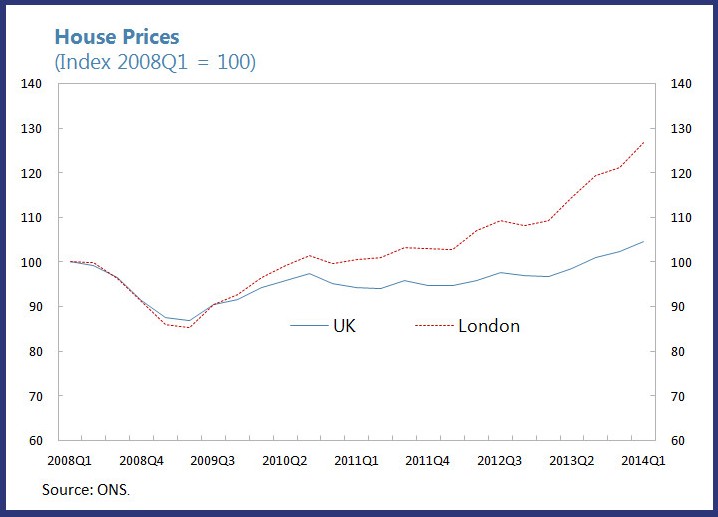

House prices are rising rapidly in the UK at an annual rate of 10.5 percent. House price inflation is particularly high in London (20 percent per year), and it is gradually accelerating in the rest of the country. The recent increases in house prices have been getting a lot of attention, and understandably have raised questions about living standards and whether another “boom-bust” cycle has begun.

The current UK housing cycle raises two important questions. What is driving the rise in house prices? And how should macroeconomic policies respond?

Macroeconomic policies should tackle two crucial issues in the housing market: (i) mitigating systemic financial risks during upswings in house prices and leverage; and (ii) encouraging an adequate supply of housing in order to safeguard affordability. In this blog, we discuss how the UK authorities are addressing these two issues and what additional policies may be necessary to manage risks from the housing market.

The current UK Housing Cycle

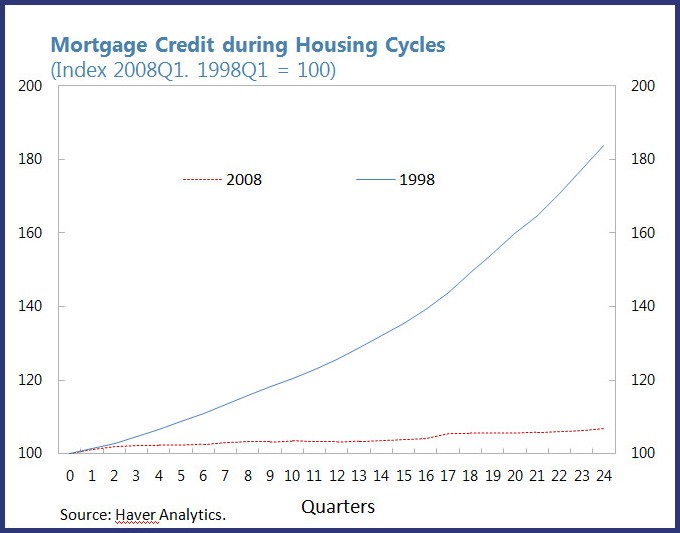

Historically, episodes of high house price inflation in the UK have been associated with a rapid expansion of incomes and mortgage credit. But the current housing cycle is notably different from the past episodes: aggregate mortgage credit growth has been relatively weak (only 1 percent over the past year), as has gross disposable income (0.5 percent growth in 2013), yet, in spite of this, house prices have been steadily increasing.

Accelerating prices explain in large part by a structural undersupply of housing in areas where demand is high, compounded by pent-up demand as credit conditions ease and consumer confidence returns.

