Nearly all 32 countries in the Middle East and Central Asia have pledged to contain greenhouse gas emissions as part of the Paris Agreement. To meet these commitments, countries now need to urgently integrate climate policies into national economic strategies.

Our new study, the first of its kind for the region, assesses its commitment to reduce GHG emissions and identifies fiscal policy options to realize this goal.

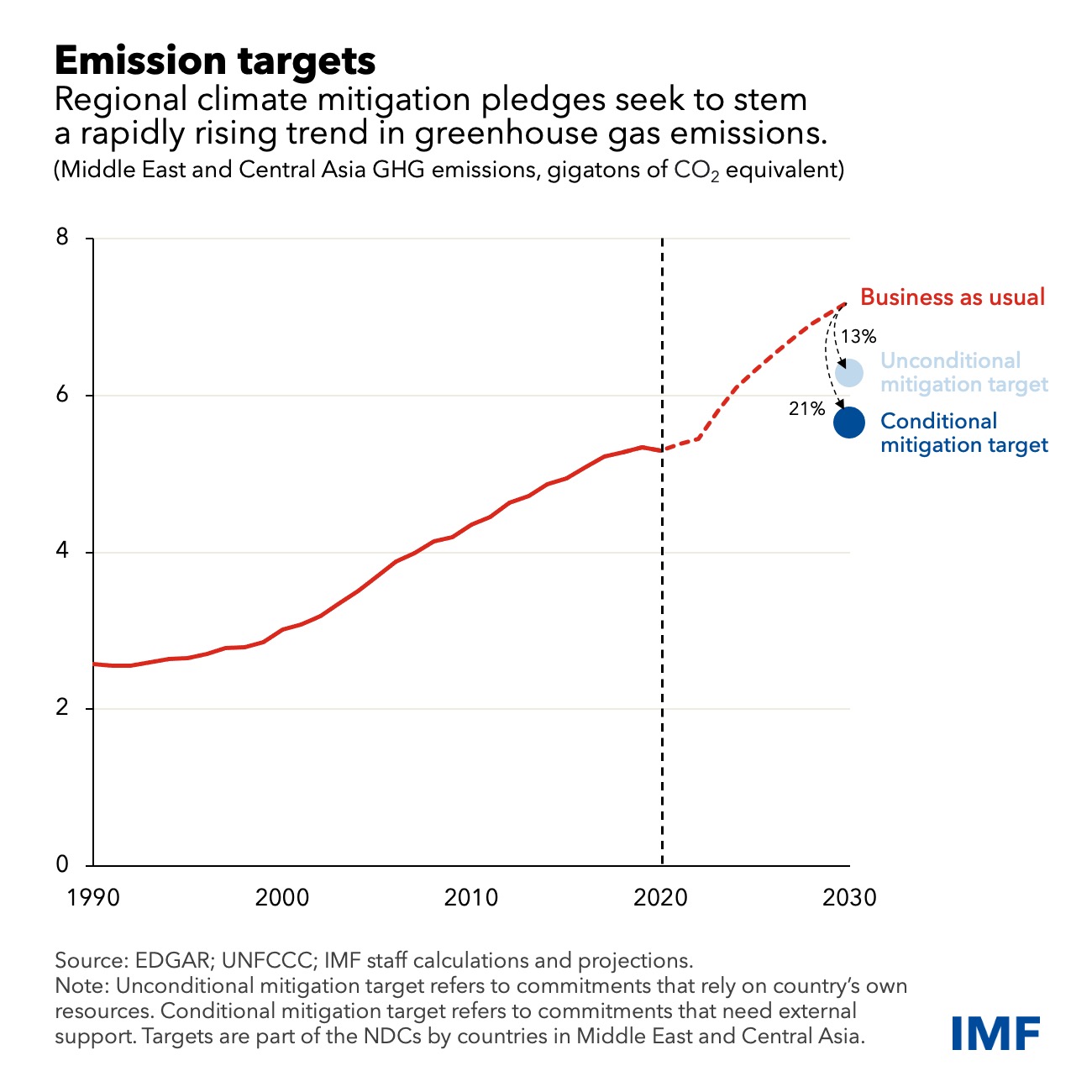

We estimate that countries in the Middle East and Central Asia have collectively pledged to reduce annual GHG emissions in 2030 by 13 percent to 21 percent, relative to the current trend, depending on the availability of external support. This means that the region will need to reduce its per capita emissions by as much as 7 percent over the next eight years. Only a few countries have achieved such a reduction while maintaining economic growth.

In our outline of policy options to meet the region’s mitigation commitment, we focus on two categories of fiscal policies—and trade-offs between them—to curb GHG emissions: first, measures that raise the effective price of fossil fuels and, second, public investments in renewable sources of energy.

