Imagine you plan to invest your savings and are looking for a firm or sector with a sustainable business model or a project that can make a real difference in the transition to a low-carbon economy. Where do you get reliable information to assess and compare projects from different companies?

Data gaps make it difficult to assess firms’ exposure to climate risk.

To give investors access to decision-useful information to effectively price and manage climate risks, there is an urgent need to strengthen the “climate information architecture.” There are three building blocks needed to support it: (i) high-quality, reliable, and comparable data, (ii) a harmonized and consistent set of climate disclosure standards, and (iii) a broadly agreed upon global taxonomy.

High-quality, reliable, and comparable data

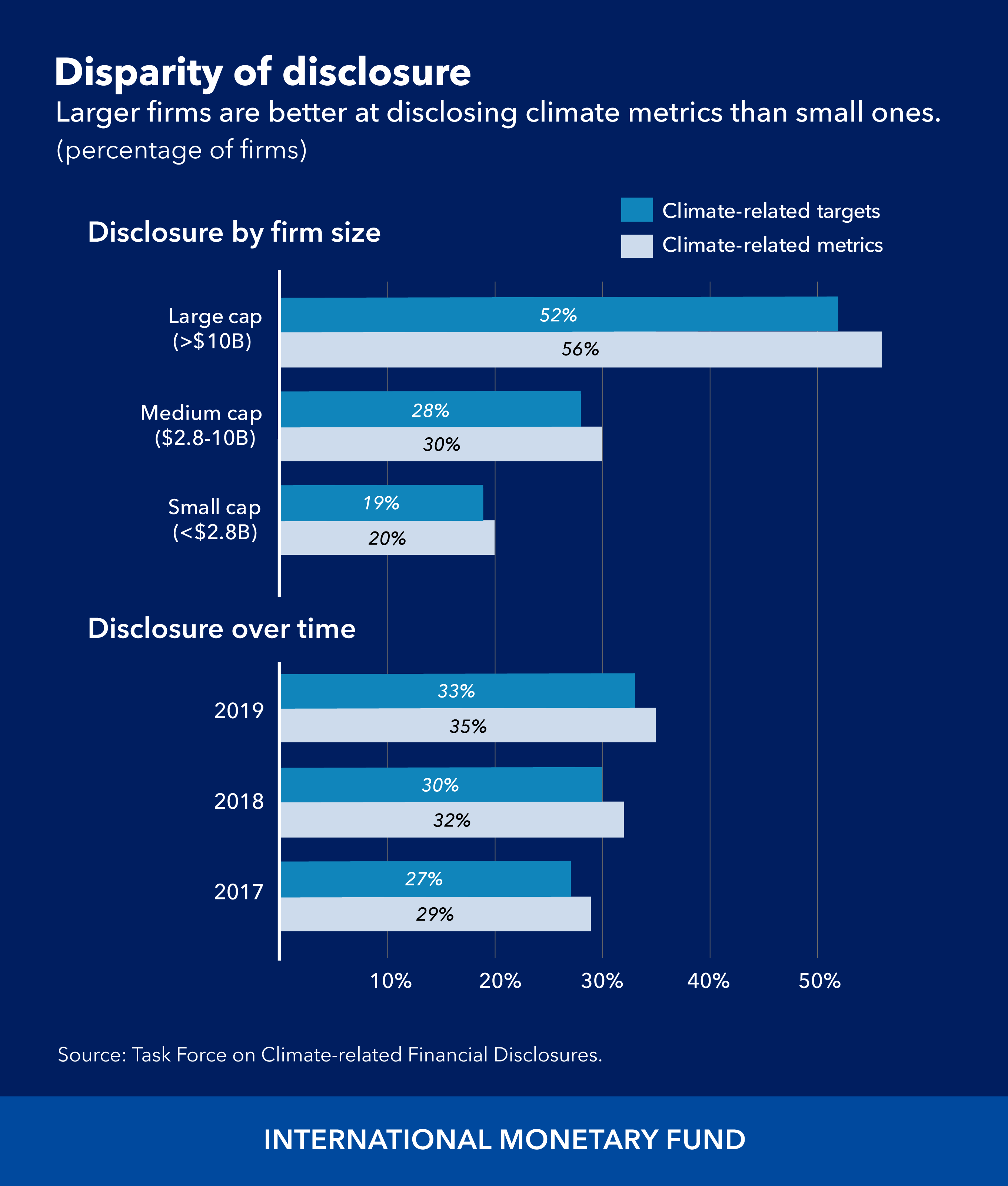

Currently, investors and policymakers face a lack of forward-looking, granular, and verifiable data—especially on firms’ efforts to move to sustainable business models (e.g., by reducing their greenhouse gas emissions). While a growing number of firms set emission reduction targets for themselves, the vast majority still does not provide this information, as shown in the chart below. Data gaps are particularly large for small and medium enterprises and for firms in emerging markets. These gaps make it difficult to assess firms’ exposure to climate risk and determine the impact of their investments on nonfinancial objectives, such as combating climate change.

Harmonized and consistent set of climate disclosure standards

One way to close these data gaps is through more and better disclosure of climate information by households, firms, and financial institutions. However, while firms are accustomed to publishing financial statements, “sustainability reporting” of climate-change risks and opportunities—in line, for instance, with the recommendations of the Task Force on Climate-related Financial Disclosures—is still in its infancy, and uptake is low, especially for smaller firms.

Moreover, with more than 200 frameworks, standards, and other forms of guidance on sustainability reporting and climate related disclosures across 40 countries, part of the problem is the multitude of existing frameworks currently used by firms and financial institutions, which undermines consistency and comparability. For example, some corporates may be asked to report according to different frameworks in different countries, making it difficult for investors to assess climate risks faced by such firms.

Broadly agreed-upon global taxonomy

Taxonomies—such as the recently published EU taxonomy are classifications of assets or activities that aim to improve market clarity on the extent to which investments support climate change adaptation and mitigation efforts. A well-designed and globally agreed taxonomy plays an important role in fostering sustainable finance markets, by helping communication with investors and facilitating the flow of capital towards climate-sustainable investments