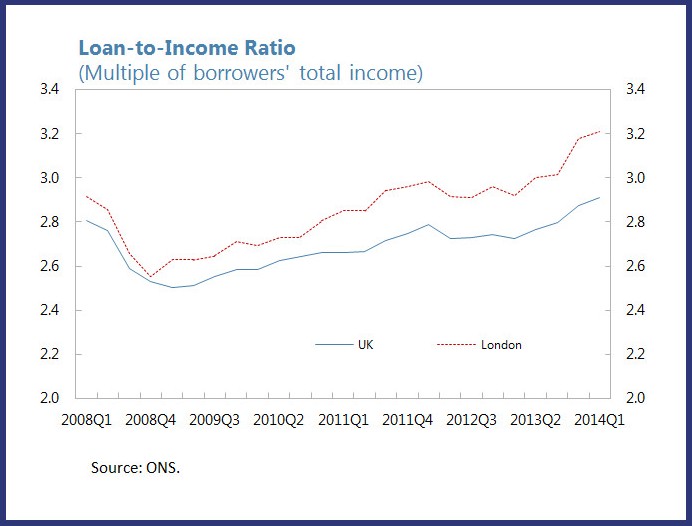

Perhaps because of expectations of further house price increases and a desire to get on the housing ladder, some households are taking larger loans relative to their incomes. The increase in the number of high loan-to-income (LTI) mortgages is more pronounced in London and among first-time buyers. As a result, an increasing number of households are vulnerable to negative income and interest rate shocks.

Addressing financial risks from the housing market

The UK authorities have implemented several policies designed to mitigate potential risks from the housing market. First, they have strengthened banks’ buffers against housing market exposures by applying more stringent mortgage risk weights and by increasing the provisioning of forborne retail mortgages. Second, they have tightened underwriting standards, for example, by verifying the income of new borrowers. Third, they have refocused the Funding for Lending Scheme toward business, by making household lending no longer eligible for borrowing allowances.

More recently, the government has recommended a cap on mortgages with high loan-to-income ratios, addressing the problem of excessive household indebtedness in the financial system, while allowing lenders to have the flexibility to allocate the risk of their mortgage portfolios.

The 2014 UK Article IV Staff Report analyzes recent experiences of such “macroprudential” measures in advanced economies, and suggests that that caps on debt-to-income (DTI) and on loan-to-value (LTV) ratios are potent tools to dampen mortgage credit growth and to mitigate financial stability risks. The effectiveness of these tools is enhanced when they are used simultaneously with additional macroprudential measures. Countries tend to implement macroprudential policies gradually, possibly as a result of the uncertainty of the transmission mechanism of those policies.loan

However, if these policy measures prove to be insufficient, then the Bank of England might want to consider an interest rate hike to tighten financial conditions. This would certainly have an effect, but the decision would require weighing the immediate costs in terms of growth and employment against the effects of an increase in financial risks associated with the housing market.

Addressing structural problems of housing supply

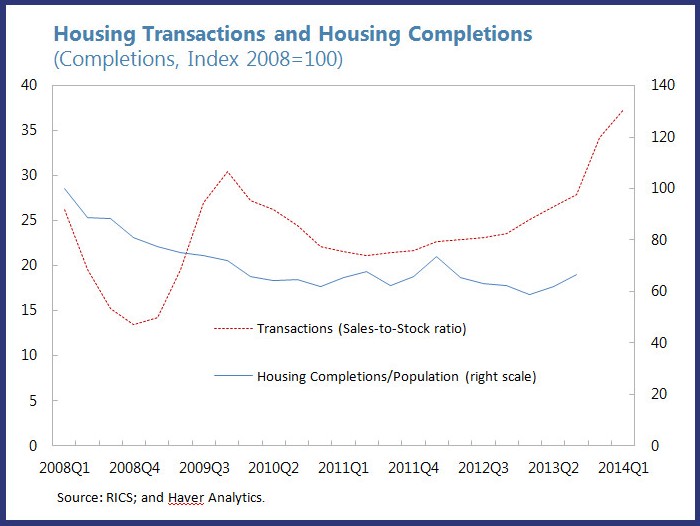

The recent trends in house prices ultimately reflect an imbalance between demand and supply. While the demand for housing—measured by the volume of transactions— has recovered to pre-crisis levels, housing supply—measured by housing completions per capita—is lagging. Micro- and macro-prudential policies will only be able to affect the demand for housing, but will not influence the supply for housing and consequently its affordability in the medium and long term.

Recent reforms in the planning system are contributing to a gradual increase in house building from recession lows, but more is needed to remove the unnecessary constraints and regulations on development. Further reforms to the tax system could encourage a more efficient use of land and provide economic incentives to local councils to grant more building permits, for instance by better linking local fiscal revenues with the development of local projects. It is also crucial to further develop the private rental market sector in the UK, which currently accounts for approximately 16.5 percent of households.

Ensuring long-run affordability and addressing financial stability risks requires understanding the nature of the problem—and what can reasonably be expected from different policies. The financial authorities are concerned about the potential for financial risks and have employed new measures to control them. But, notwithstanding recent changes to planning laws, more will likely be needed on the supply side. Ultimately this will require political and social consensus to allow more houses to be built where they are needed.