Raising fossil-fuel prices

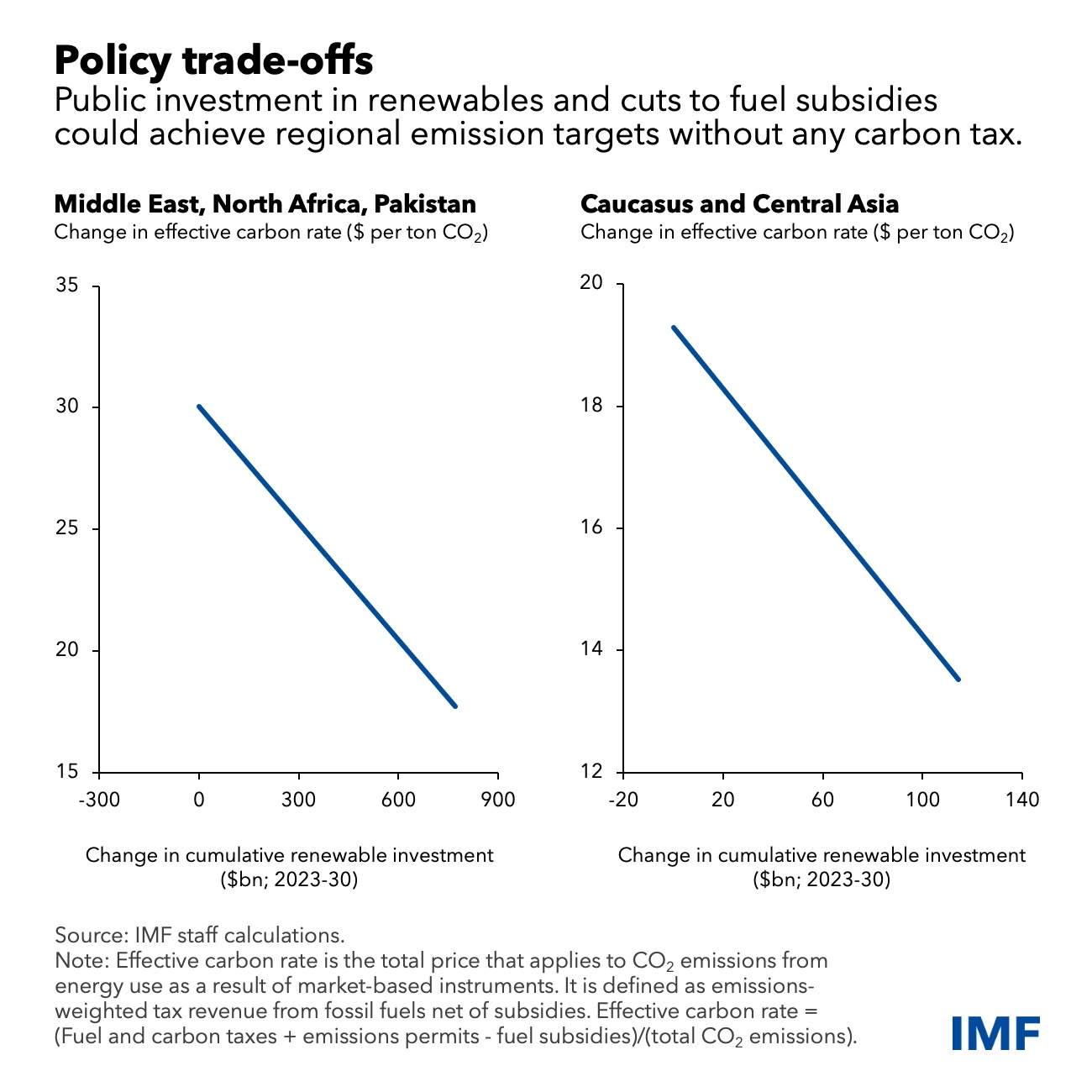

For the first, the region’s 2030 mitigation targets could be met through a gradual removal of fuel subsidies in addition to a phased introduction of a carbon tax of $8 per ton of CO2 emissions in the Middle East, North Africa, Afghanistan, and Pakistan, or MENAP, and $4 per ton in the Caucasus and Central Asia, or CCA.

Some countries are already taking steps in this direction. For example, Kazakhstan introduced an emissions trading scheme, Jordan has been steadily phasing out fuel subsidies, and Saudi Arabia recently established a regional carbon credit market.

Raising the effective price of fossil fuels has near-term challenges because it calls on the current generation to bear the burden of the energy transition. Vulnerable people and businesses that rely on cheap energy would be particularly affected. Though additional fiscal resources from tax revenues and reduced subsidies could ease these side effects, economic growth could temporarily slow, and inflation could increase.

In the long term, however, such a transition will leave future generations an economy that’s cleaner, more energy efficient, and potentially more competitive because it would inherit fewer distortions, stronger public finances, and a more efficient resource allocation.

Investing in renewable energy

For the second, additional public investments in renewable energy of $770 billion in MENAP and $114 billion in the CCA—more than a fifth of the region’s current gross domestic product—between 2023 and 2030 could achieve the region’s emission reduction targets with fuel subsidies reduced only by two-thirds and without any carbon tax.

Large-scale renewable projects are already taking off in the region. For example, Qatar developed the world’s largest solar plant, with an 800-megawatt capacity that can meet about a tenth of the country’s peak demand, while Dubai built a 5,000-megawatt single-site solar park that’s also the biggest project of its kind.

