Versions in Português (Portuguese), and Español (Spanish)

The global landscape has changed since our last update in October 2016. These changes have been mainly shaped by:

- An anticipated shift in the U.S. policy mix, higher growth and inflation, and a stronger dollar. In the United States—while potential policy changes remain uncertain—fiscal policy is likely to become expansionary, while monetary policy is expected to tighten faster than previously expected because of stronger demand and inflation pressures. As a result, growth is projected to rise to 2.3 percent in 2017 and 2.5 percent in 2018—a cumulative increase in GDP of ½ percentage point relative to the October forecast. The expected change in the policy mix and growth has led to an increase in global long-term interest rates, a stronger dollar in real effective terms, and a moderation of capital flows to Latin America.

- Improved outlook for other advanced economies and China for 2017–18, reflecting somewhat stronger activity in the second half of 2016 as well as projected policy stimulus.

- Some recovery in commodity prices, especially metal and oil prices, on the back of strong infrastructure and real estate investment in China, expectations of fiscal easing in the United States, and agreement among major petroleum producers to cut supply.

The impact of these global currents on Latin America is mixed, and domestic factors continue to dominate for some countries.

A positive boost from higher anticipated demand in the United States could be offset by higher global interest rates and uncertainty stemming from possible changes in U.S. trade and immigration policy, particularly for Mexico and Central America. At the same time, higher commodity prices since early 2016 have benefited commodity exporters. Yet, commodity prices are still expected to remain low relative to their historical standards.

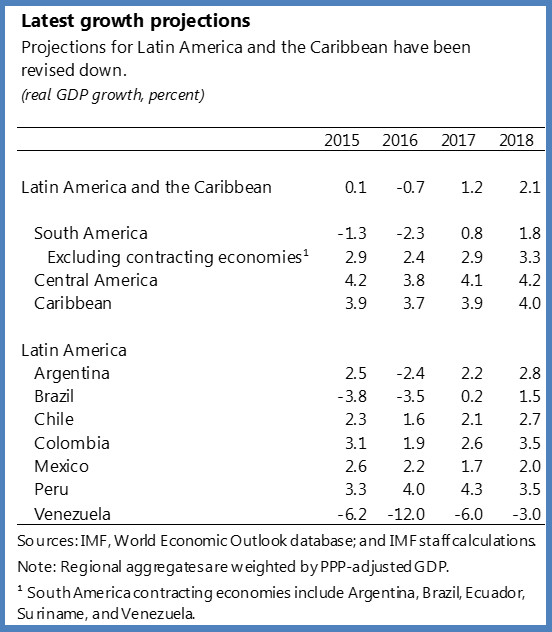

On balance, economic activity in the region is expected to expand by 1.2 percent in 2017 and 2.1 percent in 2018, following a contraction of 0.7 percent in 2016. The projected recovery is weaker than in our October forecast, given persistent weakness in some of the largest economies even as others continue to see moderate growth.

To spur activity, countries in the region are easing monetary policy, where appropriate, using available space to calibrate fiscal adjustment, and, more importantly, pursuing much-needed supply-side reforms.

South America: domestic policies and commodity prices at play

In Brazil, GDP continued to contract in the third quarter of 2016, and end-year activity indicators point to a delay in the recovery as private spending remains weak. Real GDP growth in 2017 is expected to turn positive and reach 0.2 percent. However, elevated unemployment and high private sector debt will continue to be a drag on demand. To spur growth, the government has announced measures to help highly indebted companies and reforms to reduce red tape and the cost of doing business. To bolster confidence in public finances, a constitutional amendment to cap central government noninterest spending in real terms was approved, and the government has submitted to Congress a draft pension reform. Meanwhile, the fiscal situation of several subnational governments has become increasingly difficult, and new legislation is expected to lay the basis for state-level adjustment and reform programs monitored by the federal government. Inflation has been declining rapidly in recent months, and at end-2016 was below the upper limit of the tolerance band. Citing weaker than expected growth, faster than expected disinflation, and progress with fiscal reform, the central bank accelerated significantly the pace of monetary policy easing in its last policy meeting.

