What has been the role of foreign banks in financing growth and convergence in Central, Eastern and Southeastern Europe, and how is that role changing? This is discussed in the first issue of a new series of analytical work on the region called Regional Economic Issues, which we launched at a joint IMF/Czech National Bank conference two weeks ago in Prague.

In the 1990s, there were very few foreign banks—state-owned banks were dominant. Many countries went through severe banking crises. When banking systems were opened to foreign investors, foreign ownership quickly became prevalent (Figure 1) and the incidence of banking crises dropped dramatically. And where they still occurred, they were the usually the result of failing domestic banks—not foreign-owned banks.

In the 1990s, there were very few foreign banks—state-owned banks were dominant. Many countries went through severe banking crises. When banking systems were opened to foreign investors, foreign ownership quickly became prevalent (Figure 1) and the incidence of banking crises dropped dramatically. And where they still occurred, they were the usually the result of failing domestic banks—not foreign-owned banks.

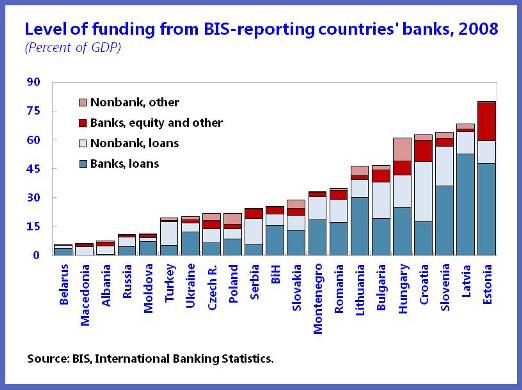

During the mid 2000s, though, foreign banks fueled and financed tremendous domestic demand booms which in many countries ended in busts. This was because foreign banks had access to large amounts of foreign funding (Figure 2)—mostly from their parent banks in Western Europe, who in turn were tapping wholesale funding markets—which they used to expand credit where demand was strongest and profits were highest. Countries in the region, with their bright growth prospects and relatively low credit penetration to start with, were attractive lending destintations. The ensuing booms were extraordinary in many countries.

During the mid 2000s, though, foreign banks fueled and financed tremendous domestic demand booms which in many countries ended in busts. This was because foreign banks had access to large amounts of foreign funding (Figure 2)—mostly from their parent banks in Western Europe, who in turn were tapping wholesale funding markets—which they used to expand credit where demand was strongest and profits were highest. Countries in the region, with their bright growth prospects and relatively low credit penetration to start with, were attractive lending destintations. The ensuing booms were extraordinary in many countries.

When the global crisis hit in 2008, new parent funding dried up and much of the previous inflows reversed, triggering deep recessions. The larger were the inflows during the boom years, the larger have been the outflows since 2008 (Figure 3), and the sharper the economic contraction (Figure 4).

Since late 2008, parent banks have been scaling back funding of their subsidiaries, who are increasingly relying on domestic deposit funding. Over time, this will help reduce boom-bust cycles, since retail deposits tend to be more stable. But the shift bears close watch to make sure it does not go too fast nor too far.

How can policy makers help? Establishing a banking union would facilitate home-host supervisory cooperation which, together with more coordinated use of macro prudential policies, would reduce the magnitude, and possibly also the likelihood, of future credit cycles. And tackling nonperforming loans—which in many countries are still very high—and developing local capital markets as an alternative source for investment finance would offset some of the headwinds to economic growth from less plentiful foreign funding.