroeconomic stability, especially for countries with a history of default and high inflation. There are grounds for optimism because of the institutional strengthening that has taken place in many countries in recent years; in this context, fiscal rules and responsibility laws have proven helpful in containing discretionary procyclical spending in a number of Latin American countries, including Brazil, Chile, Colombia, and Peru. For oil exporters such as Ecuador, Mexico, and Venezuela, today's high prices provide an exceptional opportunity to further reduce public debt. Further efforts to curb nonessential expenditures, broaden and boost revenues, and improve budget flexibility would also spur growth by making room for increased spending on productivity-enhancing and poverty-reducing physical and social infrastructure. Keeping inflation low. Notwithstanding the remarkable progress in reducing inflation, scope exists to further entrench these gains, especially in the face of higher and more volatile oil prices. For example, sustaining the credibility of inflation-targeting frameworks that have helped anchor inflation expectations in a number of large Latin American countries will require keeping exchange rates flexible. Further steps to enhance central bank independence and policy transparency would also be helpful. Countries that pursue alternative policy approaches because of dollarization or specific trading patterns need to take special care to maintain sufficient robustness and flexibility in fiscal and structural policies. Accelerating financial sector reforms. Latin America still lags behind other regions in financial intermediation and credit availability. Real interest rates remain high in many countries, reflecting, among other things, inefficiencies in the banking system and, in some cases, the taxation of banking transactions. Countries need to strengthen financial system regulation, build consolidated supervision, bring financial regulation up to international prudential standards, and upgrade bankruptcy laws. The continued development of local currency capital markets (including the deepening of local government and corporate bond markets, equity markets, and the introduction of derivative products, where appropriate) to manage interest rate and exchange rate risk would help improve the efficiency of financial intermediation. A strengthening of financial sectors would also help reduce the high level of dollarization that still characterizes some countries. Peru has shown that a combination of good macroeconomic policies and improved financial sector regulation can successfully reduce dollarization. Second, to raise low saving and investment ratios, and attract investors, policymakers should focus on: Managing natural resources efficiently. Despite having the largest proven oil reserves in the world after the Middle East, the region has been slow to take full advantage of the oil price boom. The sluggish trend in output reflects short-term factors—including sporadic work stoppages—as well as deeper, underlying constraints that have inhibited necessary investments. Among the latter have been weak public finances, the dominant position of national oil companies with generally weak governance, and an unpredictable policy environment that has limited private-sector investment. A stronger national consensus is needed in many countries on improving the climate for new investment in these sectors, as well as on ensuring that the benefits are more equitably shared. Improving the investment climate. Latin America generally does less well than other, more rapidly growing regions in providing the key ingredients of a friendly investment climate. Heavy regulation of the entry and exit of businesses, cumbersome labor force practices, and weak contract enforcement divert domestic capital and investment overseas—often hitting hardest small- and medium-sized enterprises and those in rural areas. Business climates need to be improved to encourage private investment, particularly by improving regulatory frameworks and strengthening competition policy. Governance also needs to be better; corruption and weaknesses in the rule of law undercut investor confidence in the enforceability of contracts and property rights. Reforming labor markets. Labor market reforms—notably absent for most Latin American countries in the 1990s—will, over time, yield broad-based benefits, including more rapid growth of employment in the formal sector. The state should provide safety nets to deal with transitional problems associated with intersectoral mobility, and invest in workers' training and skill upgrading. Such reforms assume greater significance in the context of increased trade liberalization to encourage labor to move from less productive to more productive employment sectors. Liberalizing and diversifying trade. Notwithstanding recent gains, Latin America is still relatively closed to international trade compared with other dynamic regions, contrasting sharply with the openness in the capital account. Trade initiatives—including the Central American Free Trade Agreement (see "Building on CAFTA" on page 30)—may help, and a successful and ambitious conclusion to the Doha Round also could provide a significant boost. Despite the success in diversifying exports, the U.S. market accounted for over 40 percent of the increase in the region's exports between 2002 and 2004. Thus, robust growth in the United States, and continued access to U.S. markets, will be necessary to sustain healthy export performance, especially for countries with strong U.S. trade ties, such as Mexico. Fulfilling its potential Latin America's recent resurgence amid continuing favorable external conditions provides another historic opportunity for the region to catalyze its considerable natural and human capital resources into sustained and higher growth. Latin America's potential has never been in doubt—it has achieved several stretches of rapid growth in recent decades—but all too often, policy inconsistencies have precipitated debt and financial crises. With more consistent policies, the region could have sustained growth rates in the order of those found among the more rapidly growing emerging market countries in Asia. The crucial challenge now for the region is to build on its recent resurgence, minimize the policy swings and uncertainties that have undercut previous growth episodes, entrench the forces generating the current growth momentum, and deepen structural reforms—especially those related to institutional strengthening and the labor market—that will limit harmful discretion, reduce rigidities, and open up new avenues for private investment and entrepreneurship. Much greater macroeconomic stability would contribute to the consolidation of robust democracies, providing a suitable backdrop for the many elections that lie ahead.

|