In Argentina, the pace of contraction of economic activity slowed in the second half of 2016, but real GDP is projected to rebound this year, as higher real wages boost consumption, stronger external demand supports exports, and public investment accelerates. Still, because of the weaker than forecasted output growth in the last two quarters of 2016, GDP growth projections for 2016 and 2017 were revised down to -2.4 and 2.2 percent, respectively. The successful tax amnesty is expected to provide some fillip to domestic demand and help achieve the fiscal targets in 2016 and 2017. Inflation is expected to fall significantly but remain slightly above the central bank’s target in 2017. Continuing with macroeconomic adjustment and advancing a strengthening of the institutional framework will help bolster investor confidence in the fiscal and monetary policy targets and facilitate a rebound of private investment. At the same time, advancing the supply-side reform agenda remains essential to rebuild the foundation for stronger, sustained, and more equitable growth.

In Colombia, timely monetary and fiscal tightening have supported a faster than expected narrowing of the current account deficit, hence reducing external risks. Economic activity has been somewhat weaker than previously anticipated, growing by 0.3 percentage points lower in 2016 than projected earlier, and inflation pressures are dissipating gradually. Medium-term growth will be reinforced by the recently signed peace agreement and a structural tax reform, which will create space for key infrastructure and social spending.

Chile’s growth is projected at 2.1 percent in 2017, on top of the increase of 1.6 percent in 2016. Higher external demand, a stronger outlook for copper prices, and significant monetary easing are the main factors driving the pickup. But an uncertain regional outlook, higher interest rates abroad, and still low confidence at home could stand in the way of a noticeable recovery.

In Peru, growth remains relatively resilient. Growth is expected to reach 4.3 percent in 2017 as a result of expanding copper production, higher copper prices, a rebound in regional and local public spending, and robust private consumption. With the output gap closing, focus should shift to gradual fiscal consolidation, while preserving public infrastructure spending, and growth friendly-structural reforms such as decreasing informality, raising the level of education, deepening capital markets, and reducing red tape.

The economic outlook for Ecuador has improved, in light of the better access to international capital markets prompted by the recovery in oil prices.

Venezuela remains in a deep economic crisis on a path to hyperinflation, led by a large fiscal deficit that has been monetized, extensive economic distortions, and a severe restriction on the availability of imports of intermediate goods. Economic activity is projected to contract sharply in 2017, while inflation is expected to accelerate further.

Mexico, Central America, and the Caribbean

Mexico’s economy continues to grow moderately but is entering a difficult terrain. The outlook is clouded by uncertainty about U.S. trade policy which, along with tighter financial conditions, will be a drag on activity. To maintain market confidence and put public debt firmly on a downward path, it is important to persevere with fiscal consolidation. Although inflation has been rising following the sharp peso depreciation and increases in energy prices, the tightening of monetary policy should help keep inflation expectations under control. Going forward, further tightening will only be needed to prevent any second-round effects, as the rise in inflation that is due to changes in relative prices of tradable goods will be temporary.

Economic activity in Central America and the Dominican Republic has been supported by faster U.S. growth, though higher global interest rates and an appreciation of the dollar pose downside risks, particularly for countries where exchange rates do not depreciate with respect to the U.S. dollar. Inflation is low, at 2¼ percent, and external positions are robust given still low commodity prices and strong remittances inflow in some countries.

Prospects for the Caribbean region are improving, with moderate growth projected for 2017. Growth in tourism-dependent economies will be supported by the expected higher growth in the United States, while commodity exporters will benefit from somewhat higher (though still low) commodity prices, notably of oil. The region continues to face several risks, including the withdrawal of correspondent banking relationships and a high degree of policy uncertainty in the United States.

Countries should enhance resilience and long-term growth

Amid increasingly volatile external conditions, exchange rate flexibility has served the region well and should remain the first line of defense against shocks. Well-established monetary policy frameworks in the region are suited to limit the exchange rate pass-through to consumer prices. Strong risk management practices and policies facilitating corporate balance sheet repair are also critical to reduce vulnerabilities arising from a tightening of global financial conditions and sharp currency movements.

Countries should continue to use available space to calibrate fiscal adjustment, as commodity prices are expected to remain low relative to their historical levels, notwithstanding the recent uptick. The needed pace of adjustment will depend on debt levels and market pressures. Beyond macroeconomic policy adjustment, structural reforms—such as decreasing informality and red tape, boosting infrastructure quality, and improving education and rule of law—are essential to support medium-term growth.