This option has several advantages for the current generation. Families and businesses wouldn’t be as hard pressed to change energy consumption habits because of a smaller price increase. Moreover, targeted investments in renewable energy sources will create more jobs and faster growth, while improving the energy security of oil-importing countries.

But this approach also has some long-term costs. Remaining fuel subsidies are likely to keep distorting energy prices, limiting energy efficiency gains and leaving emissions in many parts of the economy largely unabated. Significant public spending to accelerate the energy transition could weaken fiscal positions and macroeconomic stability, leaving fewer resources available to future generations.

We estimate that net government debt in 2030 could rise by 12 percent of GDP in MENAP and 15 percent in the CCA. Thus, a smoother transition now could set future generations on a path of lower long-term growth.

Time to act

Governments in the region face a difficult decision: how to share the economic burden of climate mitigation across generations. Other combinations of these fiscal strategies are also compatible with reaching countries’ emissions targets.

Countries should choose an option that best suits their circumstances and the available budget resources. Regardless of the choice, early adoption of a fiscal strategy will help meet mitigation pledges on time while minimizing potential economic disruptions.

Starting sooner would provide sufficient time for domestic public discourse, for the private sector to adjust to expected policy changes, and for the authorities to implement policies to address potential side effects, including improving social safety nets.

Finally, an early start will gear up other policies and structural reforms, helping countries in the region navigate a smoother path toward greener economies.