However, by focusing excessively on fully sustainable investments, taxonomies can fail to recognize efforts by firms and countries to transition to a climate-sustainable business model, hindering the flow of capital to such firms. This is especially problematic in emerging markets where investments for transition purposes are needed the most and can have the largest benefits.

The way forward

Standardized and decision-useful information will be critical to help meet the large financing and investment needs associated with climate change mitigation and adaptation. Work to bridge the data gaps by the Network for Greening the Financial System to produce a detailed list of currently missing data items is an important step toward better data. For its part, the IMF has created a Climate Change Indicators Dashboard that brings together climate-related data needed for macroeconomic and financial policy analysis. Technological solutions, such as artificial intelligence and open-source data platforms and tools, can also be used for data collection and distribution.

As earlier IMF work has argued, convergence toward more-standardized sustainability reporting should now be a priority. To be useful in decision making, the information that gets reported should, first off, allow for investors to assess the value and the risks of firms and projects. Second, it should enable the monitoring of financial stability risks from climate change—something the IMF has also previously examined. And finally, the information should allow investors, policymakers, customers and other stakeholders to understand how firms will transition toward a more climate-sustainable business model.

Consolidating the multiple existing reporting initiatives is challenging. The International Financial Reporting Standards Foundation’s initiative to develop global sustainability reporting standards will help to promote transparency and global comparability. Aligning financial and non-financial reporting and providing assurance by auditors would also facilitate decision making, improving market confidence. Moving quickly in this direction is imperative, and building and improving on existing frameworks should be encouraged.

While steps towards globally agreed-upon taxonomies are less advanced than those on disclosure and data, efforts by the EU and others are notable. However, taxonomies must be flexible enough to recognize the complex efforts taken by companies to transition to a climate sustainable business model, especially in emerging markets and developing economies where investments are needed the most.

Challenges remain

To make more progress, a consistent, timely, and uniform implementation of internationally agreed sustainability reporting standards is necessary. Here, strong international commitment will be needed, while taking into account regional, institutional, and legal specificities, and while allowing individual jurisdictions to introduce additional requirements, if necessary. Moreover, implementation challenges for emerging markets—and for many small and medium enterprises—will have to be considered carefully.

Looking further ahead, the scope of the standards will need to be widened to address broader sustainability dimensions, for example environmental issues such as the loss of biodiversity, as well as social and governance issues.